Nasdaq Leads at the Open, Dow and S&P Rise While Small Caps Slip

At the opening bell Friday, stocks tilted higher: the Dow Jones Industrial Average added +86.82 (+0.18%) to 47,608; the S&P 500 rose +45.14 (+0.66%) to 6,867.48; the Nasdaq Composite climbed +325.13 (+1.38%) to 23,906; and the Russell 2000 ETF edged down -0.65 (-0.27%) to 244.20.

On the micro side, Western Digital’s latest quarter underscored how the AI build-out is reshaping storage from a cyclical to a secular story, with revenue up 27% year over year, gross margin at 43.5%, and free cash flow of $599 million. Management cited multi-year hyperscale purchase orders, some stretching into 2027, and guided to sustained profitability as higher-capacity drives scale, with bullish read-throughs for peers across the memory and HDD complex.

Analysts also sharpened their pencils on the mega-caps. Wedbush reiterated OUTPERFORM on AmazonAMZN-- with a $330 price target, noting that AWS posted +20.2% year-over-year growth, outpacing expectations and easing the key overhang on the shares. “Following a reacceleration in AWS growth and positive commentary this quarter, we believe investors have regained comfort in management's ability to retain a leading position in the AI space,” Wedbush said in its report. The firm highlighted improving online retail and advertising trends and flagged the AI-enabled “Rufus” assistant as a sales driver.

For AppleAAPL--, Wedbush lifted its price target to $320, pointing to an iPhone 17 cycle that is outpacing last year’s model and a Services engine that delivered $28.75 billion in revenue, up 15% from a year earlier. Wedbush Managing Director Daniel Ives wrote, “Tariffs continue to remain a headwind to margins as Apple saw a $1.1 billion impact to profits…” yet the firm expects double-digit revenue growth in the December quarter and argues the time is ripe for Apple to accelerate its AI roadmap.

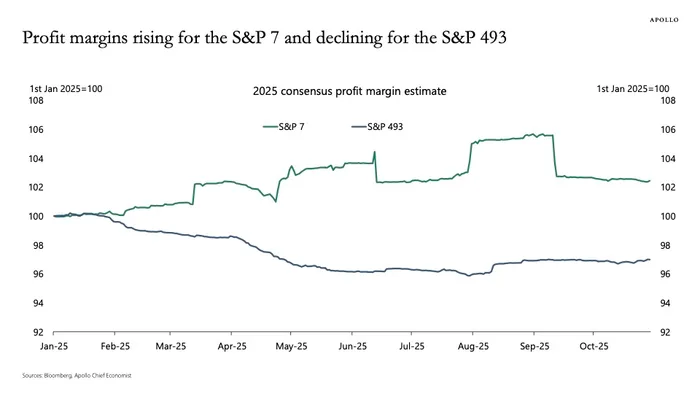

The macro backdrop remains uneven. Apollo Global Management’s chief economist Torsten Slok characterizes a K-shaped corporate landscape, with profit margins rising for the “Magnificent Seven” while slipping for the rest—an imbalance that can amplify index-level resilience even as breadth stays fragile.

Meanwhile, trade remains a wild card. As Rick Newman writes in The Rick Report, “A casual observer of President Trump’s trade wars might think that after eight months, they’ve accomplished precisely nothing.” Yet the piece argues the policy mix has materially shifted the playing field, with Trump acting as “the middleman on trade,” using tariffs to steer industrial outcomes while seeking to contain China. Newman includes a chart that shows the average effective U.S. tariff rate climbing to about 17.2% since January 2025, with the average on China near 47%, figures attributed to the Yale Budget Lab; the report adds that such revenue could be repurposed for domestic priorities.

With AI infrastructure still in the driver’s seat and tariff frictions lingering, investors are calibrating between micro strength in platform tech and macro policy uncertainty—a balance that will likely keep positioning tightly tethered to earnings execution and the durability of cloud-AI demand.

Comentarios

Aún no hay comentarios