Lower for Longer: Why China's Bond Yields Offer a Strategic Hedge Against Deflation and Currency Stability

The People's Bank of China (PBOC) has positioned itself as the global custodian of ultra-low yields, with China's 10-year government bond yield hovering near historic lows of 1.65% amid persistent deflation and a deliberate policy of monetary accommodation. For investors seeking shelter in a world of tariff wars, weak growth, and currency volatility, this environment presents a compelling case for overweighting Chinese government bonds as a defensive asset class. Let's dissect the drivers behind this “lower for longer” regime and why it's a strategic hedge against deflation and yuan instability.

The Deflationary Feedback Loop: Why Yields Won't Budge

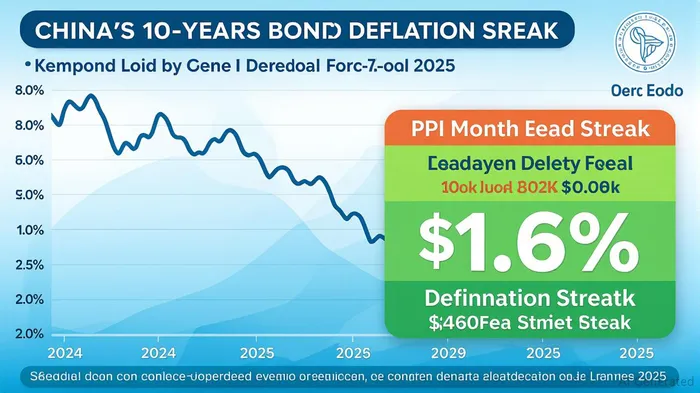

China's bond market is being held captive by a deflationary spiral that shows no signs of abating. Producer prices have now declined for 33 consecutive months, with the June 2025 PPI dropping 3.6% year-on-year—the steepest decline since 2023. Weak consumer demand, stagnant wage growth, and a collapsed housing market (new home prices down 4.8% YoY) have created a self-reinforcing cycle: falling prices → reduced spending → weaker economic activity → lower inflation expectations.

This dynamic has left the PBOC with little choice but to keep rates anchored near zero. Analysts at Guoshen Securities project the 10-year yield to dip further to 1.4–1.6% by late 2025, with the PBOC's 7-day reverse repo rate—now at 1.5%—remaining steady through 2026.

PBOC Liquidity Management: A Tightrope Walk

The central bank's dual mandate—stabilizing the yuan and supporting growth—has led to a mix of unconventional tools:

- Targeted Liquidity Injections: A 1 trillion yuan RRR cut in 2025 injected liquidity into regional banks, encouraging low-interest loans (some as low as 3.4% for mortgages) to prop up housing and SMEs.

- Yield Curve Control: By halting government bond purchases and sterilizing foreign exchange outflows, the PBOC has kept long-term yields suppressed.

- Digital Yuan Expansion: The e-CNY's rollout in trade settlements reduces reliance on dollar financing, indirectly supporting yuan stability.

However, these measures have done little to spark credit demand, which remains anemic. Commercial banks report 70% of new loans are tied to policy-driven sectors like elderly care and infrastructure—proof of a credit market held up by artificial demand, not organic growth.

The US-China Yield Gap: A Double-Edged Sword

The spread between China's 10-year yield and U.S. Treasuries has narrowed to ~230 bps in July 2025, down from peaks of 250 bps earlier this year. This is driven by:

- U.S. Fed Dovishness: Expectations of a September 2025 rate cut (to 4.5%) have dragged U.S. yields down from 4.4% highs.

- Yuan Stability: A weaker yield gap reduces capital flight risks; the yuan has stabilized near 7.25/USD, aided by PBOC's policy of modest appreciation to ease trade tensions.

However, risks remain: further U.S. tariff hikes (now at 30% on $200B of Chinese goods) could reignite inflation and widen the gap again.

Investment Case: Overweight Chinese Bonds as a Defensive Play

Why Bonds, Not Equities?

- Deflation Hedge: Bonds thrive in low-growth, low-inflation environments. China's 10-year yield offers a 0.7% real return (vs. -0.1% CPI), making it a better inflation-protected asset than equities.

- Currency Stability: A narrowing yield gap reduces yuan volatility, making bonds a safer haven than volatile stocks or real estate.

- Tariff Mitigation: Bonds act as a “buffer” against trade wars; their steady coupons offset earnings volatility in tariff-hit sectors like manufacturing.

Strategic Recommendations:

- Duration Overweight: Add 5–10% to portfolios via iShares China Bond ETF (CGB) or direct purchases of 10-year government notes.

- Ladder Maturity Risks: Focus on 3–5-year bonds to avoid capital losses if yields eventually rise.

- Pair with Yuan Exposure: Use FX forwards (e.g., CNH/USD) to lock in current exchange rates and protect against unexpected devaluations.

Risks and the Long-Term Outlook

- Policy Overreach: If the PBOC cuts rates further, it risks inflating asset bubbles (e.g., in real estate) and undermining debt sustainability.

- Global Recession: A U.S./Europe slowdown could deepen China's deflation, pushing yields even lower.

Yet, the base case remains clear: with deflation entrenched and the PBOC's hands tied by weak growth, lower for longer is not a prediction—it's a policy. For investors, this is a call to treat Chinese bonds not as a temporary trade, but as a core defensive holding.

Final Takeaway: In a world of geopolitical storms and deflationary headwinds, China's bond market offers a rare oasis of stability. The “lower for longer” yield regime, supported by policy and economics, makes it a must-hold defensive asset for 2025 and beyond.

Comentarios

Aún no hay comentarios