Market Resilience and Undervalued Assets: Navigating the 2025 Government Shutdown

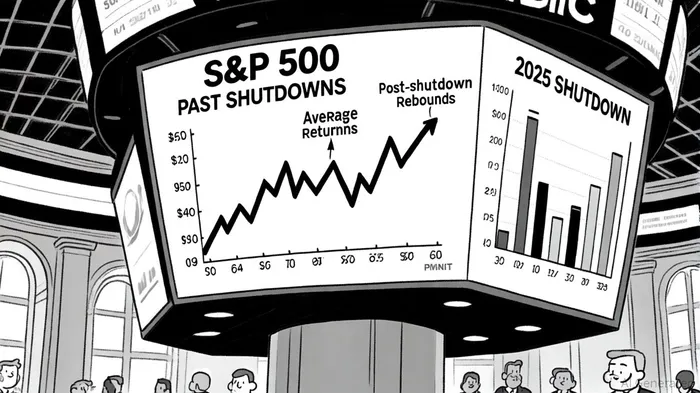

Government shutdowns in the United States have long been a source of political drama, but their economic and market impacts are often overstated. Historical data reveals a pattern of market resilience, with the S&P 500 averaging a modest 0.2% return during shutdowns since 1976 and rebounding strongly in the following month, according to the YCharts data. The 2025 shutdown, which began on October 1, 2025, has followed a similar script, with the index rising 0.34% on the first day despite widespread uncertainty. This resilience underscores a critical insight for investors: while shutdowns create short-term noise, they rarely derail long-term market trends.

Historical Context: Shutdowns and Market Behavior

Government shutdowns have historically had limited and often transient effects on asset classes. For instance, the 35-day 2018–2019 shutdown coincided with a 10.3% gain in the S&P 500, driven by Federal Reserve policy and trade negotiations rather than the shutdown itself, per the YCharts analysis. Similarly, the 2013 shutdown initially caused a 3% decline but was followed by a swift rebound and a positive monthly close, as noted in the CNBC analysis. These examples highlight that shutdowns are rarely catalysts for sustained downturns. Instead, broader macroeconomic factors-such as interest rates, inflation, and global trade dynamics-tend to dominate market performance.

The 2025 shutdown has introduced unique challenges, however. Delayed release of key economic data, including employment and inflation figures, has created uncertainty around the Federal Reserve's October rate cut decision, according to the YCharts piece. Fixed-income markets have responded with mixed volatility, as seen in the MOVE Index's pre-shutdown rise and post-shutdown decline, based on an IBAfin analysis. Meanwhile, the 10-year Treasury yield has fallen on average during shutdowns, reflecting a flight to safety, a pattern echoed by the CNBC analysis.

Undervalued Assets: Sectors Poised for a V-Shaped Recovery

While the broader market has shown resilience, certain sectors and assets have been disproportionately affected by the 2025 shutdown, presenting opportunities for a V-shaped recovery.

Healthcare and Government Services Contractors

The healthcare sector has emerged as a defensive haven during the 2025 shutdown, with the XLV ETF rising 3.09% on the first day, according to YCharts. This performance aligns with historical patterns: healthcare outperformed during the 2013 shutdown but lagged in 2018–2019, suggesting its performance is more tied to macroeconomic conditions than shutdowns themselves. Government services contractors, such as CACI International (CACI), have surged by 3.28%, reflecting expectations of catch-up spending once the shutdown ends. These sectors are well-positioned to rebound as political gridlock resolves and federal contracts resume.Defense and Aerospace

Defense manufacturers have remained stable during the 2025 shutdown, with an average decline of just -0.01%, per the YCharts data. Historically, the defense sector has outperformed the S&P 500 during shutdowns due to long-term fiscal support and geopolitical tensions. For example, during the 2018–2019 shutdown, defense stocks outperformed as investors anticipated increased military spending. A prolonged 2025 shutdown could amplify this dynamic, particularly if fiscal stimulus measures are enacted post-resolution.Safe-Haven Assets: Gold and Treasuries

Gold has reached record highs in 2025 as investors seek refuge from political uncertainty, according to a Business Insider report. This aligns with historical trends, where gold and Treasury bonds have typically gained traction during shutdowns, as noted in a Morgan Stanley analysis. The 10-year Treasury yield fell 3 basis points to 4.12% during the 2025 shutdown, reinforcing its role as a safe-haven asset per the YCharts piece. These assets are likely to remain attractive until political clarity is restored.

The Case for a V-Shaped Recovery

The 2025 shutdown has created a unique confluence of factors that could drive a sharp post-resolution rebound. Historically, the S&P 500 has gained an average of 13% in the 12 months following a shutdown, according to the YCharts analysis. This pattern is supported by the 2025 context: a data-dependent Federal Reserve, ongoing AI-driven market momentum, and fiscal initiatives like the "Big Beautiful Bill," as discussed in a Publish0x article. Sectors like defense, healthcare, and government services are particularly well-positioned to benefit from catch-up demand and policy-driven spending.

However, risks remain. Prolonged shutdowns could disrupt GDP growth (estimated at a 0.1% annualized decline per week, per the Morgan Stanley analysis) and delay critical policy decisions. Investors should remain cautious but avoid overreacting to short-term volatility. As the 2025 shutdown unfolds, the focus should shift to long-term fundamentals-earnings growth, interest rates, and geopolitical stability-rather than the immediate noise of political brinkmanship.

Conclusion

The 2025 government shutdown, while disruptive, has not derailed the market's upward trajectory. Investors who focus on undervalued sectors like healthcare, government services, and defense-and maintain exposure to safe-haven assets like gold and Treasuries-may position themselves to capitalize on a V-shaped recovery. As history shows, markets tend to absorb the shocks of shutdowns and rebound with vigor once political uncertainties are resolved. The key is to stay disciplined, diversified, and attuned to the broader economic forces shaping the landscape.

Comentarios

Aún no hay comentarios