McDonald's Valuation Divergence: A Test of Growth Sustainability in a Rising Market

In the current investment landscape, McDonald'sMCD-- (MCD) has become a case study in valuation divergence. While the S&P 500 has rallied on the back of improving earnings and a resilient economy, McDonald's stock has lagged, trading at a premium to its peers despite robust financial performance. This disconnect raises critical questions about the sustainability of its long-term growth strategies and whether the market is overcorrecting for industry-specific challenges.

Valuation Divergence: A Premium for Future Earnings?

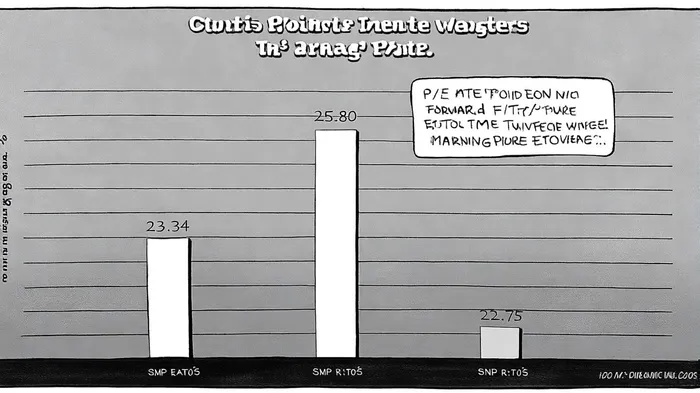

McDonald's trailing Price-to-Earnings (P/E) ratio of 25.80 and forward P/E of 23.34[1] place it above the S&P 500's average of 22.75[5], a gap that widens when compared to direct peers like StarbucksSBUX-- (36x) and ChipotleCMG-- (34.6x)[4]. This premium reflects investor optimism about the company's ability to deliver consistent earnings growth, even as its Price-to-Book (P/B) ratio remains negative (-78.4)[3], signaling a stark disconnect between market value and accounting metrics. Meanwhile, the S&P 500's P/B of 5.34[6]—though elevated—suggests a more grounded valuation for the broader market.

The divergence is further underscored by McDonald's negative debt-to-equity (D/E) ratio of -16.8[4], a byproduct of aggressive share buybacks that have eroded shareholder equity. In contrast, the S&P 500's D/E ratio of 4.78[2] reflects a sector-wide increase in leverage, particularly in Q3 2025. While McDonald's capital structure appears healthier, its reliance on buybacks to drive returns has raised concerns about long-term sustainability, especially as interest expenses rise[1].

Growth Strategies: Value, Innovation, and Expansion

McDonald's 2025 performance highlights its strategic resilience. Second-quarter revenue grew 5% year-over-year to $6.84 billion[1], driven by global comparable sales gains and the McValue menu's success in attracting price-sensitive customers. The company's “Accelerating the Arches” initiative—focused on digital innovation, menu diversification, and franchise expansion—has positioned it to outperform in an inflationary environment[3].

Notably, McDonald's plans to open 2,200 new locations in 2025 and 10,000 by 2027[4], leveraging its franchise model to scale without overburdening balance sheets. International markets, particularly Developmental Licensed regions, have shown strong growth (5.6% sales increase in Q2 2025)[1], while domestic efforts like the $5 value meal strategy have extended their reach to 93% of U.S. franchisees[3].

However, challenges persist. A 2024 E. coli outbreak linked to its Quarter Pounder[4] and shifting consumer preferences toward healthier options have pressured traffic. The company's response—introducing plant-based items like the McPlant and expanding its McCrispy line—signals an attempt to adapt, but execution risks remain.

Sustainability Concerns: Can the Premium Justify the Growth?

The key question is whether McDonald's valuation premium is warranted. Its 14.97% return on invested capital (ROIC) in 2024[1] outpaces the S&P 500's projected 9.2% earnings growth for 2025[6], suggesting strong operational efficiency. Yet, a PEG ratio of 3.13[4] indicates the market is pricing in growth that may be difficult to sustain. Analysts argue the stock is undervalued by 9.6% based on fair value estimates[4], but this assumes continued execution against ambitious expansion targets and menu innovation.

The broader market's optimism about sectors like Technology and Healthcare—projected to drive S&P 500 earnings growth into the high teens by year-end[6]—has diverted attention from defensive plays like McDonald's. However, the company's 2.35% dividend yield[3] and resilient franchising model offer a counterpoint to growth-centric narratives, particularly in a high-interest-rate environment.

Conclusion: A Case of Overcorrection or Underappreciated Resilience?

McDonald's valuation divergence reflects a tug-of-war between its proven ability to generate cash flow and the market's skepticism about its ability to adapt to evolving consumer trends. While its P/E premium and negative P/B ratio suggest investors are betting on future growth, the company's debt-driven capital structure and industry headwinds warrant caution. For now, McDonald's remains a bellwether for the fast-food sector, with its long-term success hinging on the execution of its value-driven strategies and its ability to maintain margins amid rising costs.

Comentarios

Aún no hay comentarios