Mortgage Rates Hover Below 7%: Navigating Volatility in a Tight Market

The U.S. mortgage market remains in a precarious balancing act, with the 30-year fixed-rate mortgage averaging 6.83% as of April 2025—just under the psychologically significant 7% threshold. While this represents a slight increase from the prior week, it underscores a fragile equilibrium shaped by geopolitical tensions, inflation fears, and shifting monetary policies. For investors, this environment offers both opportunities and risks, particularly for those in real estate, homebuilding, or fixed-income markets.

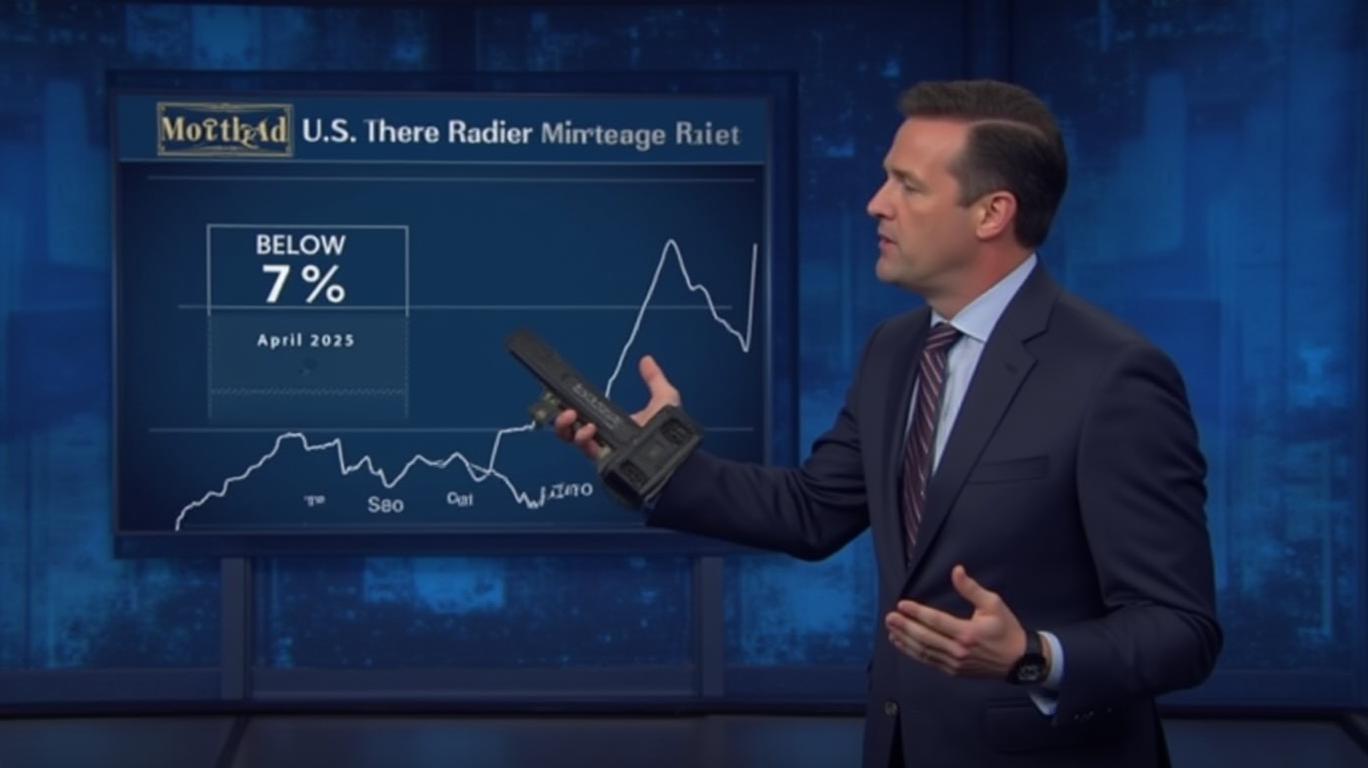

Current Rates: A Delicate Dance Around 7%

Freddie Mac’s April 18 report highlights the latest volatility, with the 30-year fixed rate rising 21 basis points week-over-week to 6.83%—its highest level since late 2023. While this is still below the 2024 peak of 7.57%, it reflects growing pressures from President Trump’s tariffs, which have stoked inflation fears and pushed bond yields higher. Meanwhile, Zillow’s data shows a slightly lower average of 6.71%, emphasizing the variability in how rates are reported across lenders and platforms.

