U.S. Natural Gas Market Volatility and Seasonal Demand Risks: Navigating Short-Term Investment Challenges

The U.S. natural gas market in October 2025 is caught in a tug-of-war between lingering warm weather, elevated storage levels, and surging export demand. For short-term investors, understanding these dynamics is critical to navigating volatility and positioning for potential catalysts.

1. Warm Weather Delays Heating Demand, But Cooling Loads Remain Uneven

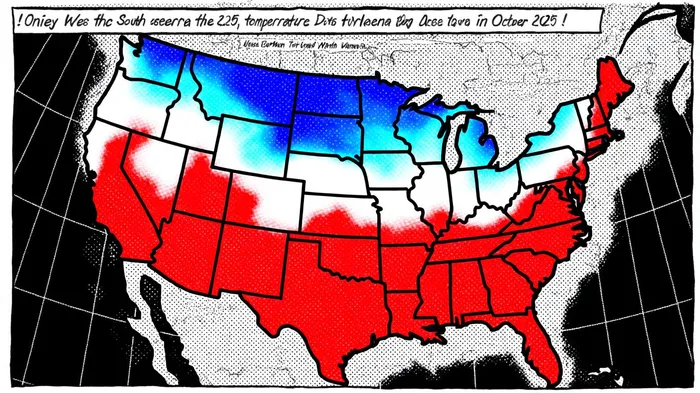

Recent temperature data reveals stark regional contrasts. Florida, Texas, and Louisiana-key consumption hubs-have experienced persistent warmth, with Orlando recording an average of 71°F and Texas averaging highs of 87°F in early October, according to an Energy Central overview. These conditions have suppressed heating demand, a traditional winter driver, while cooling needs in the South and West have remained elevated. Florida alone logged 102 degree days, the highest among major regions, as reported in EIA Today in Energy. However, the EIA notes that overall natural gas consumption in October has been lower than winter peaks, reflecting milder temperatures compared to historical heating seasons, as shown in AGA market indicators.

The National Weather Service forecasts a gradual shift: by mid-October, northern regions are expected to see deeper autumn cooling, potentially boosting heating demand as early as October 14–23, according to a NaturalGasIntel analysis. This transition could create localized volatility, particularly in the Midwest and Northeast, where storage withdrawals might accelerate.

2. Storage Inventories Remain Elevated, Pressuring Prices

As of October 3, 2025, U.S. working natural gas inventories stood at 3,641 billion cubic feet (Bcf), 23 Bcf above last year's level and 157 Bcf above the five-year average, according to the EIA weekly storage. This surplus, driven by seven consecutive weeks of net injections exceeding 100 Bcf, has weighed on prices. The EIA projects inventories will reach 3,872 Bcf by month-end, further widening the gap from historical norms, per an OGJ report.

High storage levels are exacerbated by record production-daily output in the Lower 48 states hit 107.0 Bcf/d as of October 3-creating a bearish backdrop for near-term pricing, as noted in a Nasdaq article. However, analysts caution that this oversupply may not persist if cold weather triggers rapid inventory draws or if LNG export projects delay further.

3. LNG Exports and Global Demand: A Double-Edged Sword

While domestic demand has been muted, U.S. LNG exports have emerged as a key price driver. Record shipments to Europe and Asia-fueled by geopolitical tensions and weak Asian demand-have tightened domestic supply. The EIA forecasts a 20% increase in gas exports in 2025, with facilities like Plaquemines and Corpus Christi Stage 3 ramping up, according to a NaturalGasIntel note.

Yet, this export-driven demand comes with risks. Global markets remain fragile, with China and India reducing imports due to economic slowdowns and renewable energy adoption, as detailed in the IEA report. Additionally, the delayed ramp-up of the Golden Pass LNG Terminal could ease domestic supply pressures, potentially capping prices in the short term, according to a NaturalGasIntel article.

4. Short-Term Investment Risks and Strategic Positioning

For investors, the interplay of these factors creates a high-risk, high-reward environment. Key risks include:

- Weather Volatility: A sudden cold snap in northern regions could trigger sharp price spikes, while prolonged warmth in the South may deepen oversupply.

- Storage-Price Dynamics: Elevated inventories suggest a bearish bias, but rapid draws during cold snaps could reverse this trend.

- Global Market Shocks: Geopolitical shifts or Asian demand rebounds could disrupt the current export-driven equilibrium.

Strategic positioning should focus on:

- Hedging Against Weather Swings: Investors might consider short-term futures contracts to capitalize on potential cold-weather rallies.

- Monitoring Storage Reports: Weekly EIA data will be critical; deviations from the five-year average could signal turning points.

- LNG Project Timelines: Delays in export facilities could temporarily alleviate domestic supply pressures, offering upside potential.

Conclusion: Balancing Risks and Opportunities

The U.S. natural gas market in late 2025 is a study in contrasts: warm weather suppresses heating demand, but LNG exports and production surges create upward price pressure. For short-term investors, the path forward hinges on closely tracking weather patterns, storage trends, and global demand shifts. While the bearish case remains strong due to oversupply, the potential for cold-weather-driven rallies and export-driven tightness offers asymmetric upside. Positioning with flexibility-through diversified contracts and real-time data monitoring-will be key to navigating this volatile landscape.

Comentarios

Aún no hay comentarios