LIXTE's Platform Pivot: A High-Stakes Bet on Clear Cell Ovarian Cancer

LIXTE Biotechnology's strategic pivot is a direct response to the structural dynamics of the rare cancer market it targets. The company is attempting to transition from a single-drug biotech to a multi-asset oncology platform, a move driven by the high unmet need in its core indication, ovarian clear cell carcinoma (CCOC). This subtype represents approximately 10 to 12% of all ovarian cancers and is characterized by distinct biology and high chemoresistance, creating a clear niche for novel therapies. The company's lead compound, LB-100, is being advanced in clinical trials for this specific patient population, underscoring the focus on a defined, high-need segment.

The financial opportunity for this shift is substantial and growing. The global market for CCOC treatments is projected to expand from USD 2.7 Billion across the top 7 markets in 2024 to USD 5.8 Billion by 2035, a compound annual growth rate of 7.23%. This projected doubling of the market size over a decade provides a compelling tailwind for a company building a focused oncology portfolio. LIXTE's management has confirmed it is in advanced negotiations regarding potential transactions to acquire complementary oncology assets, aiming to build a differentiated platform that can capture a share of this expanding pie.

The central investor question is whether this platform model can overcome the capital and execution hurdles inherent in a small biotech. Building a pipeline through acquisitions introduces significant complexity and risk, particularly for a company that must simultaneously fund clinical development and navigate the integration of new assets. The strategic move is logical from a market perspective, as it seeks to diversify beyond a single clinical candidate and create a more resilient business. However, the execution will be paramount. The company must demonstrate it can not only secure and integrate acquisitions but also efficiently advance multiple programs to generate clinical and commercial value. The pivot represents an attempt to scale a niche opportunity, but its success hinges on the company's operational and financial capacity to execute a complex growth strategy.

Clinical Execution: Validating the Platform's Core Mechanism

The operational story at LIXTELIXT-- is now in motion, with the expanded trial footprint providing a tangible test of its core scientific premise.  The company has successfully added the Robert H. Lurie Comprehensive Cancer Center as a second site for its ovarian clear cell carcinoma trial. This is more than just a site addition; it accelerates patient recruitment and validates the collaborative model. By enlisting a National Cancer Institute-designated center, LIXTE is demonstrating its ability to attract top-tier academic partners, a critical step for credibility and execution.

The company has successfully added the Robert H. Lurie Comprehensive Cancer Center as a second site for its ovarian clear cell carcinoma trial. This is more than just a site addition; it accelerates patient recruitment and validates the collaborative model. By enlisting a National Cancer Institute-designated center, LIXTE is demonstrating its ability to attract top-tier academic partners, a critical step for credibility and execution.

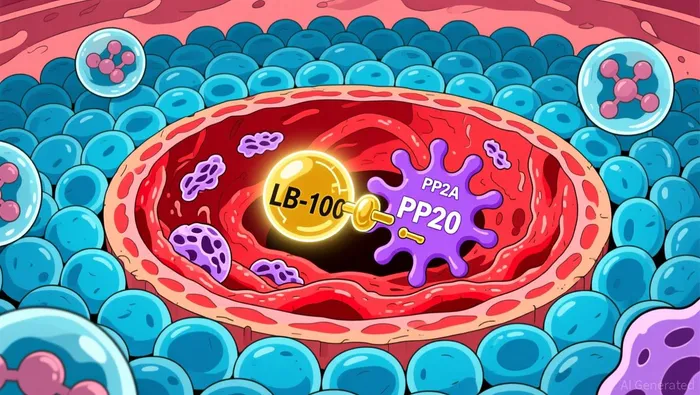

The central question is whether this expanded clinical activity can de-risk the platform story. The company's strategy hinges on LB-100 acting as a combination therapy enhancer, aiming to overcome resistance by making tumors more visible to immunotherapy and more vulnerable to chemotherapy. The mechanism is counterintuitive but precise: LB-100 temporarily inhibits the PP2A enzyme, pushing cancer cells into a state of stress and proliferation that makes them easier targets for subsequent treatments. The upcoming data will be the ultimate validation of this "activation lethality" concept.

The near-term catalysts are concentrated in the second half of 2025, creating a clear inflection point. LIXTE anticipates preliminary efficacy data in Q4 2025 from its ovarian clear cell carcinoma trial. This is the first major readout and will signal whether the combination works in a high-unmet-need setting. Further data from other trials-PFS and ORR data in late Q3 2025 from the soft tissue sarcoma trial and initial biomarker and response data in Q4 2025 from the metastatic colon cancer trial-will provide a broader picture of the drug's potential across different tumor types.