This visualization reveals the tight correlation between mortgage rates and Treasury yields. As the 10-year Treasury yield surged to 4.15% in early April, mortgage rates followed suit—a reminder that bond market dynamics remain the primary driver.

What’s Driving the Volatility?

- Geopolitical Uncertainty: The administration’s April 2 tariffs on Chinese imports disrupted global supply chains, sparking fears of inflationary pressures. This has kept bond markets on edge, with yields spiking and dragging mortgage rates upward.

- Inflation Lingering: Despite Fed efforts to cool prices, core inflation remains elevated at 3.8% year-over-year, above the 2% target. Persistent inflation limits the likelihood of rate cuts, keeping mortgage rates elevated.

- Political Playbook: The administration’s stance on housing—such as subsidies for first-time buyers—has created uneven demand, with some markets overheating while others stagnate.

Investment Implications: Where to Look

Homebuilders: Riding Volatility or Bracing for a Crash?

Homebuilder stocks like D.R. Horton (DHI) and Lennar (LEN) have been volatile, reflecting both rising costs and shifting buyer sentiment.

The chart shows a clear inverse relationship: when rates dip below 7%, homebuilder stocks rally, but they stall when rates climb. Investors in this sector should consider hedging with inverse rate ETFs or focusing on companies with strong cash reserves.

Mortgage-Backed Securities (MBS): A Cautionary Tale

For fixed-income investors, MBS remain a staple, but their appeal hinges on rate stability. A sudden spike in rates could reduce the value of these securities, especially those tied to adjustable-rate mortgages (ARMs).

Real Estate ETFs: Diversification is Key

ETFs like the SPDR S&P 500 Real Estate ETF (XLK) offer exposure to a broad basket of real estate stocks. However, investors should pair these with inverse rate instruments to mitigate risk.

Expert Forecasts: A Modest Downturn Ahead?

Despite the April surge, most experts see rates trending lower by year-end. The Mortgage Bankers Association (MBA) predicts the 30-year rate will average 6.7% by December 2025, while Bankrate’s survey of economists anticipates a 6.41% average. These projections assume the Fed holds rates steady and inflation eases—a scenario that hinges on global supply chains stabilizing and consumer spending cooling.

Risks on the Horizon

- Inflation Resurgence: If tariffs fuel a new wave of price hikes, the Fed may tighten further, pushing rates higher.

- Global Shocks: Geopolitical conflicts or energy crises could disrupt bond markets, leading to sudden rate spikes.

- Housing Market Correction: Rising rates have already slowed resale activity, with inventory at decade lows. A prolonged stagnation could hurt homebuilder valuations.

Conclusion: Caution Meets Opportunity

The mortgage market’s flirtation with 7% underscores its vulnerability to external shocks, but it also presents strategic entry points. Investors in real estate or homebuilders should prioritize diversification and hedging. Meanwhile, fixed-income investors might consider short-term MBS or inverse rate products to insulate portfolios.

The data is clear: the 6.83% rate as of April 2025 remains a hard-won reprieve from 2024’s highs, but it’s not a guarantee of stability. With inflation and policy risks lingering, investors must stay nimble. As Freddie Mac’s historical data shows, the 30-year rate has averaged 7.72% since 1971—meaning today’s rates, while elevated, still offer a window of opportunity.

But don’t mistake this for a return to the 2021 lows of 2.65%. In this tight market, success hinges on discipline, hedging, and a keen eye on the geopolitical chessboard.

Comentarios

Aún no hay comentarios