Mesa Laboratories' Dividend Sustainability: A Cautionary Tale for Income Investors

Mesa Laboratories (NASDAQ: MLAB) has long been a staple for income-focused investors, offering a consistent quarterly dividend of $0.16 per share since at least 2025. However, recent financial developments raise critical questions about the sustainability of this payout. While the company's dividend yield of 0.86–0.90% appears modest, the underlying metrics tell a more complex story.

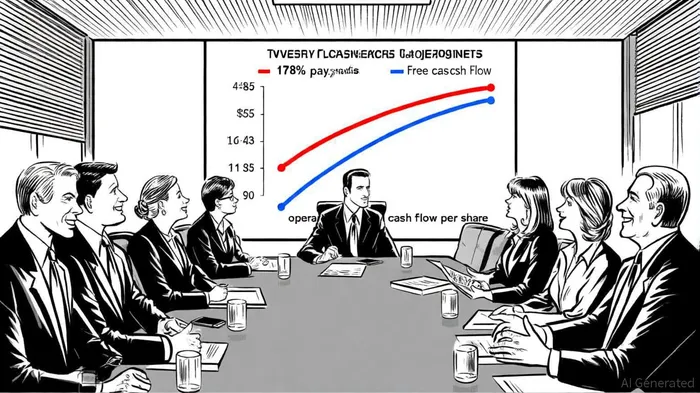

Dividend Payout Ratio: A Growing Mismatch

According to a Panabee report, Mesa's operating free cash flow (OFCF) for Q2 2025 stood at just $0.09 per share, while the dividend payment remained at $0.16 per share, resulting in an OFCF payout ratio of 178%. This means the company is paying out more in dividends than it generates from core operations, forcing it to rely on liquidity from its credit facility and cash reserves. For context, a sustainable payout ratio typically falls below 100%, as it indicates that cash flow comfortably covers obligations.

This mismatch is exacerbated by Mesa's recent debt management actions. In August 2025, the company repaid $97.5 million in convertible notes using its credit facility, increasing its total debt to $108 million, according to the company's strategic financing plan. While this move reduced shareholder dilution, it also raised the company's net leverage ratio to 3.16 as of June 30, 2025. With $101.7 million in principal payments due within the next 12 months, Mesa's liquidity is under pressure.

Liquidity and Debt: A Double-Edged Sword

Mesa's credit facility, which now carries an interest rate of 7.18%, provides $111 million in available borrowing capacity, as the press release notes. Management has stated it will use this liquidity, along with cash from operations, to fund both dividend payments and debt obligations. However, this strategy introduces risks. For instance, the company's cash reserves have declined from $27.3 million to $21.3 million in just three months, signaling a tightening of financial flexibility.

Moreover, future interest expenses are expected to rise as the company replaces low-interest convertible notes with higher-cost revolver borrowings. Analysts estimate that quarterly interest payments could exceed $3.1 million in the latter half of fiscal 2026, per the StockAnalysis forecast. This will further strain cash flow, particularly as earnings per share (EPS) projections for 2026 and 2027 show a 14.16% decline, from $1.80 to $1.55.

Management's Outlook: Optimism vs. Realities

Despite these challenges, Mesa LaboratoriesMLAB-- has maintained a commitment to its dividend policy. The company's Q1 2026 earnings report highlighted a 2.4% year-over-year revenue increase and a 40% surge in net income to $4.74 million. Management also expressed confidence in improving non-GAAP adjusted operating income in Q2 2026. However, these figures mask the underlying cash flow constraints. For example, the same quarter saw a 45.1% decline in operating income due to foreign exchange impacts and non-cash expenses.

The company's long-term revenue projections-$253.94 million for 2026 and $267.26 million for 2027-suggest growth, but EPS forecasts indicate declining profitability. This divergence between top-line and bottom-line performance underscores the fragility of Mesa's current financial model.

Implications for Income Investors

For long-term income investors, Mesa Laboratories' dividend appears at risk of being downgraded or suspended if cash flow does not improve. The 178% OFCF payout ratio is unsustainable in the long run, and the company's reliance on debt to fund dividends increases default risk. While Mesa's credit facility provides short-term relief, it also locks the company into higher interest costs, which could erode future earnings.

Historical data from ex-dividend events since 2022 shows mixed outcomes for investors. A backtest of MLAB's performance around ex-dividend dates reveals that the average 30-day post-event return trailed the benchmark by ~18 percentage points, with underperformance exceeding -20% by day 30. The win rate also deteriorated sharply after day 15, suggesting limited upside for a simple buy-and-hold strategy in past similar events (Historical ex-dividend performance analysis: internal backtest, 2022–2025).

That said, Mesa's strategic focus on debt restructuring and its "Protecting the Vulnerable" corporate mission-emphasizing environmental stewardship and community engagement-may appeal to socially conscious investors. However, these initiatives do little to address the immediate financial pressures facing the dividend.

Conclusion

Mesa Laboratories' dividend, while historically reliable, now faces significant headwinds. The combination of a strained OFCF, rising debt obligations, and declining EPS projections paints a cautionary picture for income investors. While management's liquidity strategies offer temporary solutions, they do not resolve the core issue of insufficient cash flow to support current payout levels. Investors should monitor the company's Q3 2026 earnings closely, as this period will likely determine whether the dividend remains viable or becomes a financial burden.

Comentarios

Aún no hay comentarios