MongoDB vs. ServiceNow: Which AI Software Stock Has Greater Upside?

MongoDB MDB and ServiceNow NOW are enterprise AI software companies positioned at the intersection of cloud infrastructure and intelligent automation. MongoDBMDB-- powers modern and AI-driven applications through its flexible, developer-focused cloud database platform, while ServiceNowNOW-- orchestrates enterprise workflows and governs AI agents at scale across global organizations. Both operate platform-based models where revenues expand as customers deepen adoption across broader use cases and workloads.

Per Mordor Intelligence, the global enterprise AI market is valued at $114.87 billion for 2026 and is projected to reach $273.08 billion by 2031 at a CAGR of 18.91%. This expansion is driven by enterprises moving from AI pilots into production deployments, rising demand for cloud-native data infrastructure and the accelerating commercialization of agentic AI workloads. As organizations scale intelligent applications, demand for both integrated database platforms and AI-powered workflow automation grows proportionately, positioning MongoDB and ServiceNow to benefit from the same structural tailwinds.

Let's delve deeper to determine which stock offers a greater upside.

The Case for MDB

MongoDB operates as a cloud database platform provider, with Atlas consolidating document storage, search, vector search and embeddings into a single fully managed system. The company has built meaningful scale in the cloud database market, yet softer fiscal 2027 guidance and the unmonetized nature of its newer AI capabilities present challenges that distinguish it from platforms where AI monetization is more broadly established.

Atlas is available through a free entry-level tier, which, while effective at driving developer mindshare, creates uncertainty around the pace at which new users convert into commercially meaningful relationships, making top-line growth more dependent on a narrower cohort of large enterprise accounts.

Voyage AI's embedding and reranking models have seen growing customer adoption since the acquisition, yet their revenue contribution remains insignificant, and the product is not expected to be a meaningful contributor in the near term. Being a consumption-based business, MongoDB's revenue is directly tied to how aggressively customers expand workloads on Atlas, introducing visibility risk that subscription-based peers do not face to the same degree. Fiscal 2027 revenue growth is guided at 16% to 18%, nearly 600 basis points below fiscal 2026's pace, reflecting the weight of these dynamics on the near-term outlook.

.

The Zacks Consensus Estimate for MDB's fiscal 2027 EPS is pegged at $5.82, up 3.74% over the past 30 days, indicating year-over-year growth of 17.1%.

The Case for NOW

ServiceNow operates as an enterprise AI platform provider, with its workflow automation and orchestration capabilities serving as the operating layer through which enterprises govern, deploy and scale AI agents across complex business processes. The platform's subscription-based model, anchored by deep workflow integration across IT, human resources and customer service functions, creates a structurally recurring revenue base that is difficult to displace once embedded within an organization's core operations.

Now Assist benefits from being layered onto an existing and deeply embedded customer base, allowing ServiceNow to capture incremental AI spend through renewal upsell rather than new customer acquisition. The $600 million in annual contract value crossed in the fourth quarter of 2025, and the trajectory toward $1 billion in 2026 reflects this dynamic playing out at scale.

However, ServiceNow's acquisition strategy has created near-term uncertainty around the financial outlook. Moveworks, while already integrated, is yet to make a meaningful revenue contribution. Armis, pending close in the early second half of 2026, is expected to create up to 50 basis points of operating margin headwind even before full integration begins. With both acquisitions at different stages of maturity, the monetization path across each asset is likely to remain uncertain in the near term.

The Zacks Consensus Estimate for NOW's 2026 EPS is pegged at $4.12, down by a penny over the past 30 days, suggesting year-over-year growth of 17.38%.

ServiceNow, Inc. Price and Consensus

ServiceNow, Inc. price-consensus-chart | ServiceNow, Inc. Quote

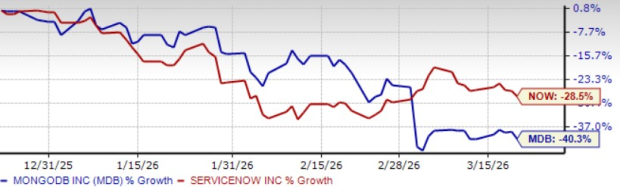

Price Performance and Valuation of MDBMDB-- and NOW

Over the past three months, MongoDB shares have plunged 40.3% while ServiceNow shares have declined 28.5%. ServiceNow's relative resilience reflects the strength of its underlying business fundamentals, with AI monetization gaining measurable traction through Now Assist. MongoDB's steeper decline aligns with softer fiscal 2027 guidance and the unmonetized nature of its AI capabilities at this stage.

MDB vs. NOW Price Performance

Image Source: Zacks Investment Research

On a forward 12-month price-to-sales basis, ServiceNow trades at 6.95x against MongoDB's 7.1x. With active AI monetization through Now Assist and a deeply embedded subscription model, ServiceNow's multiple appears more justified relative to MongoDB, which trades at a modest premium despite softer growth guidance and an AI investment cycle yet to translate into revenue.

MDB vs. NOW Valuation

Image Source: Zacks Investment Research

Conclusion

ServiceNow's subscription-based model, deeply embedded enterprise workflows and actively monetizing Now Assist suite present a fundamentally sound and compounding growth profile. MongoDB, while a credible cloud database platform, has softer fiscal 2027 guidance and an AI investment cycle whose near-term revenue contribution remains uncertain.

These dynamics give ServiceNow a clearer edge over MDB. With NOW carrying a Zacks Rank #3 (Hold) against MDB's Zacks Rank #5 (Strong Sell), ServiceNow emerges as the more compelling pick. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

MongoDB, Inc. (MDB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios