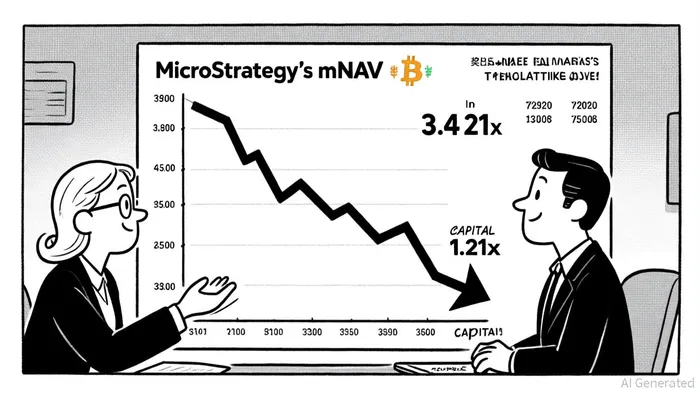

MicroStrategy's mNAV Compression: A Strategic Entry Point Amid Bitcoin's Long-Term Tailwinds

MicroStrategy (MSTR), now rebranded as "Strategy," has cemented its identity as the corporate world's most aggressive BitcoinBTC-- (BTC) accumulator. As of Q3 2025, the company holds 640,031 bitcoinsBTC--, valued at $73.21 billion in carrying value-nearly triple its $47.35 billion cost basis, according to a Panabee report. Yet, its stock trades at a historically compressed multiple to these holdings. With a market capitalization of $95 billion and a Bitcoin net asset value (NAV) of $78 billion, MicroStrategy's mNAV (market value to Bitcoin NAV ratio) stands at 1.21x, the lowest level in 19 months, according to a CoinRepublic article. This represents a stark contrast to the 3.4x peak observed in late 2024 and suggests a compelling entry point for investors seeking Bitcoin exposure through a uniquely structured equity vehicle.

The mNAV Metric: A Barometer of Investor Sentiment

The mNAV, calculated as MicroStrategy's enterprise value divided by the market value of its Bitcoin holdings, has long served as a proxy for market sentiment toward the company's Bitcoin-centric strategy. Historically, the metric followed a slow exponential curve, rising from 1.8x in 2022 to 2.1x in May 2025 before collapsing to 1.62x in August 2025, according to an mNAV analysis. The current 1.21x level reflects a flight to caution, driven by concerns over equity dilution, debt servicing costs, and Bitcoin's volatility.

This compression is particularly striking given Bitcoin's year-to-date performance. While BTC gained 31%, MicroStrategy's shares rose only 13.3%, widening the gap between the asset and its proxy (reported by CoinRepublic). The disconnect underscores a weakening flywheel effect-the self-reinforcing cycle of capital raising, Bitcoin accumulation, and valuation expansion that once defined MicroStrategy's growth. Yet, for long-term investors, this discount may represent a mispricing opportunity.

Strategic Implications of the Discount

MicroStrategy's balance sheet remains robust, with $5.09 billion in Q3 2025 capital raises funding its Bitcoin purchases (Panabee). However, its $8.24 billion in debt and $6.59 billion in preferred stock create annualized fixed charges exceeding $673 million (Panabee). These obligations amplify downside risk in a bear market but also highlight the company's commitment to maintaining its position as the largest corporate Bitcoin holder (over 2.5% of total supply), as noted in a Brave New Coin insight.

The recent adoption of ASU 2023-08 accounting standards has further amplified volatility in reported earnings by mandating the recognition of unrealized gains and losses on Bitcoin holdings (Panabee). While this transparency is beneficial, it has contributed to a negative earnings trajectory, with Q3 2025 reporting a $16.49 loss per share-a 5,219% decline year-over-year, reported by a Protos report. Regulatory clarity, such as the IRS's exclusion of unrealized gains from Adjusted Financial Statement Income (AFSI), has mitigated CAMT risks (Panabee), but market participants remain wary of leveraged exposure.

Investment Case: Capturing Bitcoin's Tailwinds at a Discount

The current mNAV compression offers a unique opportunity to gain Bitcoin exposure at a significant discount to intrinsic value. For context, MicroStrategy's 25% Bitcoin yield in 2025-measured as growth in Bitcoin holdings per share-demonstrates the effectiveness of its capital-raising strategy (Brave New Coin). While larger purchases are now required to sustain this yield, the company's cost basis ($73,983 per BTC) remains well below the $115,959 average acquisition price in Q3 2025 (Panabee), providing a buffer against near-term price declines.

Moreover, MicroStrategy's transformation into a Bitcoin treasury company has inspired over 161 publicly traded firms to adopt digital assets (Brave New Coin), creating a network effect that could drive broader institutional adoption. The recent passage of the GENIUS and CLARITY Acts (Brave New Coin) further reduces regulatory uncertainty, potentially attracting new capital to the space. For investors, this aligns with Bitcoin's long-term tailwinds-scarcity, institutional acceptance, and macroeconomic hedges-while leveraging MicroStrategy's operational expertise in capital allocation.

Risks and Considerations

Critics argue that MicroStrategy's model is inherently fragile. Its software business generates less than $350 million in trailing 12-month gross profit (CoinRepublic), making the stock increasingly a bet on Bitcoin rather than operational performance. Additionally, the company's reliance on capital markets exposes it to liquidity risks; a market downturn could force sales of Bitcoin at a loss or higher borrowing costs. Insider selling and dilutive share offerings have also eroded shareholder confidence, with the company revising its mNAV guidance to permit dilution "when otherwise deemed advantageous" (Protos).

Conclusion: A Calculated Bet on Bitcoin's Future

MicroStrategy's 1.21x mNAV represents a historically weak valuation metric, offering a compelling entry point for investors who believe in Bitcoin's long-term trajectory. While risks such as leverage and operational fragility persist, the company's strategic position as the largest corporate Bitcoin holder, combined with regulatory tailwinds, strengthens its case as a leveraged play on the digital asset. For those willing to navigate short-term volatility, the current discount may provide an asymmetric opportunity to capture Bitcoin's upside through a uniquely structured equity vehicle.

Comentarios

Aún no hay comentarios