Limbach Holdings: Navigating the Post-Recovery Infrastructure Landscape with Strategic Precision

In the aftermath of a global economic recovery, the industrial and infrastructure services sector is undergoing a transformation defined by pragmatism, technological integration, and recalibrated risk management. Limbach HoldingsLMB-- (NASDAQ:LMB) has emerged as a standout player in this evolving landscape, leveraging its strategic focus on high-margin, recurring revenue streams and disciplined capital allocation. For investors, the question is whether Limbach's current trajectory-marked by robust financial performance and aggressive expansion-can sustain its momentum amid a backdrop of both opportunity and uncertainty.

Financial Performance: A Recipe for Resilience

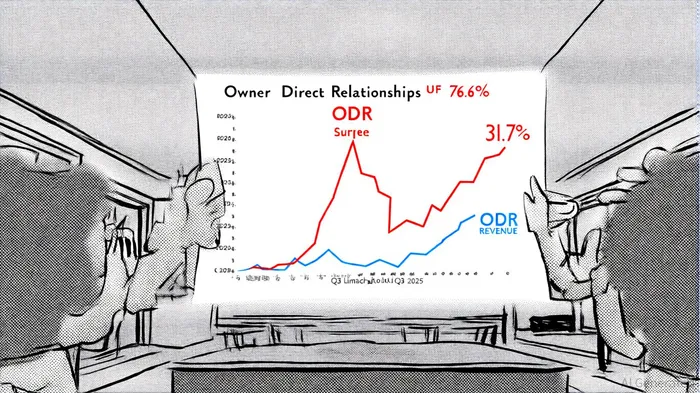

Limbach's second-quarter 2025 results underscore its ability to capitalize on post-recovery demand. Total revenue surged 16.4% year-over-year to $142.2 million, driven by a 31.7% increase in Owner Direct Relationships (ODR) revenue to $108.9 million, which now accounts for 76.6% of total revenue, according to Limbach's press release. This shift toward ODR-a segment characterized by long-term contracts with building owners-has not only stabilized cash flows but also amplified gross margins. Adjusted EBITDA rose 30% to $17.9 million, outpacing revenue growth and signaling operational efficiency.

The company's strategic investments further reinforce its growth narrative. A $100 million credit facility expansion and the $66.1 million acquisition of Pioneer Power, Inc. demonstrate Limbach's commitment to scaling its ODR business while diversifying into adjacent markets like energy services, the company said. These moves align with broader industry trends, where infrastructure firms are prioritizing recurring revenue models to buffer against cyclical volatility.

Strategic Positioning: ODR as a Growth Engine

Limbach's focus on ODR is not merely tactical-it is existential. In a sector historically plagued by project-based volatility, the company has repositioned itself as a provider of essential building systems solutions, offering services such as HVAC, electrical, and plumbing to existing infrastructure. This model mirrors the shift seen in software-as-a-service (SaaS) businesses, where customer retention and upselling drive compounding growth.

According to a KPMG report, digitization and sustainability are reshaping infrastructure services in 2025, with digital twin technology and AI-driven asset management becoming critical differentiators. Limbach's investments in a national sales organization and digital tools position it to capture these trends. For instance, its enhanced go-to-market strategy enables deeper penetration into large commercial and industrial clients, many of whom are now prioritizing energy efficiency and decarbonization, the company reported.

Industry Tailwinds and Headwinds

The post-recovery infrastructure sector is a double-edged sword. On one hand, the energy transition and AI-driven demand for data centers are fueling infrastructure spending. On the other, supply chain bottlenecks, geopolitical tensions, and regulatory shifts-such as the U.S. re-withdrawing from the Paris Agreement under Trump 2.0-introduce volatility, according to Goldman Sachs.

Limbach's risk-rebalance potential lies in its ability to insulate itself from these headwinds. Its ODR model, with its emphasis on existing infrastructure, is less exposed to the capital-intensive demands of new construction. Additionally, the company's recent acquisition of Pioneer Power, a provider of electrical infrastructure solutions, aligns with the U.S. government's push for grid modernization-a $1.2 trillion market opportunity by 2030, KPMG projects.

However, challenges remain. Supply chain volatility could erode margins if component costs for HVAC or electrical systems spike. Moreover, the infrastructure sector's reliance on public-private partnerships means policy shifts-such as changes in federal funding for green energy-could disrupt long-term planning.

Risk Mitigation: A Framework for Resilience

Limbach's approach to risk mirrors the strategies outlined in the 2025 National Infrastructure Risk Management Plan, which emphasizes collaboration and proactive mitigation, KPMG notes. By expanding its credit facility and diversifying its service offerings, the company has strengthened liquidity and reduced overreliance on any single market. Furthermore, its adoption of Building Information Modeling (BIM) and digital twins aligns with industry best practices for predictive maintenance and real-time risk monitoring, the company reported.

Conclusion: A Calculated Bet on the Future

Limbach Holdings' strategic positioning in the post-recovery infrastructure sector is a masterclass in balancing growth and prudence. Its ODR-centric model, bolstered by technological investments and disciplined capital allocation, offers a compelling value proposition in an era of uncertainty. Yet, the company's success will ultimately depend on its ability to navigate geopolitical and supply chain risks while maintaining its margin expansion. For investors, LimbachLMB-- represents a calculated bet on the future of infrastructure-one where resilience and adaptability are as valuable as revenue growth.

Comentarios

Aún no hay comentarios