Medicare Advantage Market Dynamics: Navigating Consolidation and Regulatory Shifts for Long-Term Investment Gains

The Medicare Advantage (MA) landscape in 2025 is defined by stark market consolidation, regulatory headwinds, and divergent financial strategies among insurers. For investors, understanding these dynamics is critical to identifying long-term opportunities in healthcare's fastest-growing sector.

Market Consolidation: A Tale of Two Insurers

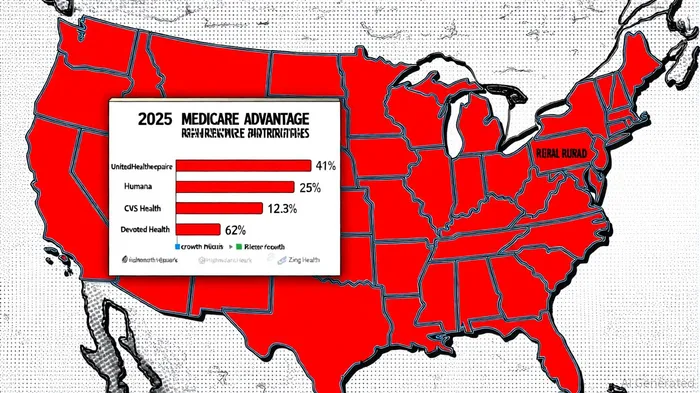

According to a report by the Kaiser Family Foundation (KFF), UnitedHealthcare and HumanaHUM-- dominate 59% of MA enrollees across two-thirds of U.S. counties, with UnitedHealthcare alone capturing 41% of enrollment in highly concentrated regions[1]. This duopoly extends to plan offerings, as the two insurers account for 66% of all MA plans[2]. Rural areas exacerbate this trend: 39% of the most rural counties are “very highly concentrated,” compared to just 6% in urban regions[1]. While smaller insurers like Highmark Health and Zing Health Consolidator, Inc. have grown plan offerings by 23.3% and 90.5% year-over-year, respectively[3], their market share remains dwarfed by industry giants. Devoted Health, however, stands out as a disruptor, expanding its plan count by 62% in 2025[3], signaling a potential shift in competitive dynamics.

Enrollment Trends and Regional Disparities

Q3 2025 data reveals a 1.3% year-over-year increase in MA enrollment, adding 450,000 members during the Annual Enrollment Period (AEP)—a slowdown from prior years[4]. Growth is uneven: Pennsylvania, Texas, and Michigan saw significant gains, while New York and Vermont experienced declines[4]. Special Needs Plans (SNPs) now account for 21% of MA enrollment, driven by a 71% surge in chronic condition-specific plans (C-SNPs)[5]. This specialization reflects insurers' strategies to target high-need populations amid regulatory pressures.

Financial Performance: Margin Management Over Membership

The financial health of MA insurers diverges sharply. Humana and CVS Health (Aetna) prioritized margin preservation in 2024 by reducing benefits and exiting unprofitable markets, resulting in improved 2025 profitability[6]. Humana cut MA membership by 400,000, while CVS reduced it by 200,000, optimizing their membership mix[6]. Conversely, UnitedHealthUNH-- Group's aggressive expansion—adding 500,000 members—backfired as rising medical costs and a 3.9% increase in medical loss ratios (MLRs) forced downward profit revisions[6]. Analysts note that regional insurers face steeper challenges, with 2024 loss ratios rising 1.7% on average versus 3.1% for national carriers[7].

Regulatory Pressures: IRA and Risk Adjustment Model V28

The Inflation Reduction Act (IRA) and the Medicare risk adjustment model V28 (2025–2027) are reshaping profitability. The IRA's drug price negotiations and $2,000 annual out-of-pocket cap for Part D beneficiaries reduce insurers' revenue streams[8]. Simultaneously, V28 recalibrates risk adjustment factors, slashing payments to MA plans by 3.12% in 2024—a $11 billion hit[8]. These changes force insurers to adopt automation and vertical integration to offset margin pressures, as highlighted by McKinsey's projection of 3–3.5% MA profitability by 2028[7].

Investment Outlook: Balancing Risk and Resilience

For long-term investors, the MA sector offers both risks and rewards. Insurers like Humana and CVS, which have embraced margin-first strategies, appear better positioned to navigate regulatory and financial headwinds. Conversely, growth-at-all-costs models, as seen with UnitedHealth, may face sustainability issues. Smaller insurers with agile operations—such as Highmark and Zing Health—could capitalize on market gaps left by larger players exiting unprofitable regions[3].

However, systemic challenges persist. The KFF notes that 97% of counties remain highly or very highly consolidated[1], limiting beneficiary choice and inviting antitrust scrutiny. Additionally, the shift toward SNPs and chronic care management demands significant capital investment in care coordination and technology.

Conclusion

The MA market's consolidation and regulatory evolution present a complex landscape for investors. While industry leaders like UnitedHealth and Humana dominate enrollment and plan offerings, their financial trajectories diverge sharply. Smaller insurers and disruptors like Devoted Health offer growth potential but face scalability hurdles. For investors, the key lies in balancing exposure to established players with resilience in margin management against emerging innovators poised to exploit market gaps. As the sector transitions from volume-based growth to value-based sustainability, strategic adaptability—not market share alone—will define long-term success.

Comentarios

Aún no hay comentarios