Mainframe Service Providers and Digital Transformation: Strategic Valuation and Growth Potential in Legacy IT Modernization

The mainframe computing landscape is undergoing a seismic shift as enterprises prioritize digital transformation and legacy IT modernization. While mainframes remain the backbone of critical systems in finance, healthcare, and government, their integration with cloud-native architectures, AI, and automation is unlocking new value. For investors, this transition presents a compelling opportunity to evaluate strategic valuation metrics and growth potential among key service providers.

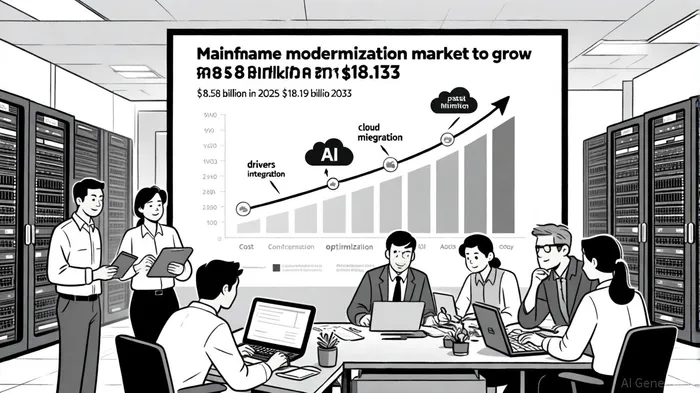

Market Dynamics: A Dual Growth Story

The global mainframe modernization market is projected to surge from $8.58 billion in 2025 to $18.19 billion by 2033, growing at a 9.8% CAGR, according to Grand View Research. This acceleration is fueled by the need to reduce operational costs, enhance scalability, and align legacy systems with cloud and AI-driven workflows, according to In‑Com. Meanwhile, the broader legacy IT modernization market is expected to expand even faster, with a 17.92% CAGR, reaching $56.87 billion by 2030, according to Mordor Intelligence. These figures underscore a critical insight: modernization is no longer optional but a strategic imperative for enterprises seeking agility in a digital-first era.

Key drivers include the integration of AI and machine learning to automate code refactoring and optimize performance - a trend highlighted by In‑Com - as well as the adoption of microservices architectures to decouple monolithic systems, noted by Grand View Research. For example, Fujitsu's GenAI-assisted modernization projects have reduced system update times by 50% for clients like Toyota, as reported by Mordor Intelligence, demonstrating the tangible ROI of these technologies.

Strategic Valuation: Revenue Growth, Market Share, and Partnerships

Investors must assess the competitive positioning of mainframe service providers through three lenses: revenue growth, market share, and strategic partnerships.

- Revenue Growth:

- IBM, the dominant player in the mainframe market (64% share in 2024, per Mordor Intelligence), reported $27 billion in Software segment revenue in 2024, driven by its hybrid cloud and AI strategy. Its acquisition of Red Hat has positioned it as a leader in enterprise cloud integration.

Unisys, with its GS Series mainframes, faces a smaller but growing niche. Despite a 1.53% year-over-year revenue decline in its 12-month fiscal period ending June 2025 (WallStreetZen), the GS Series is projected to grow at a 10.8% CAGR, outpacing IBM's Z Systems due to its cost-performance balance, according to Mordor Intelligence.

Market Share:

- IBM's Z Systems dominate the mainframe hardware market, according to Mordor Intelligence, but competitors like UnisysUIS-- and Fujitsu are gaining traction in hybrid cloud environments. Unisys holds a 3.62% market share in Cloud Computing & Data Analytics, reflecting its focus on infrastructure modernization (WallStreetZen).

Kyndryl, spun off from IBMIBM--, leverages its infrastructure management expertise to offer multi-cloud partnerships, enabling clients to reduce costs while maintaining compliance, as described by In‑Com.

Strategic Partnerships:

- AWS and DXC Technology are redefining modernization through cloud-native solutions. AWS's platform allows enterprises to rehost or refactor mainframe workloads, integrating with analytics and security tools, while DXC's GenAI-powered services accelerate refactoring with vendor-neutral approaches - both trends covered by In‑Com.

- M&A activity further strengthens these strategies. For instance, Databricks' acquisition of BladeBridge and MongoDB's purchase of Voyage AI were highlighted in a CIO roundup, demonstrating the sector's focus on AI-driven modernization tools.

M&A and Investment Trends: Consolidation and Specialization

The mainframe and legacy IT modernization sectors are witnessing aggressive consolidation. In 2025, U.S. M&A deal values in technology and telecommunications surged, with AI-related transactions doubling year-over-year, according to an EY report. High-profile deals like Roche's $3.5 billion acquisition of 89bio and Radian's $1.7 billion purchase of Inigo signal a shift toward specialized capabilities in data analytics and automation.

For mainframe providers, M&A is a tool to expand cloud and AI competencies. Cohesity's acquisition of Veritas, for example, bolsters its data protection offerings - a critical component of modernization strategies. Similarly, Presidio's acquisition of Contender Solutions reflects the industry's push to deliver end-to-end digital transformation services, as noted by EY.

Investment Potential: Balancing Risks and Rewards

While the market's growth trajectory is clear, investors must weigh risks such as technological obsolescence and client resistance to change. However, the rewards are substantial:

- High-margin services: Modernization projects often command premium pricing due to their complexity and ROI.

- Long-term client relationships: Enterprises reliant on mainframes for mission-critical operations are likely to maintain long-term partnerships with trusted providers.

- Scalability through AI/ML: Automation reduces the cost of refactoring, enabling providers to scale services across industries, a pattern identified by In‑Com.

Conclusion: A Strategic Buy for the Digital Era

Mainframe service providers are no longer custodians of legacy systems but architects of digital transformation. With the modernization market set to nearly double in a decade, according to Grand View Research, companies like IBM, AWS, and Kyndryl are well-positioned to capitalize on this shift. For investors, the key is to prioritize firms with robust AI/ML integration, flexible cloud partnerships, and proven M&A strategies. As enterprises grapple with technical debt and the need for agility, the mainframe's evolution from relic to enabler will define the next era of IT investment.

Comentarios

Aún no hay comentarios