U.S. Manufacturing Contracts Again in March as Prices Surge; Markets React Sharply

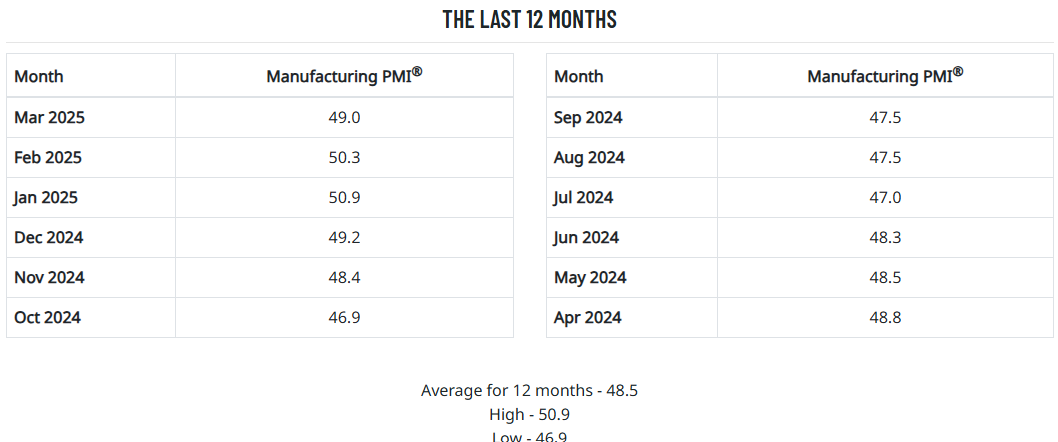

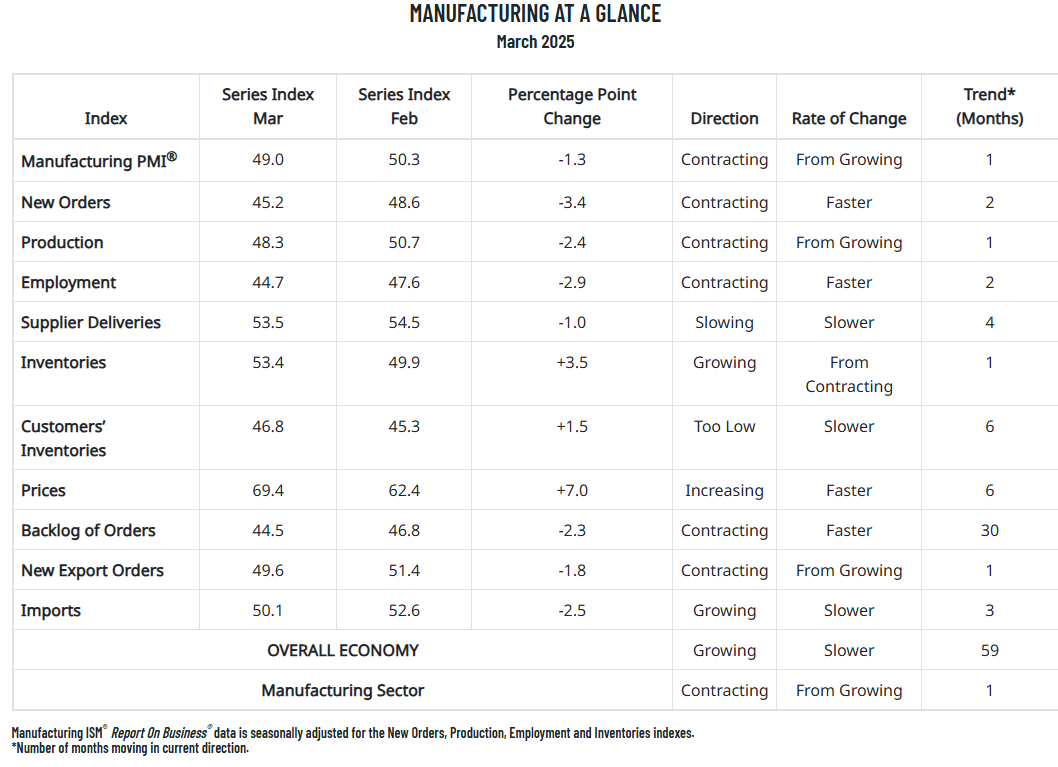

The March ISM Manufacturing Index fell to 49.0, below consensus expectations of 49.5 and down from February’s 50.3 reading, marking a return to contraction for the U.S. manufacturing sector. The data interrupted a fragile rebound, with the report showing weakening demand, deteriorating production, and softening labor conditions—while cost pressures escalated dramatically. The sharp rise in input prices, particularly the Prices Paid component, sparked fresh inflation concerns and weighed on risk sentiment, prompting a broad market selloff as investors reassessed the soft-landing narrative.

New orders fell deeper into contraction territory, declining 3.4 points to 45.2, highlighting persistent demand weakness. The Production Index dropped to 48.3 from 50.7, snapping a brief two-month expansion streak. Meanwhile, the Employment Index sank to 44.7 from 47.6, a sign that manufacturers are actively cutting headcount or attriting staff in response to sluggish activity. The contraction in these key subcomponents suggests factory floors are seeing a pullback not just in output, but in expectations as well.

The standout—and market-moving—element of the report was the Prices Index, which surged to 69.4 from 62.4, well above forecasts and its highest level since mid-2022. The acceleration in input costs is being linked to new tariffs and critical material shortages, especially those tied to Chinese export restrictions on strategic minerals like germanium. These inflationary signals complicated the Federal Reserve’s path forward, rekindling fears of stagflation at a time when core PCE had just shown tentative progress.

Inventories jumped back into expansion at 53.4, up sharply from 49.9, likely reflecting firms pulling forward purchases in anticipation of further tariff-driven cost increases. This restocking dynamic, while supportive of near-term activity, may prove transitory if demand does not rebound. Supplier Deliveries eased slightly to 53.5, still signaling slower deliveries but at a decelerating rate. Meanwhile, customers’ inventories remained in “too low” territory, suggesting some tension between stocking behavior and end-market absorption.

The trade subcomponents offered further cause for caution. New Export Orders dipped to 49.6 from 51.4, falling back into contraction, while Imports slowed but held slightly above the expansion line at 50.1. This dynamic reflects both softer global demand and potential distortions from shifting trade terms, including retaliatory measures from Canada and Europe. Respondents flagged concerns around overseas buyer resistance to U.S. goods, while others cited inventory surges as customers tried to get ahead of price increases.

Tariffs emerged as a clear villain across multiple respondent comments. Executives cited cost pressures, compressed profit margins, and growing uncertainty around purchasing decisions as key pain points. Several noted that short-term boosts in orders may be masking deeper concerns about demand destruction and geopolitical risk. A common refrain across sectors was the difficulty in forecasting amidst policy-driven price volatility—an echo of 2018’s trade war dislocations.

Markets responded negatively to the report, with the S&P 500 falling over 0.5% intraday as Treasury yields fell on growth concerns.

In sum, the March ISM Manufacturing Report delivered a sobering message: activity is slowing, and cost pressures are accelerating. For policymakers, this raises the specter of renewed inflation just as growth shows signs of rolling over. For investors, the report reinforced the fragility of the “immaculate disinflation” thesis—and suggests that the next directional move in markets may hinge on how the Fed balances its dual mandate against a noisy, geopolitically fraught backdrop.

Comentarios

Aún no hay comentarios