Main Street Capital: A Strategic Entry Point Amid Market Overreaction and Strong Fundamentals

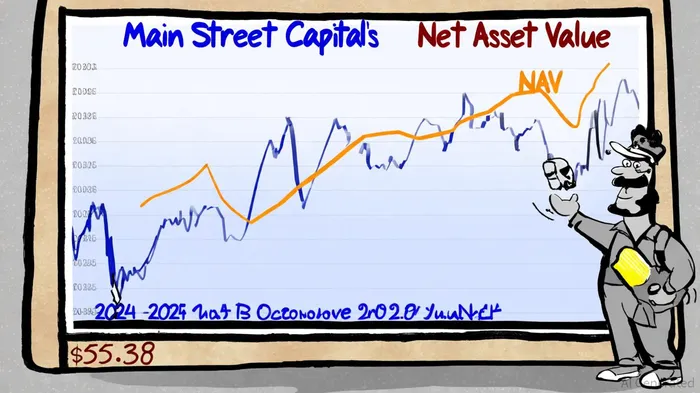

The recent 12.96% decline in Main Street Capital's (MAIN) stock price in October 2025 has sparked renewed interest among value-oriented investors. While the drop may seem alarming at first glance, a closer examination of the company's fundamentals, sector dynamics, and valuation metrics reveals a compelling case for strategic entry. With a Net Asset Value (NAV) per share of $32.30 as of Q2 2025 and a current stock price of $55.38, the P/NAV ratio stands at 1.73x-a historically attractive level for a Business Development Company (BDC) with Main Street's track record of disciplined investing and operational efficiency, according to the Q2 2025 slides.

Fundamental Resilience: A Model of Stability in a Volatile Sector

Main Street Capital's business model is a testament to its long-term resilience. As a leading BDC, the firm specializes in customized debt and equity solutions for lower middle market (LMM) companies and private equity-backed businesses. Its Q2 2025 results underscore this strength: revenue grew 8.9% year-over-year to $144 million, outpacing expectations, while NAV per share increased 8.4% to $32.30, as shown in the Q2 2025 slides. The company's portfolio is diversified across 187 companies, with 52% allocated to LMM investments and 38% to private loans, ensuring a balanced exposure to high-yield opportunities (Q2 2025 slides).

A critical differentiator is Main Street's conservative leverage ratio of 0.65x and a weighted-average effective yield of 12.0% on its investments (Q2 2025 slides). These metrics highlight its ability to generate consistent returns while mitigating risk-a rare combination in the BDC sector. Furthermore, the firm's operating expense to assets ratio of 1.3% reflects cost-efficient operations, a key driver of profitability in a low-margin environment (Q2 2025 slides).

Market Overreaction: A Sector-Wide Headwind, Not a Company-Specific Crisis

The BDC sector has faced broad-based headwinds in Q3 2025, driven by macroeconomic uncertainties and the Federal Reserve's rate-cutting cycle. Analysts at Sahm Capital note that rising interest rates and non-accrual risks have pressured BDC valuations, with some stocks hitting 52-week lows. However, Main Street's fundamentals remain robust. Its 52-week high of $67.77 and current price of $55.38 suggest a 22.37% discount to peak valuations, yet the company's intrinsic value-backed by a 17.1% annualized Return on Equity (ROE) and a 132% increase in monthly dividends since its IPO-remains intact, as the company stated in its preliminary estimate.

Wall Street analysts have assigned MAIN a "Moderate Buy" consensus rating, with a 12-month average price target of $61.20 (implying a 10.5% upside from the current price), according to MarketBeat. This optimism is grounded in Main Street's ability to navigate sector-wide challenges through proactive balance sheet management, including debt refinancing and equity issuances (company preliminary estimate). For instance, the company's Q2 2025 results included a $0.30 supplemental dividend, demonstrating its capacity to reward shareholders even amid macroeconomic turbulence (Q2 2025 slides).

Strategic Entry Opportunity: Undervaluation and Long-Term Catalysts

Main Street's current valuation offers a rare entry point for investors seeking exposure to a high-quality BDC. At a P/NAV of 1.73x, the stock trades at a discount to its historical average of 1.8–2.0x, a range typical for BDCs with Main Street's credit profile (Q2 2025 slides). Analysts at Sahm Capital note that the firm's fair value is likely near $62.96, suggesting the market has overcorrected in its reaction to sector-wide risks (Sahm Capital).

Long-term catalysts further bolster the case for investment. Main Street's focus on LMM companies-a sector poised for growth as private equity activity rebounds-positions it to capitalize on underserved credit markets (Q2 2025 slides). Additionally, its 4.8% dividend yield, coupled with a 132% increase in payouts since its IPO, offers income-focused investors a compelling total return profile (Q2 2025 slides).

Conclusion: A Case for Prudent Optimism

Main Street Capital's recent price drop is a buying opportunity for investors who recognize the gap between market sentiment and the company's underlying strength. With a diversified portfolio, conservative leverage, and a track record of NAV growth, MAIN is well-positioned to recover as macroeconomic uncertainties abate. For those willing to look beyond short-term volatility, the stock represents a strategic entry point into a BDC with a proven ability to deliver value over the long term.

Comentarios

Aún no hay comentarios