lululemon Q4 Earnings Ahead: Should Investors Buy the Stock Now?

lululemon athletica inc. LULU is likely to witness top and bottom-line declines when it reports fourth-quarter fiscal 2025 results on March 17, after market close. The Zacks Consensus Estimate for fiscal fourth-quarter revenues is pegged at $3.6 billion, indicating a 0.3% decline from the year-ago quarter's reported figure.

The consensus estimate for the company's fiscal fourth-quarter earnings is pegged at $4.77 per share, suggesting a 22.3% decline from the year-ago quarter’s actual. Earnings estimates have moved down by a penny in the past 30 days.

The Vancouver-based company has been reporting steady earnings outcomes, as evident from its bottom-line surprise trends in the past several quarters. lululemon has a trailing four-quarter earnings surprise of 7.8%, on average. Given its positive record, the question is, can LULU maintain the momentum?

Earnings Whispers

Our proven model conclusively predicts an earnings beat for LULU this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

lululemon has an Earnings ESP of +0.39% and a Zacks Rank #3. You can see the complete list of today's Zacks #1 Rank stocks here.

Key Insights on Trends to Define LULU’s Q4 Results

lululemon is expected to report strong fourth-quarter fiscal 2025 results, citing strong holiday demand that is tracking results toward the high end of its prior guidance. In its recent guidance update, management expected fourth-quarter fiscal 2025 net revenues and EPS to be at the upper end of the previously mentioned $3.5-$3.59 billion and $4.66-$4.76, respectively. Solid holiday traffic, resilient demand from core customers and disciplined execution supported performance in the key selling season, helping offset broader macro uncertainty and promotional pressures across apparel retail.

lululemon continues to benefit from the progress with its Power of Three X2 growth strategy. The plan focuses on three key growth drivers — product innovation, guest experience and market expansion. LULU is expected to deliver solid revenue growth in the fiscal fourth quarter through product innovation, enhanced guest experience and aggressive international expansion, under the plan.

International markets, led by Mainland China, continue to post outsized growth, while the men’s category is gaining share. Digital investments are strengthening the omnichannel ecosystem and disciplined store expansion is supporting brand visibility.

However, lululemon’s margins are expected to remain under pressure in the to-be-reported quarter due to higher costs, rising markdowns and tariff impacts. A sharp fiscal fourth-quarter margin decline outlook and fixed-cost deleverage limit near-term profitability and leverage. The company’s performance in the Americas, predominantly the U.S. business, is expected to have reflected soft trends.

North America, lululemon’s largest and most mature market, has been witnessing a softness due to weaker traffic trends and increasingly cautious consumer spending, particularly in discretionary categories, as elevated inflation and higher interest rates pressured purchasing behavior. The impact has been most visible in the women’s category, a core driver of the brand’s North American business.

While international markets are accelerating, slower momentum in North America limits consolidated growth and raises concerns about market saturation. Until demand stabilizes and traffic improves, North America is likely to remain a drag on near-term revenue growth and investor sentiment.

On its last reported quarter’s earnings call, management projected revenues in the Americas to be flat to down 1%, indicating a 1% decline in the United States and nearly stable performance in Canada. Our model predicts revenues for the Americas business to decline 4.3% year over year for the fourth quarter and 2% for fiscal 2025.

lululemon athletica inc. Price and EPS Surprise

lululemon athletica inc. price-eps-surprise | lululemon athletica inc. Quote

Headwinds from ongoing uncertainty stemming from increased tariffs on imports from China and Mexico are likely to have led to higher costs. This, along with heavy markdowns and fixed-cost deleverage, is expected to have pressured the gross margin in the to-be-reported quarter.

On the last reported quarter’s earnings call, management expected higher tariff rates and the removal of the de minimis exemption, along with fixed cost deleverage and continued investment in its multi-year distribution center to hurt the gross margin in fiscal 2025. For fiscal 2025, lululemon expected a 270-bps year-over-year decline in the gross margin. We expect adjusted gross profit to decline 10.3% in the fourth quarter and 0.4% in fiscal 2025.

lululemon also faces SG&A expense deleverage due to planned investments in strategies and initiatives to fuel long-term growth. These investments include digital marketing and seasonal store openings to drive guest acquisition, build brand awareness and expand testing for longer-term growth opportunities.

