Meta's Nuclear Moat: Securing the Energy Layer for the AI S-Curve

The AI boom is hitting a fundamental wall: electricity. As models evolve from simple tools into continuous, agentic systems, the power demand is set to explode. Energy consultants project that AI-driven data centers alone will drive at least a 30% increase in U.S. power usage by 2030. This isn't a minor uptick; it's a paradigm shift that threatens to cap the growth of the entire industry. The bottleneck is clear: the grid must provide not just more power, but the right kind.

That "right kind" is firm, baseload power. Unlike intermittent solar or wind, nuclear energy offers a constant, reliable supply. For Meta's vision of running advanced AI systems 24/7, this consistency is non-negotiable. Grid instability or price volatility could halt operations, making energy independence a strategic imperative, not a sustainability footnote.

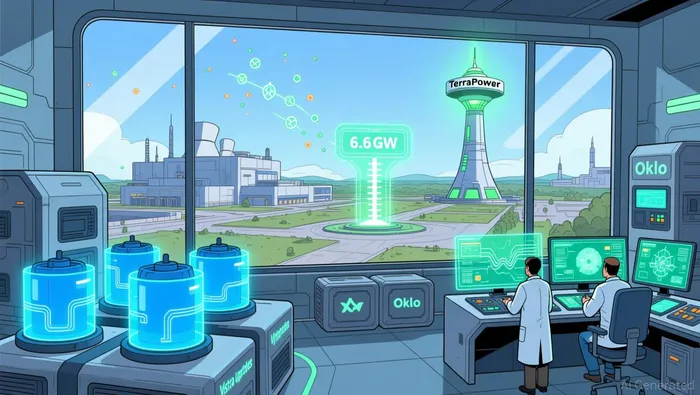

Meta is betting big to secure this layer. The company has committed to a 6.6 gigawatt portfolio of nuclear power by 2035, a plan that dwarfs previous corporate deals. This isn't a series of small, incremental purchases. It's a first-mover infrastructure play, locking in capacity across existing plants, new advanced reactors, and even funding the development of next-generation technology. By entering definitive agreements in early January, MetaMETA-- is positioning itself ahead of the curve, building the fundamental rails for the next exponential growth phase. The scale is staggering: 6 gigawatts is enough to power a city of about 5 million homes. In essence, Meta is commissioning a utility-scale power plant for its own operations, creating a private energy pipeline that forms a critical competitive moat.

The Infrastructure Play: A Capital-Efficient Moat

Meta's nuclear deals are less about buying power and more about building a foundational infrastructure layer. The structure of these agreements reveals a sophisticated, long-term investment that de-risks advanced nuclear deployment while securing a dedicated energy pipeline for its AI ambitions.

The core of the strategy is a mix of 20-year power purchase agreements (PPAs) with Vistra for existing plant uprates and capital-efficient prepayments to fund new advanced reactors at Oklo and TerraPower. This dual-track approach is key. The PPAs lock in a steady, reliable supply from proven assets, directly addressing the immediate need for firm power. Simultaneously, the prepayments act as anchor funding for nascent technologies, providing the financial certainty that developers need to move from concept to construction. By committing capital upfront, Meta is effectively subsidizing the first-mover risk of building new reactor types.

Critically, this model is designed to be capital-efficient for Meta itself. The company avoids taking on new debt or diluting shareholders to fund these massive projects. Instead, it uses its balance sheet to secure long-term energy at a fixed price, converting a future operational cost into a strategic investment. This creates a private energy pipeline that insulates the company from grid volatility and price spikes, a crucial advantage for running advanced AI systems that demand uninterrupted power.

Meta's role as a major corporate anchor customer is the linchpin. By stepping forward with definitive agreements for up to 6.6 gigawatts, the company de-risks the entire supply chain. It provides a guaranteed market for new nuclear output, making projects more bankable and accelerating deployment. This is a foundational technology play; Meta isn't just a buyer, it's a co-developer of the energy infrastructure that will underpin the AI paradigm. The scale of its commitment signals to the market that the energy bottleneck is solvable, potentially catalyzing broader investment and regulatory support. In doing so, Meta is building a moat not just around its data centers, but around the very energy layer that will power the next exponential growth phase.

