Market Momentum and Speculative Buying in Post-Peak Equity Environments: The Role of Risk-Rebalancing Strategies

In the wake of speculative fervor and momentum-driven rallies, post-peak equity markets present a paradox: extraordinary short-term gains coexist with heightened risks of reversal. The 2024 market surge, where U.S. momentum stocks outperformed the S&P 500 by over 100%, exemplifies this dynamic[3]. While such environments tempt investors to chase returns, they also amplify the need for disciplined risk-rebalancing strategies to preserve long-term portfolio resilience.

The Dual Forces of Momentum and Speculation

Market momentum, defined by the continuation of existing price trends, thrives on speculative buying. During the 2024 rally, momentum stocks—often characterized by stretched valuations and weak earnings—soared 58% compared to the S&P 500's 23% gain[3]. However, this concentration of returns underscores inherent fragility. Historical data reveals that momentum strategies suffer catastrophic drawdowns during turning points, such as the 91% loss in 1932–1933 and the 73% loss in 2009[1]. These crashes are typically preceded by overvaluation and are exacerbated by the reversal of previously strong performers.

Speculative behavior further amplifies these risks. Ultra-high-net-worth (UHNW) households, with portfolios exceeding $100 million, often adopt countercyclical strategies, buying equities during declines[1]. In contrast, high-net-worth and typical investors tend to sell during downturns, exacerbating market volatility. This divergence highlights how speculative buying—driven by retail and institutional participants—can create self-reinforcing cycles of euphoria and panic.

Risk-Rebalancing: A Counterweight to Short-Term Euphoria

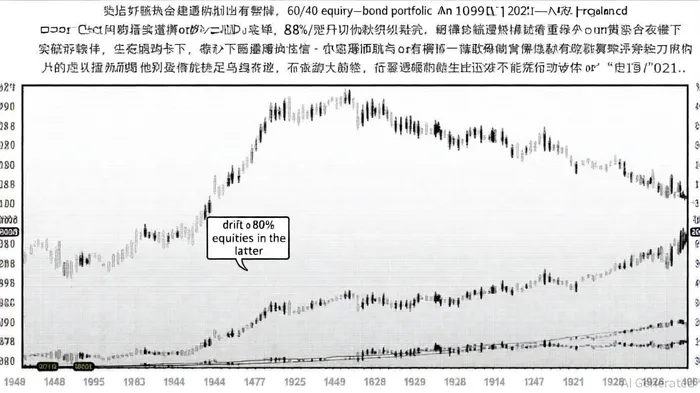

Risk-rebalancing strategies serve as a critical tool to mitigate the destabilizing effects of speculative momentum. By enforcing disciplined adjustments to asset allocations, rebalancing locks in gains from overperforming assets while systematically adding to underperforming ones. For instance, a 60/40 equity-bond portfolio left unadjusted from 1989 would have drifted to 80% equities by 2021, significantly increasing risk exposure[2]. Rebalancing resets this drift, ensuring alignment with long-term objectives.

Threshold-based rebalancing, which triggers adjustments when allocations deviate beyond predefined bands (e.g., ±15–20%), has proven particularly effective in volatile environments[4]. During the 2024 momentum-driven market, investors who rebalanced using such bands sold overperforming equities and increased bond allocations, maintaining risk parity amid rising volatility[1]. This approach not only curtails overexposure to speculative assets but also capitalizes on market inefficiencies by buying low and selling high.

Case Study: 2024 and the Power of Tactical Rebalancing

The 2024 market provides a vivid case study. As U.S. equities surged, many investors adhered to disciplined rebalancing, shifting capital to bonds and alternative assets like real estate and gold[1]. This tactical reallocation helped mitigate downside risks when speculative valuations corrected. For example, Vanguard's analysis noted that investors who rebalanced during the 2024 peak preserved capital by reducing equity exposure, even as non-U.S. markets and bonds lagged[1].

Moreover, hybrid rebalancing strategies—combining calendar-based and threshold-based methods—modestly improved risk-adjusted returns in 2024[2]. These strategies allowed investors to respond to both time-based and market-driven signals, enhancing adaptability. Morgan Stanley's extended Samuelson model (ESM) further demonstrated how dynamic rebalancing, informed by macroeconomic indicators and sentiment analysis, could predict momentum phases and guide proactive adjustments[3].

The Quantitative Edge: Advanced Rebalancing Frameworks

Quantitative approaches are increasingly shaping risk-rebalancing strategies. A 2024 study revealed that investors favored moderate asset allocations, with a 69% reliance on ETFs for diversification and cost efficiency[4]. Advanced frameworks, such as probabilistic macro allocation models and machine learning-driven risk assessment, have enabled more precise rebalancing decisions[4]. For instance, hidden Markov models and Generative Adversarial Networks (GANs) now help identify regime shifts in market conditions, allowing for timely reallocations[4].

Conclusion: Balancing Euphoria with Discipline

Post-peak equity environments demand a delicate balance between capitalizing on momentum and mitigating its risks. While speculative buying can drive short-term euphoria, it also heightens the likelihood of abrupt reversals. Risk-rebalancing strategies—particularly those leveraging threshold bands and quantitative insights—offer a structured approach to navigate these challenges. By adhering to disciplined rebalancing, investors can sustain long-term gains, avoid the pitfalls of market timing, and align portfolios with evolving risk profiles.

As markets evolve in 2025, the transition from speculative optimism to earnings-driven fundamentals will test the resilience of investment strategies. Those who prioritize adaptability and discipline, rather than chasing fleeting momentum, are likely to emerge with portfolios that endure.

Comentarios

Aún no hay comentarios