On its last reported quarter’s earnings call, the company expected the SG&A expense rate to increase 120 bps year over year for fiscal 2025. While the company continues to manage expenses prudently, it is stepping up marketing investments in the fiscal fourth quarter to drive traffic and strengthen brand awareness. LULU expects the fiscal 2025 operating margin to contract 390 bps year over year.

For the fourth quarter of fiscal 2025, management anticipated SG&A, as a percentage of sales, to deleverage 100 bps year over year, led by higher foundational investments, including related depreciation and strategic initiatives to enhance brand awareness and support growth. We expect the SG&A expense rate to increase 100 bps to 32.5%, with the operating margin declining 680 bps to 22.1% in the fiscal fourth quarter.

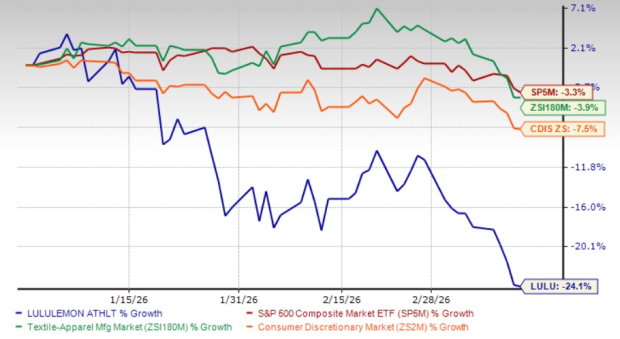

LULU’s Price Performance & Valuation

lululemon’s shares have exhibited a downtrend in the past six months, losing 24.1% compared with the industry’s fall of 3.9%. The company has also underperformed the Zacks Consumer Discretionary sector and the S&P 500’s declines of 7.5% and 3.3%, respectively.

lululemon’s YTD Performance

Image Source: Zacks Investment Research

The LULU stock has underperformed V.F. Corporation VFC, Ralph Lauren Corporation RL and PVH Corp. PVH, which have declined 11.8%, 6.5% and 9.2%, respectively, in the year-to-date period.

At its current price of $157.78, the LULU stock trades 0.7% above its 52-week low of $156.64, reached on March 13. lululemon’s current stock price stands 54.7% below its 52-week high of $348.50.

From the valuation standpoint, the company trades at a forward 12-month P/E multiple of 12.24X, below the industry average of 17.55X.

Image Source: Zacks Investment Research

Investment Thesis

lululemon is facing a challenging retail backdrop, with inflation, rising interest rates and softer discretionary spending weighing on consumer behavior. Luxury and premium categories, particularly in the Americas, are under pressure, while tariffs remain an additional headwind. These factors have created a difficult environment for growth, but the company continues to execute on its long-term vision.

Momentum is being driven by its Power of Three ×2 strategy, which targets doubling of revenues by 2026 through three pillars — international expansion, growth in the men’s business and enhanced digital engagement. This multi-pronged approach is helping lululemon balance near-term challenges with structural growth opportunities.

International markets stand out as a key driver, with China playing a central role in lululemon’s plan to significantly scale global revenues. Alongside digital investments that deepen customer engagement and a growing men’s apparel segment, lululemon is positioning itself for resilience and long-term value creation.

Conclusion

No matter how the stock responds to the upcoming fourth-quarter fiscal 2025 results, lululemon’s disciplined execution and strong brand equity continue to support its long-term outlook. Progress under the Power of Three ×2 strategy, led by international expansion, digital engagement and momentum in the men’s category, provides meaningful growth avenues.

However, near-term challenges, including softer demand in the Americas, tariff-related cost pressures and margin deleverage, are likely to weigh on lululemon’s upcoming results. Given these offsetting factors, investors may prefer to stay cautious and wait for clearer signs of demand stabilization in North America before turning more constructive on the stock. For existing shareholders, the long-term strategy provides a basis for staying the course.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

V.F. Corporation (VFC): Free Stock Analysis Report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

lululemon athletica inc. (LULU): Free Stock Analysis Report

PVH Corp. (PVH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios