Municipal Bond Income Strategies in a High-Interest-Rate Environment: Assessing PIMCO California Municipal Income Fund's Dividend Resilience

In a world where central banks have aggressively raised interest rates to combat inflation, income-focused investors face a paradox: higher yields on cash and short-term bonds, but heightened risks for long-term fixed-income strategies. For tax-conscious investors in high-tax states like California, municipal bonds remain a critical tool. The PIMCO California Municipal Income Fund (PCQ) has emerged as a focal point in this landscape, offering a recent $0.036 monthly dividend that appears resilient despite macroeconomic headwinds. This article evaluates the fund's dividend consistency, its investment strategy, and its ability to sustain yields in a high-rate environment.

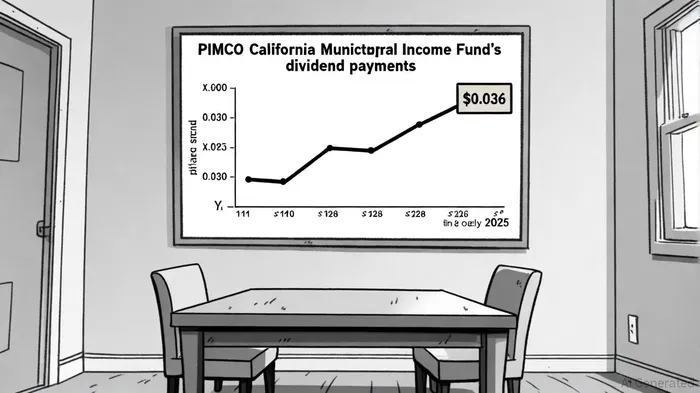

Dividend Consistency: A Shield Against Volatility

PCQ's recent $0.036 per share dividend, paid monthly, has shown remarkable consistency. From May to September 2025, the fund maintained this exact payout, translating to an annualized dividend of $0.432 and a trailing twelve-month yield of 2.86% as of October 1, 2025, according to the PCQ dividend history. This stability contrasts with broader market turbulence, where rising rates have pressured municipal bond prices. While the fund's dividend yield has fluctuated historically-ranging from 0.356% to 0.411% in early 2025-its monthly cadence and fixed amount suggest a disciplined approach to income generation, according to PIMCO's Municipal Income Opportunity.

However, the fund's earnings per share (EPS) tell a more complex story. PCQPCQ-- reported a negative EPS of -$0.62 in recent filings, raising questions about its payout ratio of 6.40% (per the PCQ dividend history). This discrepancy highlights the reliance on retained earnings and active management to sustain dividends, a strategy that may face strain if interest rates remain elevated for extended periods.

Investment Strategy: Balancing Yield and Credit Quality

PIMCO's tax-efficient investing materials indicate the fund employs active management to "lock in attractive bond yields" and adjust duration exposure based on rate forecasts. This approach leverages PIMCO's extensive credit research, ensuring a minimum average portfolio quality of AA- and avoiding alternative minimum tax (AMT) exposure, per PIMCO's managed-account materials.

In a high-interest-rate environment, the fund's flexibility to reposition across the yield curve becomes critical. For instance, PCQ may selectively invest in high-yield municipal bonds through vehicles like PIMCO Fixed Income Shares (FISH), balancing risk and return, rather than following a passive strategy that may struggle to adapt to shifting rate expectations.

Yield Sustainability: A Comparative Lens

While PCQ's dividend appears robust, its sustainability must be viewed through a comparative lens. Sibling funds like PIMCO California Municipal Income Fund II (PCK) have shown declining trends, with a 5-year average dividend growth rate of -7.65% and a low Dividend Sustainability Score (DSS), according to PCK dividends. In contrast, PCQ's 6.15% yield as of July 2025, per PIMCO's materials, outperforms PCK's struggling performance, suggesting stronger management discipline.

Yet, challenges persist. The fund's negative EPS underscores the fragility of its payout model, particularly if municipal bond spreads compress further. Additionally, global economic risks-such as a potential recession-could pressure state and local governments to delay bond repayments, indirectly affecting PCQ's income streams, as noted in the PCQ dividend history.

Conclusion: A Prudent Bet with Caveats

PCQ's $0.036 dividend reflects a blend of strategic agility and tax efficiency, making it a compelling option for California residents seeking income in a high-rate environment. Its active management and focus on credit quality provide a buffer against market volatility. However, the fund's negative EPS and reliance on retained earnings highlight the need for caution. Investors should monitor PIMCO's ability to navigate rate normalization and maintain its current payout, especially as central banks hint at potential rate cuts in 2026.

For now, PCQ remains a standout in the municipal bond space, but its long-term appeal will depend on PIMCO's capacity to adapt to evolving macroeconomic conditions.

Comentarios

Aún no hay comentarios