U.S. Monetary Policy in 2025: Small Business Sentiment and Labor Market Revisions Shape Fed Strategy and Investment Opportunities

The U.S. Federal Reserve's policy trajectory in 2025 is increasingly shaped by a delicate interplay between small business sentiment and labor market dynamics. As the central bank navigates its dual mandate of price stability and maximum employment, recent data reveals a nuanced picture of economic resilience and fragility. Small businesses—often the barometer of economic health—have shown modest optimism amid easing credit conditions, while labor market revisions and trade policy shifts have intensified expectations for monetary easing. For investors, these developments signal both risks and opportunities across key sectors.

Small Business Sentiment: A Mixed Signal of Resilience and Constraints

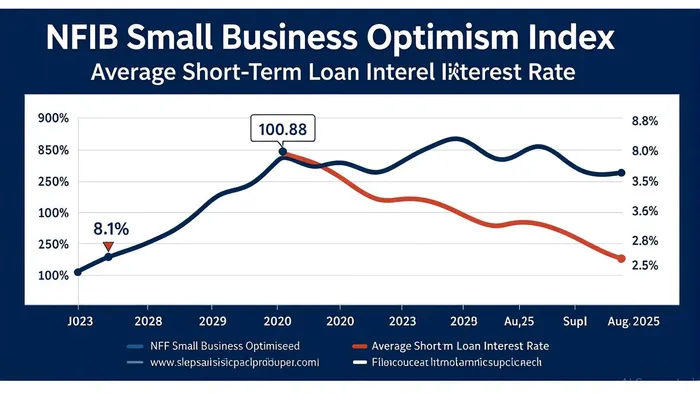

According to a report by the National Federation of Independent Business (NFIB), the Small Business Optimism Index rose to 100.8 in August 2025, slightly above its long-term average[1]. This improvement was driven by stronger expectations for real sales volumes, with 14% of small business owners rating their business health as “excellent” and 54% as “good”[2]. However, persistent challenges remain. Labor quality continues to be the top concern, with 32% of owners reporting unfilled job openings—a decline from previous months but still a significant drag on growth[3].

The easing of borrowing costs has provided some relief. The average rate paid on short-term loans fell to 8.1% in August 2025, the lowest since May 2023[4]. Yet, only 23% of small business owners reported regular borrowing, underscoring limited access to credit for newer or smaller firms[5]. This suggests that while the Fed's rate cuts are gradually filtering through the economy, their stimulative effects remain constrained by structural credit barriers.

Labor Market Revisions and Trade Policy: A Catalyst for Fed Action

Recent labor market data has further complicated the Fed's calculus. Preliminary benchmark revisions from the Bureau of Labor Statistics (BLS) revealed that U.S. job growth through March 2025 was 911,000 lower than initially estimated[6]. This downward revision, coupled with a sharp slowdown in August 2025—where only 22,000 jobs were added—has pushed the unemployment rate to 4.3%, the highest since 2021[7]. The New York Fed's Survey of Consumer Expectations also highlights a record low probability (44.9%) of finding a new job after job loss, signaling a shift from the high labor mobility of the “Great Resignation” era[8].

Trade policy shifts have exacerbated these labor market strains. Tariff hikes in 2025, which raised the average U.S. tariff rate to its highest level since the 1930s, have introduced stagflationary risks[9]. Small businesses, particularly in construction and retail, face rising operational costs and supply chain disruptions[10]. These pressures have pushed the Fed toward a more accommodative stance, with markets pricing in a 99% probability of a 25-basis-point rate cut in September 2025[11].

Investment Opportunities in a Shifting Policy Landscape

The anticipated easing cycle opens doors for sector-specific investments. Technology is a prime beneficiary, as lower borrowing costs reduce the cost of capital for growth-oriented firms. Companies in AI infrastructure and chip development, which rely heavily on R&D funding, stand to gain from reduced discount rates for future cash flows[12].

The housing sector is also poised for a rebound. With mortgage rates expected to decline alongside Fed rate cuts, demand for new homes could surge, benefiting homebuilders like LennarLEN-- and D.R. Horton[13]. Similarly, the consumer discretionary sector may see a boost as cheaper borrowing costs encourage spending on non-essential goods and services[14].

However, investors must remain cautious. Political pressures, including former President Trump's public criticism of the Fed, could introduce volatility into rate cut expectations[15]. Additionally, labor market imbalances—such as the 10.5% unemployment rate for younger workers—highlight structural challenges that may persist even with monetary easing[16].

Conclusion

The Federal Reserve's 2025 policy trajectory is inextricably linked to the health of small businesses and the labor market. While modest gains in business sentiment and easing credit conditions offer hope, structural labor shortages and trade policy risks necessitate a cautious approach. For investors, the path forward lies in capitalizing on sectors poised to benefit from lower rates—technology, housing, and consumer discretionary—while remaining vigilant to geopolitical and policy uncertainties.

Comentarios

Aún no hay comentarios