Strategic Impact and Market Validation

The true measure of a strategic bet is the market's verdict. Meta's nuclear push has already drawn a powerful validation signal. On the day the deals were announced, Vistra shares climbed 10% and Oklo shares gained 8%. Meta's own stock closed 1% higher. This isn't just a routine market tick; it's a clear vote of confidence in the company's infrastructure-first approach. Investors see the move as de-risking a critical, exponential growth phase.

The financial impact is twofold. First, it provides a massive shield against the volatility that threatens AI's capital-intensive build-out. By locking in 20-year power purchase agreements and funding new reactors, Meta converts a variable operational cost into a predictable, long-term capital expenditure. This cost predictability is essential for planning a multi-year, multi-billion dollar build-out of systems like the Prometheus supercluster. It insulates the company from the kind of price spikes that could derail a project or compress margins.

Second, the sheer scale suggests a strategic capital allocation shift. While Meta has spent billions on chips, this commitment represents a direct investment in the foundational energy layer. The 6.6 gigawatt portfolio is a multi-billion dollar commitment, dwarfing previous corporate clean-energy deals. This pivot signals that management views energy independence as a non-negotiable requirement for growth, not a secondary sustainability goal. It's a first-mover bet on the infrastructure that will enable the next S-curve of AI adoption.

The market reaction validates this as a moat-building play. By becoming a major anchor customer, Meta isn't just securing power; it's accelerating the deployment of advanced nuclear technology. This de-risks the entire supply chain, making projects more bankable and potentially catalyzing broader industry investment. In a race where the next bottleneck is already emerging, Meta is using its balance sheet to build the rails before the train arrives.

Catalysts, Risks, and the Path to Exponential Adoption

The path from announcement to a functioning energy moat is paved with specific milestones and significant uncertainties. For Meta's bet to pay off, the company must navigate a complex timeline where technical execution meets regulatory and market realities.

The first major catalyst is the start of power deliveries. The 20-year agreements with Vistra for uprated existing plants are the most immediate source. While exact start dates are not in the evidence, these projects are typically faster to deploy than new builds. The real test of the advanced reactor strategy will be the construction milestones for the two new Natrium units at TerraPower and the small reactors at Oklo. The company has committed to funding these via prepayments, but the timeline for construction and commissioning is critical. Any delays here would push back the full benefit of the 6.6-gigawatt portfolio, potentially leaving Meta exposed to grid constraints during peak AI build-out phases.

Major risks loom on this path. Regulatory delays are the most predictable hurdle for new nuclear builds. The process for licensing and permitting advanced reactors is complex and time-consuming, even with a committed anchor customer. Cost overruns are another well-documented risk in the nuclear sector, which could strain the capital-efficient model Meta is counting on. Furthermore, even with a massive increase in supply, grid congestion remains a potential bottleneck. Adding gigawatts of power to a local grid requires significant upgrades to transmission infrastructure, a process that may lag behind generation capacity.

The ultimate variable is whether Meta can replicate this model. Its U.S.-focused nuclear RFP process was a masterstroke in creating a competitive, definitive market. If other tech giants follow suit, it could accelerate deployment and drive down costs through economies of scale. But if they wait, the supply chain may not be ready to meet a broader surge in demand. Policy shifts are the wildcard here. Supportive federal and state policies that streamline permitting and provide loan guarantees could dramatically accelerate the advanced nuclear deployment timeline, directly fueling the AI S-curve. Conversely, regulatory backtracking or political opposition could stall the entire industry, turning Meta's first-mover bet into a stranded asset.

The bottom line is that Meta has built a powerful infrastructure moat, but its value will compound only if the company successfully navigates these catalysts and risks. The next few years will show whether this is a foundational investment in the energy layer of the AI paradigm or a costly detour.

Comentarios

Aún no hay comentarios