Can Merck's New Drugs & Pipeline Ease Keytruda LOE Concerns?

Merck MRK is focusing on driving long-term growth through the newer products and a promising set of pipelines as its blockbuster PD-1 inhibitor, Keytruda, approaches patent expiration in 2028.

Keytruda, approved for several types of cancer, alone accounts for around 55% of the company’s pharmaceutical sales. The drug has played a key role in driving Merck’s steady revenue growth over the past few years. Keytruda recorded sales of $31.7 billion in 2025, up 7% year over year.

Though Keytruda intravenous is set to face loss of exclusivity in 2028, its sales are expected to stay strong until then. Management expects Keytruda to achieve peak sales of $35 billion by 2028 before it loses exclusivity.

On the fourth-quarter 2025 conference call, MerckMRK-- said that it projects more than $70 billion in potential non-risk-adjusted commercial opportunities from the current pipeline by the mid-2030s. Per management, this figure ($70 billion) is more than twice the prior peak consensus sales estimate of $35 billion for Keytruda in 2028 and represents a $20 billion increase from what the company had expected just a year ago.

Building on this optimism, Merck is pinning hopes on its new products and key pipeline progress to deliver sustainable growth in the post-Keytruda LOE period.

MRK’s phase III pipeline has almost tripled since 2021, supported by in-house pipeline progress as well as the addition of candidates through mergers and acquisitions (M&A) deals. Some key new products with blockbuster potential are its 21-valent pneumococcal conjugate vaccine, Capvaxive, and pulmonary arterial hypertension drug, Winrevair.

Capvaxive recorded sales of $759 million and Winrevair generated sales of $1.4 billion in 2025. Both products have witnessed a strong launch and have the potential to generate significant revenues over the long term.

MRK’s RSV antibody, Enflonsia (clesrovimab), was approved in the United States in June 2025, while it is under review in the European Union. A fixed-dose combination of doravirine and islatravir for the treatment of HIV is under review in the United States, with an FDA decision expected in April next month.

Merck has other promising candidates in its late-stage pipeline, such as enlicitide decanoate/MK-0616, an oral PCSK9 inhibitor for hypercholesterolemia, tulisokibart, a TL1A inhibitor for ulcerative colitis and Daiichi-Sankyo-partnered antibody-drug conjugates.

MRK has also made substantial investments in strategic M&A deals in recent times to build a more durable long-term portfolio.

Given the improving long-term outlook, Merck’s newer products and strong pipeline progress have boosted confidence that it may be able to sustain growth even after Keytruda loses exclusivity, while continuing to keep competition in check.

PD-L1 Inhibitors Competing With Keytruda

Keytruda faces competition from other PD-L1 inhibitors, including Bristol Myers’ BMY Opdivo, Roche’s RHHBY Tecentriq and AstraZeneca’s AZN Imfinzi.

BMY’s Opdivo, like Keytruda, is approved across multiple cancer types, including lung, melanoma and kidney cancers. Bristol Myers recorded $10.05 billion in Opdivo sales in 2025, up 8% year over year.

Tecentriq is Roche’s leading immuno-oncology drug approved for multiple cancer indications. RHHBY recorded CHF 3.56 billion in Tecentriq sales in 2025, up 3% year over year.

AZN’s Imfinzi generated sales of $6.06 billion in 2025, up 28%, driven by demand growth in bladder and liver cancer indications. Imfinzi has strategically expanded its use across multiple cancer indications, strengthening AstraZeneca’s oncology portfolio.

MRK's Price Performance, Valuation and Estimates

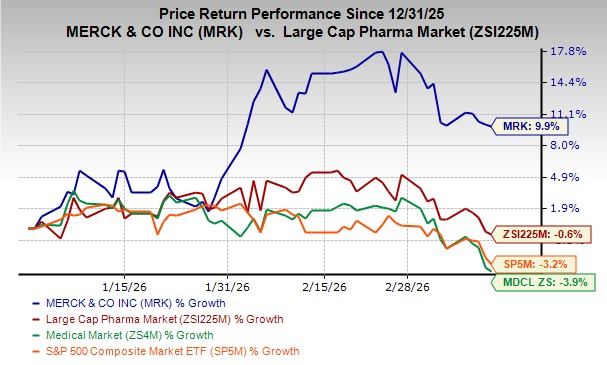

Year to date, shares of Merck have increased 9.9% against the industry’s 0.6% decline. The stock has also outperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

Image Source: Zacks Investment Research

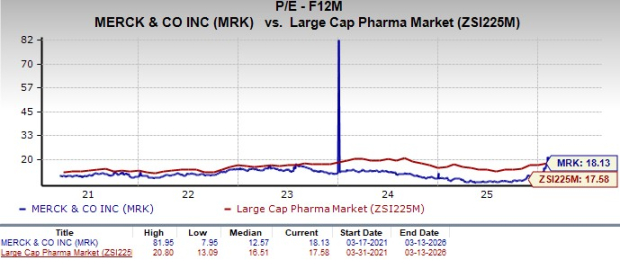

From a valuation standpoint, Merck is trading at a premium compared with the industry. Going by the price/earnings ratio, the company’s shares currently trade at 18.13 forward earnings, higher than 17.58 for the industry and its 5-year mean of 12.57.

Image Source: Zacks Investment Research

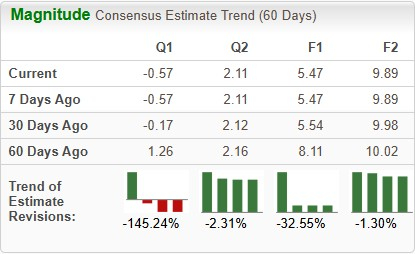

The Zacks Consensus Estimate for 2026 earnings per share has decreased from $5.54 to $5.47, while the same for 2027 has declined from $9.98 to $9.89 over the past 30 days.

Image Source: Zacks Investment Research

MRK’s Zacks Rank

Merck currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Roche Holding AG (RHHBY): Free Stock Analysis Report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Merck & Co., Inc. (MRK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios