Is Malibu Boats (MBUU) a Buy After Recent Earnings and Macro Headwinds?

Valuation: A Discounted Premium or a Hidden Risk?

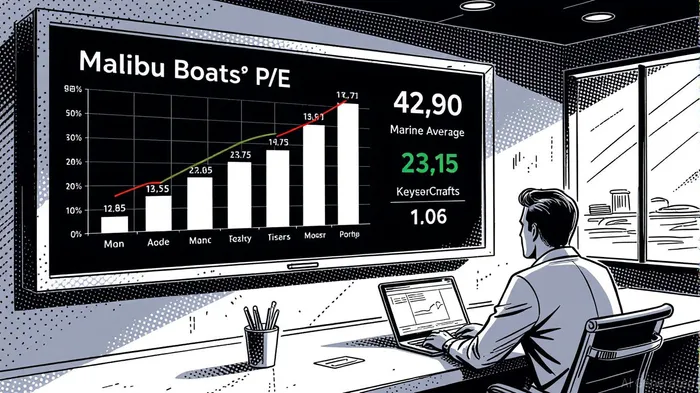

Malibu Boats (MBUU) trades at a trailing P/E ratio of 42.90, a stark contrast to the marine industry's average of 14.87. This premium suggests investors are paying a significant multiple for current earnings, which fell 76.1% year-over-year in Q2 2025. However, the forward P/E ratio of 11.71 indicates a potential re-rating if earnings stabilize, aligning closer to the industry average.

The company's P/S ratio of 0.79 further underscores its undervaluation relative to peers. For context, the marine shipping industry's average P/S is 1.47, while boat manufacturing firms like MasterCraftMCFT-- (P/S: 1.06) and Marine ProductsMPX-- (P/S: 1.4x) trade at higher multiples. MBUU's forward P/S of 0.82 suggests it is priced at a 62% discount to the broader marine industry, a gap that could narrow if revenue growth (up 30.45% year-to-date) outpaces earnings challenges.

Earnings Momentum: Segment Divergence and Operational Discipline

Q2 2025 results revealed a bifurcated performance. The Saltwater Fishing segment declined 15.2% to $70.2 million in sales, while the Cobalt segment grew 7.8% to $56.0 million. This divergence highlights MBUU's exposure to macroeconomic shifts, particularly in discretionary spending. Management attributes the sales drop to elevated dealer inventory and a weak retail environment, with CEO Steve Menneto emphasizing the need for “ongoing discipline” to align production with demand.

Adjusted EBITDA fell 26.3% to $16.9 million, reflecting margin pressures from inventory adjustments and macroeconomic uncertainty. However, proactive cost management—such as supply chain optimizations and selective price increases—could mitigate further declines. The revised full-year guidance, while conservative, signals a realistic approach to navigating a challenging market.

Macro Risks: Tariffs, Rates, and Consumer Sentiment

The marine industry faces a trifecta of headwinds. Global tariff uncertainty looms large, with MBUUMBUU-- preparing for higher cost of goods sold. Analysts at DA Davidson have cut price targets, citing the need for “more tangible data” before adopting a bullish stance. Meanwhile, elevated interest rates are dampening consumer demand, as boat purchases remain sensitive to borrowing costs.

Marine shipping peers like Teekay TankersTNK-- (P/E: 5.93) and ZIM Integrated ShippingZIM-- (P/S: 0.41) trade at even steeper discounts, underscoring sector-wide fragility. For MBUU, the path to recovery hinges on macroeconomic clarity and a rebound in retail confidence—a timeline that remains uncertain.

Conclusion: A Cautious Case for Value Investors

Malibu Boats' valuation metrics suggest it is undervalued relative to peers, particularly given its forward P/E and P/S ratios. However, earnings momentum remains fragile, and macroeconomic risks—tariffs, interest rates, and consumer caution—pose significant hurdles. For value investors, MBUU could represent an opportunity if the company executes its inventory and cost strategies effectively. Yet, the lack of near-term catalysts and sector-wide headwinds warrant a cautious approach.

In the absence of a clear retail recovery or macroeconomic stabilization, the stock's upside potential is contingent on navigating these challenges with operational agility. For now, MBUU appears more suited to patient, risk-tolerant investors than aggressive growth seekers.

Source:

[1] Malibu BoatsMBUU-- (MBUU) Financial Ratios,

https://stockanalysis.com/stocks/mbuu/financials/ratios/

[2] Malibu Boats, Inc. Announces Second Quarter Fiscal 2025 Results,

https://www.malibuboatsinc.com/investor-information/earnings-news/news-details/2025/Malibu-Boats-Inc.-Announces-Second-Quarter-Fiscal-2025-Results/default.aspx

[3] Malibu Boats (MBUU) All Metrics,

https://www.financecharts.com/stocks/MBUU/all-metrics

[4] PS ratio (Revenue Multiple) by industry,

https://fullratio.com/ps-ratio-by-industry

[5] Price-to-Sales Ratio By Industry (2025),

https://eqvista.com/price-to-sales-ratio-by-industry/

[6] MasterCraft BoatMCFT-- Holdings Valuation,

https://simplywall.st/stocks/us/consumer-durables/nasdaq-mcft/mastercraft-boat-holdings/valuation

[7] Marine Products (NYSE:MPX) - Stock Analysis,

https://simplywall.st/stocks/us/consumer-durables/nyse-mpx/marine-products

[8] MBUU PE Ratio — MBUU Valuation,

https://intellectia.ai/stock/MBUU/valuation

[9] Manufacturing EBITDA & Valuation Multiples – 2025 Report,

https://firstpagesage.com/business/manufacturing-ebitda-valuation-multiples/

[10] Malibu Boats, Inc. Announces Second Quarter Fiscal 2025 Results,

https://www.malibuboatsinc.com/investor-information/earnings-news/news-details/2025/Malibu-Boats-Inc.-Announces-Second-Quarter-Fiscal-2025-Results/default.aspx

[11] Ibid.

[12] Tariff and Inventory Headwinds Temper Retail Recovery Hopes,

https://markets.financialcontent.com/wral/article/stockstory-2025-8-29-mbuu-q2-deep-dive-tariff-and-inventory-headwinds-temper-retail-recovery-hopes

[13] Ibid.

[14] Ibid.

[15] Ibid.

[16] DA Davidson lowers Malibu Boats stock price target on ...

https://in.investing.com/news/analyst-ratings/da-davidson-lowers-malibu-boats-stock-price-target-on-marine-industry-caution-93CH-4996938

[17] Ibid.

[18] TeekayTK-- Tankers: A Deep-Value Maritime Play with a ...,

https://www.ainvest.com/news/teekay-tankers-deep-maritime-play-compelling-risk-reward-profile-2508/

[19] ZIM Integrated Shipping Services (ZIM) - P/S ratio,

https://companiesmarketcap.com/zim/ps-ratio/

Comentarios

Aún no hay comentarios