McCormick's Outperformance: A Signal of Resilience in a Slowing Consumer Sector?

In a consumer goods sector grappling with inflationary pressures, tariffs, and shifting demand, McCormickMKC-- & Company's Q2 2025 results stand out as a testament to operational discipline and strategic foresight. The global flavor leader reported 2% organic sales growth, driven by volume expansion in its Consumer segment, while maintaining adjusted operating income growth of 10% year-over-year, according to McCormick's Q2 2025 release. This outperformance raises a critical question: Is McCormick's resilience a harbinger of its ability to thrive in a slowing sector, or an anomaly in an otherwise challenging landscape?

Operational Efficiency as a Competitive Moat

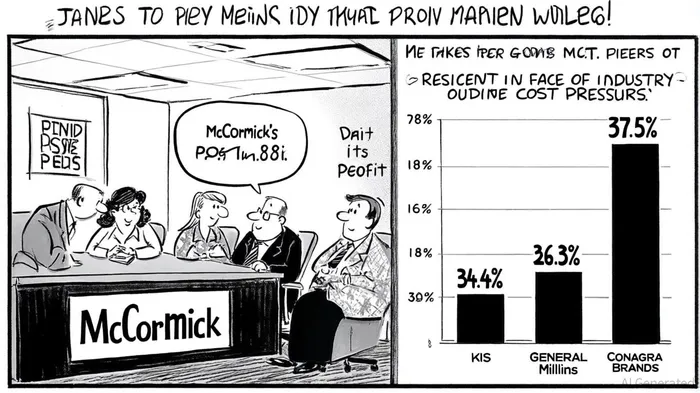

McCormick's Comprehensive Continuous Improvement (CCI) program has emerged as a cornerstone of its margin resilience. The initiative, which focuses on cost savings, advanced sourcing, and productivity gains, offset rising commodity costs and currency headwinds. For instance, in Q2 2025, gross profit margin held steady at 37.5%, despite a 20-basis-point contraction due to capacity investments and higher input costs, the release noted. By contrast, peers like Conagra Brands faced a sharper gross margin decline to 26.4% in Q1 2025, exacerbated by a 47% revenue drop in its Hebrew National segment due to supply chain disruptions, as detailed in Conagra's Q1 2025 report.

The CCI program's impact is further underscored by McCormick's ability to return $242 million to shareholders through dividends in Q2 2025, a move analysts attribute to disciplined SG&A cost management, according to the company release. This contrasts with The J. M. Smucker Company, which reported a $594 million operating loss in Q3 2025 due to noncash impairment charges, despite a 1% increase in adjusted operating income, per J.M. Smucker's Q3 2025 results.

Navigating Tariffs and Commodity Volatility

The consumer goods sector in 2025 is defined by its struggle with tariff-driven cost inflation. McCormick's proactive approach-diversifying supply chains and leveraging the CCI program-has allowed it to mitigate these pressures. For example, the company plans to expand domestic production capacity to reduce reliance on high-tariff imports, a strategy mirrored by peers but executed with greater precision, the release said.

General Mills, a top competitor with $19.49 billion in Q2 2025 revenue, reported a 34.83% gross margin, a 4.61% year-over-year decline, as shown in General Mills' Q1 2025 report. While the company cited cost management initiatives as a driver of its 7% EPS growth, its margin contraction highlights the sector's vulnerability to input costs. Conagra Brands, meanwhile, anticipates a 7% cost increase in fiscal 2026 from tariffs and inflation, with productivity gains expected to offset only 4% of this burden (as noted in Conagra's Q1 2025 report).

Strategic Positioning in a Volume-Driven Era

Industry trends increasingly favor volume-led growth over price-driven strategies, as consumers prioritize affordability. McCormick's focus on health-conscious and value-driven product innovation aligns with this shift. Its Consumer segment saw 3% volume growth in Q2 2025, driven by brand investments and distribution expansion, the company release reported. This contrasts with the Flavor Solutions segment's flat performance, which underscores the challenges of industrial demand in a macroeconomic slowdown, as highlighted by Deloitte's 2025 industry outlook.

Peers like General Mills and Conagra are also pivoting toward volume growth but face headwinds. General Mills' Q1 2025 gross margin of 35.2%-a 50-basis-point year-over-year improvement-was offset by a 10.59% decline in operating income (see General Mills' report). Conagra's Q1 2025 operating margin of 14.2% is projected to fall to 11–11.5% in 2026, reflecting the limits of its cost-cutting initiatives (as discussed in Conagra's report).

The Path Forward: Sustaining Resilience

McCormick's 2025 outlook-organic sales growth of 1–3% and adjusted EPS growth of 5–7%-reflects cautious optimism. However, the company's ability to sustain its outperformance hinges on two factors:

1. Execution of its $1 billion capital allocation plan to fund capacity expansion and shareholder returns.

2. Continued innovation in high-growth categories, such as plant-based and global spice blends, to drive volume growth, the release emphasized.

Industry analysts note that only a minority of consumer goods companies are achieving significant volume growth, with most relying on unsustainable price hikes, according to Deloitte's industry outlook. McCormick's emphasis on transformative efficiency-modernizing supply chains and leveraging AI for demand forecasting-positions it to avoid this trap (Deloitte's outlook).

Conclusion: A Model for Resilience

McCormick's Q2 2025 results demonstrate that operational excellence and strategic agility can mitigate macroeconomic headwinds. While the sector faces persistent challenges, the company's CCI program, tariff mitigation strategies, and volume-driven innovation create a durable competitive edge. For investors, the question is no longer whether McCormick can outperform its peers-but whether its playbook can be replicated in an industry where margin resilience is increasingly scarce.

Comentarios

Aún no hay comentarios