Metaplanet's Bitcoin Treasury Play: Assessing Capital Efficiency and Risk-Adjusted Returns via Perpetual Preferred Shares

In the evolving landscape of corporate BitcoinBTC-- treasury strategies, Metaplanet has emerged as a bold innovator, leveraging perpetual preferred shares to fund its aggressive Bitcoin accumulation. As of September 2025, the Tokyo-based firm holds 20,136 BTC in its treasury, acquired at an average cost of $103,196 per Bitcoin, with a total acquisition cost of $2.08 billion, according to Metaplanet's treasury analytics. This strategic shift, which mirrors but diverges from MicroStrategy's (now Strategy) debt-driven approach, raises critical questions about capital efficiency and risk-adjusted returns.

Capital Efficiency: A Structured Approach to Bitcoin Accumulation

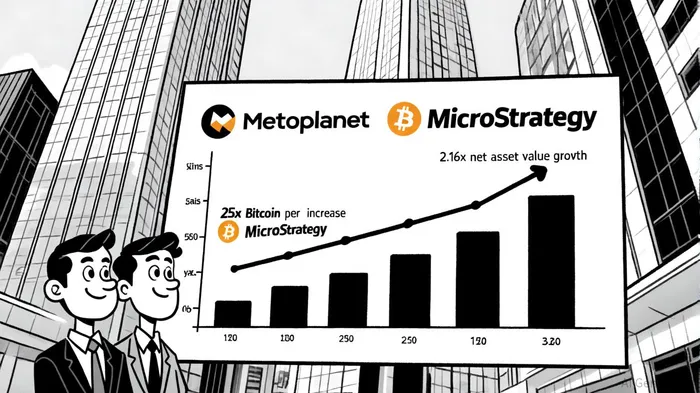

Metaplanet's use of perpetual preferred shares-offering up to 6% dividends-allows the company to raise capital without diluting common equity or increasing leverage ratios. Unlike traditional equity or debt instruments, these shares lack a maturity date and can be redeemed strategically, providing flexibility in Japan's low-interest-rate environment. For instance, the company's ¥555 billion shelf registration in 2025 enabled it to issue Class A and Class B perpetual preferred shares, with the latter including a put option for conversion into common stock, as described in a Blockspace analysis. This structure has allowed Metaplanet to grow its Bitcoin holdings 25x in one year, outpacing even Strategy's 2.16x NAV growth, according to Bitcoin Magazine.

The firm's capital efficiency is further amplified by its use of zero-interest bonds and options strategies, such as selling cash-secured put options, to acquire Bitcoin at favorable prices, as noted in a Cointelegraph analysis. By converting all proceeds to Bitcoin within 72 hours, Metaplanet minimizes exposure to fiat volatility while maintaining a clean capital structure. In contrast, Strategy's reliance on convertible bonds and preferred stock (e.g., STRKSTRK-- with 8% dividends) has led to higher leverage but slower NAV growth, according to a CCN comparison.

Risk-Adjusted Returns: Balancing Yield and Volatility

While Metaplanet's Bitcoin treasury strategyMSTR-- has driven a 170% BTC Yield in Q1 2025, per OKX, its risk profile remains complex. Perpetual preferred shares expose the company to interest rate sensitivity, as rising rates could reduce the present value of future dividends. Additionally, Bitcoin's price volatility-currently at a 12-month low of $28,500-poses challenges for maintaining dividend obligations, as reported by Yahoo Finance.

Despite these risks, Metaplanet's approach has generated a premium to net asset value (NAV) of 2.86x, reflecting strong investor confidence, per Coinotag. This contrasts with Strategy's 1.69x NAV multiple, suggesting that Metaplanet's disciplined capital sourcing and operational profitability (e.g., ¥592M operating profit in Q1 2025), as reported by BitPylon, are rewarded by the market. However, the absence of a publicly available Sharpe ratio for Metaplanet complicates direct comparisons with Strategy's 91st-percentile rank in risk-adjusted returns, per PortfoliosLab.

Challenges and Strategic Considerations

Metaplanet's reliance on perpetual preferred shares introduces long-term obligations that could strain liquidity if Bitcoin prices stagnate or decline. For example, its $3.7 billion stock offering in August 2025 aims to fund a twelvefold increase in BTC holdings by 2027 but also locks in dividend payments that may become burdensome during market downturns, as CoinDesk reported. Conversely, Strategy's higher-yield preferred shares (e.g., STRFSTRF-- with 10% dividends) offer greater income potential but at the cost of increased leverage, as noted in a CCN analysis.

Another critical factor is regulatory uncertainty. Japan's evolving stance on corporate Bitcoin holdings and preferred share structures could impact Metaplanet's ability to scale its yield curve for institutional investors, according to vTrader. Meanwhile, Strategy's U.S.-centric model benefits from clearer regulatory frameworks but faces scrutiny over its debt-heavy balance sheet.

Conclusion: A High-Stakes Bet on Bitcoin's Future

Metaplanet's perpetual preferred share strategy exemplifies the growing intersection of traditional finance and crypto. By prioritizing capital efficiency and disciplined accumulation, the firm has positioned itself as a formidable player in the Bitcoin treasury space. However, investors must weigh the potential for asymmetric returns against risks such as interest rate shifts, Bitcoin volatility, and regulatory headwinds.

As corporate Bitcoin adoption accelerates, Metaplanet's approach-while distinct from Strategy's-offers a compelling case study in balancing innovation with prudence. For those willing to navigate the complexities of perpetual preferred shares, the rewards could be substantial, provided Bitcoin's long-term value proposition holds.

Comentarios

Aún no hay comentarios