Mexico's Monetary Easing and Its Implications for Emerging Market Bonds

Mexico's monetary easing cycle, initiated by the Bank of Mexico (Banxico) in early 2024, has reshaped the landscape of emerging market (EM) debt. By March 2025, Banxico had cut its benchmark rate by 50 basis points to 9.00%, followed by another 50-basis-point reduction in June 2025, bringing the rate to 8.00%—the lowest in nearly three years[5]. These cuts, driven by disinflationary trends and economic uncertainty, have had profound structural effects on local-currency bond yields and investor positioning in EM debt markets.

Structural Impacts on Local-Currency Bond Yields

Mexico's rate cuts have not led to a collapse in bond yields, as might be expected in a typical liquidity-driven environment. Instead, the country's 10-year local-currency bond yield remains elevated at 8.80% as of Q3 2025[4], reflecting a unique interplay of inflation expectations, liquidity premia, and global capital flows. According to a report by BBVA Research, Mexico's high nominal rates—combined with a weakening U.S. dollar—have made peso-denominated assets particularly attractive for yield-starved investors[4]. This dynamic is further amplified by Mexico's status as the highest-yielding sovereign issuer among Latin America's investment-grade countries, with real interest rates (adjusted for inflation) placing it second in the region after Brazil[4].

However, structural challenges persist. Academic analysis reveals that liquidity premia in Mexico's bond market, particularly for inflation-indexed udibonos, remain volatile and higher than those for nominal bonds[1]. This reflects the less liquid nature of real-return securities in EM markets, where foreign investor participation and capital account openness play critical roles. For instance, while Colombia and Hungary have seen narrower yield spreads due to stable exchange rates and robust foreign ownership, Mexico's bond yields remain more sensitive to global risk premiums and oil price fluctuations[3].

Investor Positioning and Capital Flows

The prolonged rate-cutting cycle has also altered investor positioning in EM debt. As the U.S. Federal Reserve signals the end of its hiking cycle, capital has flowed into EM bonds, with Mexico emerging as a key beneficiary. Data from AllianzGI indicates that Mexico's local-currency bonds have outperformed hard-currency EM debt in 2024, driven by declining yields and favorable currency movements[5]. Foreign investors, particularly those seeking inflation-linked returns, have flocked to Mexico's udibonos, which now represent a significant portion of major EM benchmarks[2].

Yet, this inflow is not without risks. The Mexican corporate bond market, while active, faces challenges in managing maturities. For example, non-financial entities face MXN694 billion in outstanding debt, with major issuers like CFE and AMX confronting large refinancing needs in 2025[3]. Additionally, geopolitical risks—such as U.S. tariff threats—introduce volatility, as seen in Brazil and South Africa, where trade uncertainties have dented credit quality[2].

Comparative Insights and Future Outlook

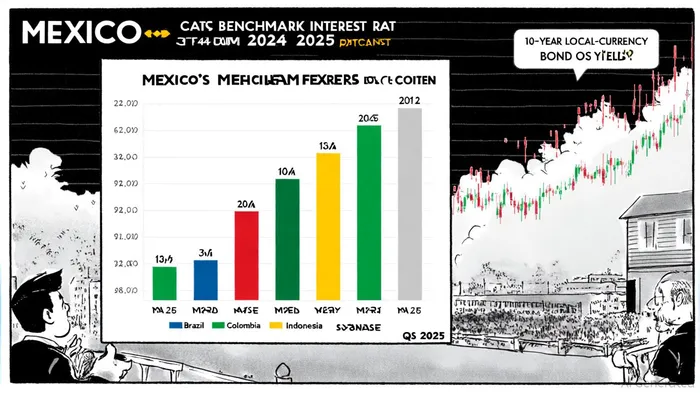

Comparing Mexico's trajectory to other EMs highlights its cautious approach. While Brazil has slashed rates more aggressively (from 15% to 8.5% by late 2025), Mexico's central bank has maintained a neutral stance relative to the Fed funds rate, prioritizing peso stability[1]. This has allowed Mexico to balance disinflation with fiscal prudence, avoiding the sharp yield spikes seen in Indonesia and Peru, where exchange rate volatility has pushed local-currency yields above foreign-currency counterparts[3].

Looking ahead, BBVA Research forecasts the policy rate could reach 7.25% by year-end 2025[6], further compressing yields. However, structural factors—such as liquidity constraints and inflation risk premia—will likely keep Mexico's bond yields elevated compared to advanced economies. The EMBI spread, a key metric for EM risk, underscores this: Mexico's spread remains lower than Venezuela's 254% but higher than Colombia's, reflecting its intermediate risk profile[1].

Conclusion

Mexico's monetary easing has created a paradox: high yields persist despite aggressive rate cuts, driven by a mix of inflation-linked demand, dollar weakness, and EM investors' appetite for risk. While this environment has bolstered Mexico's bond market, structural challenges—liquidity premia, geopolitical risks, and refinancing pressures—demand careful navigation. For investors, Mexico offers a compelling case study in how prolonged rate cuts can reshape EM debt dynamics, balancing yield opportunities with the inherent volatility of emerging markets.

Comentarios

Aún no hay comentarios