The bottom line is that clinical execution is now the primary narrative driver. The expanded trial footprint shows operational progress, but the market will be watching for the hard data. Positive results across these trials could transform LIXTE from a speculative biotech into a platform with validated utility, potentially attracting partnerships and de-risking the broader oncology strategy. Negative or mixed results, however, would likely reinforce the perception of high clinical uncertainty. The coming months will separate the platform's theoretical promise from its practical performance.

Risk & Guardrails: The Platform's Achilles' Heel

The investment thesis for Lixte hinges on a single, unproven mechanism. The core risk is clinical: LB-100's proposed "activation lethality" strategy is a first-in-class approach with no established track record in humans. The company's premise-that temporarily disabling the PP2A "off switch" can sensitize tumors to chemo and immunotherapy-is scientifically ambitious but untested at scale. The proof-of-concept trials in ovarian clear-cell carcinoma, metastatic colon cancer, and soft-tissue sarcomas are critical. Failure to demonstrate a clear, statistically significant benefit over standard care in these high-need settings would undermine the entire platform narrative and likely collapse the stock.

Execution risk is equally high. The company is attempting a rapid pivot from a single-drug biotech to a multi-asset oncology platform. This requires successful integration of acquired assets, like the recently closed Liora Technologies Europe Ltd., and building robust quality, CMC (chemistry, manufacturing, and controls), and regulatory systems. As the October 2025 press release notes, the company is in "advanced negotiations" on further acquisitions. For a firm with a market value of roughly US$25–27 million, this is a significant operational challenge. The leadership's M&A background is a tool, but integrating disparate technologies and clinical pipelines under a tight budget is a complex, high-stakes task that can derail timelines and burn cash.

Financial sustainability is the third, immediate guardrail. With a treasury policy that allows up to 50% of its reserves to be held in cryptocurrencies, the company is adding an unnecessary layer of volatility to its balance sheet. The recent purchase of 10.5 bitcoinBTC-- and 300 ether for about US$2.6 million represents a meaningful portion of its capital. This speculative allocation is a stark contrast to the capital discipline required for clinical development. The company's two financings in 2025 totaling US$6.5 million underscore its cash-constrained reality. Any delay in clinical readouts or acquisition integration could quickly exhaust this runway, forcing dilutive equity raises at depressed valuations.

The bottom line is that Lixte is betting everything on a high-risk, high-reward platform strategy. Investors must monitor three concrete metrics: clinical readouts from the ongoing Phase 2 trials, the successful integration of the proton-therapy platform and any future acquisitions, and the company's cash burn rate against its treasury policy. The crypto allocation is a red flag, not a feature. It signals a balance sheet exposed to two volatile markets-drug development and digital assets-making the path to a sustainable, profitable oncology franchise exceptionally narrow.

Valuation & Catalysts: Pricing the Asymmetric Bet

The stock trades around $4.17, a level that reflects a high-risk, binary bet on the next 12 to 18 months. This price is a direct function of the company's clinical and strategic timeline. The primary catalyst is the Q4 2025 data readout from the Phase 1b/2 trial of LB-100 in ovarian clear cell carcinoma (OCCC). Positive efficacy results here could unlock immediate partnership or acquisition interest, providing a capital infusion and validating the platform's potential. Conversely, negative or inconclusive data would likely be catastrophic for the stock, as it would undermine the core value proposition of LB-100 as a combination therapy enhancer.

A secondary, but equally critical, catalyst is the outcome of acquisition talks. The company has confirmed it is in advanced negotiations regarding potential transactions for complementary oncology assets. A successful deal could provide a much-needed boost to the pipeline and balance sheet, accelerating development. A failed negotiation, however, would signal a lack of partner interest and could further pressure the stock, especially if the company is forced to fund its growth independently.

The valuation is asymmetric. On the upside, the platform's potential scale is substantial. LB-100 is being tested across three major unmet needs: OCCC, soft tissue sarcoma, and microsatellite-stable colon cancer. If it demonstrates consistent efficacy as a sensitizer to existing chemotherapies, it could command a premium valuation. On the downside, the failure modes are clear. The stock's current price already discounts significant execution risk. Any delay in clinical data, a failure to secure a strategic partner, or a deterioration in the company's cash position would likely trigger a sharp de-rating.

The bottom line is that investors are paying for a story that hinges on two specific events in late 2025. The market is pricing in a high probability of failure, hence the low stock level. The re-rating potential is binary: a successful data readout and/or a strategic deal could propel the stock meaningfully higher, while any stumble would likely lead to a collapse. Monitoring the December 30th trading session post-split is a compliance checkpoint, but the real valuation inflection will come from the clinical and business development milestones in the coming quarters.

Comentarios

Aún no hay comentarios