Lulus Shares Jump 66% in a Year: Should You Buy the Stock?

Lulu's Fashion Lounge Holdings, Inc. LVLU shares have surged 65.6% in the past year compared with the industry’s 18.3% growth. The company has outperformed other industry players, including Deckers Outdoor Corporation DECK and Stitch Fix, Inc. SFIX. Shares of DECK and SFIX have declined 19.3% and 29.3%, respectively, in the same time frame. LVLULVLU-- benefits from strong digital brand positioning, data-driven merchandising, improved product margins and expanding wholesale partnerships, supporting growth alongside continued focus on occasion wear demand.

Image Source: Zacks Investment Research

A Key Look Into LVLU’s Business Operations

Lulus is a digitally native, primarily online attainable luxury fashion brand for women, focused on modern feminine designs at accessible prices for life’s key occasions. Serving mainly Millennial and Gen Z customers, the brand emphasizes strong relationships with its community through personalized styling services, customer feedback and active engagement across digital platforms. Its data-driven “test, learn, and reorder” model allows the company to launch hundreds of new styles weekly, test demand in small batches and quickly scale successful products, reducing inventory risk and markdowns. The company also sees opportunities in international expansion and product innovation, supported by proprietary technology, predictive analytics and strong supplier relationships.

Lulus’ Key Tailwinds

The company benefits from its strong positioning as a digitally native fashion brand focused on occasion wear and event-driven apparel. It primarily targets Millennial and Gen Z consumers, a demographic that often discovers the brand in their early adult years and continues engaging with it across multiple life stages. This creates opportunities for repeat purchases and long-term customer relationships. In addition, the company uses a data-driven “test, learn, and reorder” merchandising model that enables it to identify successful styles early and restock them quickly. By leveraging real-time transaction data and customer feedback, the company can respond efficiently to changing fashion trends and evolving consumer preferences.

Another supportive factor is the company’s improving merchandise mix and product margins. Recent performance reflects benefits from reduced markdown activity, improved product sourcing, and a higher proportion of full-price sales. Its assortment includes its proprietary Lulus brand, exclusive designs developed with partners and selected third-party brands. Merchandise designed internally or sold exclusively through the platform generally carries higher margins than third-party products, supporting profitability.

The company is also expanding its distribution strategy beyond its traditional direct-to-consumer channel. While the brand initially built its presence through its online platform, it has increasingly developed partnerships with wholesale retailers to broaden its reach. A recent milestone includes expanding its presence into all Nordstrom stores nationwide following strong in-store performance and retailer confidence in the brand. These partnerships allow the company to introduce its products to new customers in physical retail environments while continuing to strengthen brand awareness. Management views wholesale expansion as complementary to its digital business, enabling broader exposure without abandoning its core direct-to-consumer strategy.

Demand for event-driven fashion categories also provides meaningful growth opportunities for the company. The brand has established itself as a destination for occasion wear, including dresses for weddings, proms and other social events. As consumer spending on experiences and celebrations continues to recover, demand for these categories may remain resilient. The company’s focus on design, customer engagement, and differentiated product offerings positions it well within this niche.

Challenges Persist for LVLU’s Business

The company faces several headwinds that continue to pressure its financial performance. Demand for its products is sensitive to macroeconomic conditions, such as inflation, higher interest rates, the resumption of student loan repayments and declining consumer confidence, all of which can reduce discretionary spending on apparel. In addition, sales have been affected by lower order volumes and shifting product mix, which has contributed to declining revenue and increased return rates. Rising borrowing levels and higher interest expenses also add financial strain, while the company continues to report operating losses and accumulated deficits.

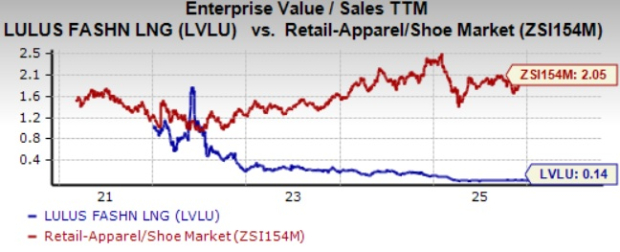

Lulus’ Valuation

The company is cheaply priced compared with the industry average. Currently, LVLU is trading at 0.14X trailing 12-month EV/sales value, below the industry’s average of 2.05X. The metric also remains lower than that of one of the company’s peers, Deckers Outdoor (2.51X), but matches that of Stitch Fix.

Image Source: Zacks Investment Research

Conclusion

The company’s strong brand positioning, data-driven merchandising strategy, and expanding wholesale partnerships provide a solid foundation for long-term growth. However, persistent macroeconomic pressures, declining order volumes and ongoing operating losses may continue to weigh on near-term performance.

Strong fundamentals, coupled with LVLU’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolio.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Stitch Fix, Inc. (SFIX): Free Stock Analysis Report

Lulu's Fashion Lounge Holdings, Inc. (LVLU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios