Lloyds' Additional $1.07 Billion Provision for Mis-Sold Car Loans: Risk Management and Long-Term Valuation Implications for UK Banking Stocks

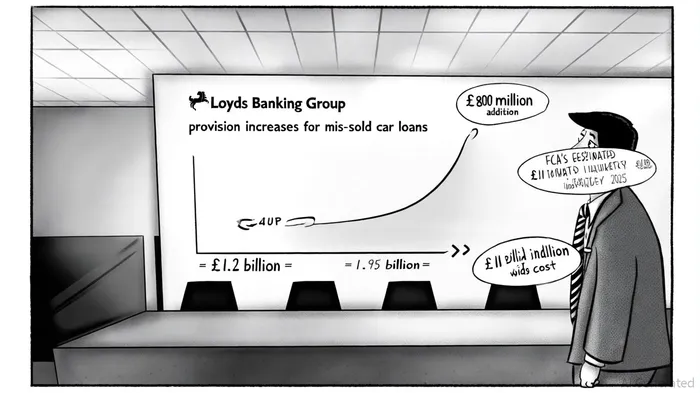

Lloyds Banking Group's recent announcement of an additional £800 million provision-converted to approximately $1.07 billion at the time, in a Yahoo Finance roundup-for its mis-sold car loan scandal has reignited scrutiny over risk management practices and long-term valuation risks in the UK banking sector. This provision, which brings Lloyds' total exposure to £1.95 billion, according to a Sky News report, underscores systemic vulnerabilities in the motor finance industry and raises critical questions about the adequacy of current regulatory frameworks.

Risk Management: A Test of Resilience

Lloyds' initial £1.2 billion provision proved insufficient as the Financial Conduct Authority (FCA) expanded its proposed redress scheme to cover up to 14 million car finance agreements, with average payouts of £700, according to the Scottish Financial Review. The bank's warning of potential "material" further charges, noted by Sky News, highlights a key risk: the disconnect between regulatory redress methodologies and actual customer losses. LloydsLYG-- has criticized the FCA's approach for not fully accounting for the financial harm caused by discretionary commission arrangements (DCAs), which allowed dealers to inflate interest rates to boost commissions, as reported by the Scottish Financial Review.

This misalignment exposes a broader issue in risk management: the reliance on static provisioning models in a dynamic regulatory environment. While Lloyds' updated £1.95 billion provision reflects a more conservative stance, analysts at Jefferies note that the bank's exposure could still outpace its current reserves, as covered in the Yahoo Finance roundup. For context, the FCA's estimated £11 billion industry-wide cost, reported by Sky News, suggests that Lloyds, as a dominant player in the motor finance market, remains disproportionately vulnerable.

Industry-Wide Implications and Systemic Risks

The scandal has ripple effects across the UK banking sector. Competitors like Close Brothers are likely to face similar pressure to increase provisions, the Scottish Financial Review warns, amplifying sector-wide capital outflows. This scenario could strain liquidity and capital ratios, particularly for banks with limited diversification. The FCA's focus on DCAs-a practice banned in 2021, per the Scottish Financial Review-also signals a regulatory shift toward retrospective accountability, which may force banks to revisit historical lending practices.

From an investor perspective, the FCA's proposed scheme introduces uncertainty in earnings forecasts. For Lloyds, the £1.95 billion provision represents a significant drag on profitability, with potential further charges threatening its ability to meet regulatory capital thresholds. Moody's and S&P have already flagged the need for closer monitoring of UK banks' capital buffers, a development Sky News has highlighted, that could impact credit ratings and borrowing costs.

Long-Term Valuation Impacts

The long-term valuation of UK banking stocks hinges on how effectively institutions like Lloyds navigate these challenges. While the immediate cost of the provision is substantial, the broader impact lies in eroded investor confidence and higher compliance costs. Lloyds' dominance in the motor finance market-accounting for over 30% of UK car loans, according to the Scottish Financial Review-means its struggles could serve as a bellwether for sector-wide profitability.

Moreover, the scandal underscores the growing importance of ESG (Environmental, Social, and Governance) factors in banking valuations. The mis-selling of car loans, driven by opaque commission structures, has damaged Lloyds' reputation for ethical lending. As institutional investors prioritize ESG alignment, banks with poor risk governance frameworks may face higher equity costs and reduced market multiples.

Conclusion: A Call for Prudent Investment Strategies

Lloyds' $1.07 billion provision is a stark reminder of the fragility of risk management in a post-crisis banking landscape. While the bank's updated reserves reflect a more cautious approach, the potential for further charges and regulatory scrutiny necessitates a reevaluation of its long-term value proposition. For UK banking stocks broadly, the incident highlights the need for robust governance, transparent provisioning practices, and proactive alignment with regulatory priorities.

Investors should remain cautious, particularly as the FCA's redress scheme unfolds. Diversification into banks with stronger capital buffers and lower exposure to high-risk lending segments may offer a more resilient portfolio strategy in the coming years.

Comentarios

Aún no hay comentarios