Luxfer Holdings' Dividend Signal and Future Earnings Potential: Navigating Sustainability in a High-Yield Environment

Luxfer Holdings PLC (LXFR) has long been a magnet for income-focused investors, offering a dividend yield of approximately 4.77% in 2025-well above the Industrials sector average of 3.4%, according to a Panabee analysis. However, the company's dividend sustainability is under intense scrutiny due to conflicting financial metrics and liquidity pressures. This analysis evaluates Luxfer's dividend signal and future earnings potential, dissecting its cash flow dynamics, refinancing challenges, and sector positioning in a high-yield environment.

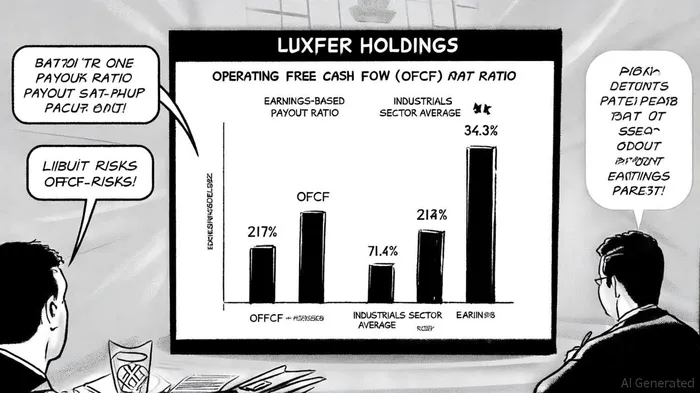

Dividend Sustainability: A Tale of Two Payout Ratios

Luxfer's dividend sustainability hinges on reconciling two starkly different payout ratios: 217% based on operating free cash flow (OFCF) and 71.4% based on earnings per share (EPS), according to FullRatio. The 217% OFCF ratio reveals a critical flaw: the company's quarterly dividend of $0.13 per share exceeds its operating cash flow generation, forcing reliance on debt financing and drawn banking facilities, a Panabee note explains. For the first half of 2025, operating cash flow fell 48% year-over-year to $6.6 million, driven by adverse working capital changes and the absence of prior-year legal cost recoveries, per StockAnalysis.

Conversely, the 71.4% EPS-based ratio suggests a more favorable picture, implying that earnings cover the dividend with a manageable margin. This discrepancy underscores the importance of context: while EPS-based metrics may appear reassuring, OFCF-a stricter measure of cash availability-paints a grimmer reality. Luxfer's low cash-to-debt ratio of 0.13 and $28.7 million in short-term debt further amplify risks, as noted by StockInvest.

Liquidity Constraints and 2026 Refinancing Hurdles

Luxfer's liquidity position is precarious. Year-to-date operating cash flow of $6.6 million in 2025 fell short of the $7.0 million in dividends paid, with the gap partially funded through drawn banking facilities (Panabee). The company's $105 million undrawn revolving credit facility provides some buffer, but its ability to maintain dividend payments depends heavily on refinancing $25 million in Loan Notes maturing in 2026 (the Panabee 0.13 note). Preliminary steps have been initiated, but securing favorable terms in a potentially tighter credit environment remains uncertain. Failure to refinance could force LuxferLXFR-- to prioritize debt repayment over dividends, jeopardizing its high-yield appeal.

Future Earnings and Sector Positioning

Luxfer's 2025 Q2 results offer a glimmer of optimism. Adjusted EPS of $0.30-30% above forecasts-and revenue of $104 million (exceeding $98.2 million estimates) reflect effective cost management and strategic shifts toward high-margin sectors like aerospace and space exploration, as detailed in the earnings transcript. The company updated its 2025 guidance to $0.97–$1.05 in adjusted EPS and $49–$52 million in adjusted EBITDA, with free cash flow projected at $20–25 million, according to Seeking Alpha. While these figures suggest modest growth, the $3.5 million quarterly dividend ($14 million annually) still strains OFCF, which averaged $1.65 million in Q3 2025 (Panabee).

The Industrials sector, however, remains a tailwind. Up 17% year-to-date in 2025, the sector benefits from easing trade tensions, manufacturing recovery, and high-yield opportunities, according to TradersAlley. Competitors like Otis Worldwide (1.9% yield) and C.H. Robinson (2.4% yield) leverage stable cash flows and AI-driven efficiency to bolster dividends. Luxfer's 4.77% yield is competitive, but its OFCF-driven payout ratio of 217% lags behind sector peers, raising questions about its ability to sustain payouts amid economic volatility.

Balancing Risk and Reward

Luxfer's Dividend Sustainability Score (71.01%) and Growth Potential Score (44.10%) suggest a moderate likelihood of maintaining or increasing dividends, per StockInvest. Yet these scores must be weighed against its OFCF constraints. A 2025–2026 earnings forecast of $1.03 and $1.18 per share, respectively, indicates cautious optimism, but revenue growth of 3%–4% may not offset cash flow pressures, according to Yahoo Finance. Investors must also consider the company's reliance on undrawn credit facilities and its exposure to short-term debt.

Conclusion: A High-Yield Dilemma

Luxfer Holdings' dividend yield is undeniably attractive in a high-yield environment, but its sustainability is contingent on resolving liquidity challenges and securing favorable refinancing terms. While the company's strategic pivot to high-margin sectors and strong EPS performance offer hope, the 217% OFCF payout ratio and $25 million 2026 debt maturity pose significant risks. For income investors, Luxfer represents a high-reward, high-risk proposition-ideal for those with a tolerance for volatility and a belief in the company's ability to navigate its refinancing hurdles.

Comentarios

Aún no hay comentarios