NAKA's Deteriorating Fundamentals and High-Risk Outlook: A Deep Dive into Red Flags

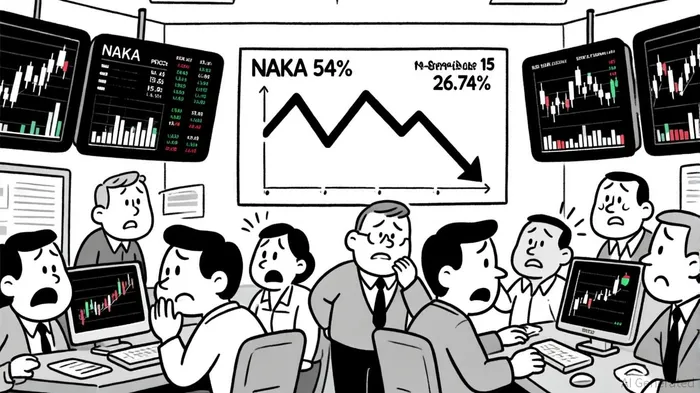

Kindly MD, Inc. (NAKA) has become a cautionary tale in the volatile world of speculative investing. Over the past month, the company's stock has plummeted by 26.74%, with a single-day freefall of 54% on September 15, 2025, sending shockwaves through the market[3]. This collapse is not merely a short-term volatility event but a symptom of deeper, systemic issues in NAKA's financial and operational health. From abysmal profitability metrics to a strategic pivot that has alienated investors, the company's fundamentals paint a picture of a business in freefall.

Financial Red Flags: A House of Cards

NAKA's Q3 2025 financials reveal a company hemorrhaging cash. Despite generating $2.72 million in revenue, the firm reported an EBIT margin of -242.9% and a profit margin of -244.44%, indicating losses far exceeding revenue[1]. These figures are among the most dire in the publicly traded market, underscoring a complete breakdown in cost control and operational efficiency. Compounding the problem, NAKA's cash flow from operations turned negative, with a -$1.91 million outflow, raising urgent questions about its ability to fund even basic operations without external financing[1].

The situation is further exacerbated by a troubling pattern of losses. Over the past four quarters, NAKANAKA-- has posted a cumulative net loss of $3.62 million, with a recent Q2 2025 earnings report showing a loss of $0.35 per share—well below analyst expectations[3]. Meanwhile, the company's price-to-sales ratio of 9.44 appears disconnected from reality, given its inability to translate revenue into profitability[1].

Strategic Missteps and Investor Fatigue

NAKA's recent strategic moves have only deepened investor skepticism. The company's $30 million investment in Metaplanet, a metaverse-related venture, has been widely criticized as a desperate attempt to pivot without a clear value proposition[1]. Equally damaging was the announcement of a $5 billion at-the-market equity offering program, which triggered a 22% drop in share price as investors bristled at the prospect of aggressive dilution[1].

The company's flirtation with BitcoinBTC-- treasury strategies has also backfired. While some firms have successfully leveraged crypto holdings to generate returns, NAKA's approach has been perceived as a gimmick. As noted in a recent analysis, “investor exhaustion toward Bitcoin treasury companies is palpable, and NAKA's lack of operational improvements has only accelerated this trend”[3]. This strategy has failed to address core weaknesses, leaving the company reliant on speculative bets rather than sustainable revenue streams.

Market Sentiment and Analyst Outlook

The market's reaction has been swift and unforgiving. NAKA's stock has lost over half its value in a single trading day, with the share price falling to $1.28 on September 15—a level that raises concerns about insolvency risks[3]. Analysts have echoed these worries, citing “poor profitability, high valuation, and strategic uncertainties” as key risks[3]. The company's gross margin of 100%, while technically a positive metric, is misleading in this context, as it fails to account for the massive operational and financial losses eroding shareholder value[2].

Conclusion: A High-Risk Proposition

For investors, NAKA represents a high-risk, high-volatility proposition with little downside protection. The company's deteriorating fundamentals—marked by unsustainable losses, liquidity challenges, and a lack of credible strategic direction—suggest a prolonged period of instability. While speculative rebounds are always possible in such scenarios, the absence of a clear path to profitability or operational turnaround makes NAKA a perilous bet.

In the absence of material improvements, NAKA's trajectory appears set for further declines. As one market observer aptly put it, “this is a case study in how not to manage a public company”[1]. For now, caution—and perhaps a hard pass—is warranted.

Comentarios

Aún no hay comentarios