What Could Lift Energy Fuels' Uranium Margins in 2026?

Energy Fuels UUUU is heading into 2026 with a clearer path to better uranium unit economics. Higher mill utilization, improving cost absorption and a larger share of lower-cost feed are expected to strengthen operating leverage as volumes rise.

Still, investors should separate operational progress from reported revenue timing. Contract mix, delivery cadence and inventory decisions can create lags even when fundamentals improve.

The Setup Behind Better Unit Economics for Energy Fuels

The White Mesa Mill is central to the company's margin story. In the fourth quarter of 2025, the mill ran at roughly 250,000 pounds per month, and output peaked at 350,000 pounds in December, a setup that supports stronger cost absorption in 2026.

Operating leverage is expected to show up in finished inventory costs. Weighted average finished inventory costs were about $43 per pound at year-end 2025, and the expectation is for those costs to move into the low $30s during 2026 as processing scales and feed quality improves.

UUUU’s 2026 Volumes, Sales, and Delivery Commitments

Management expects to mine 2–2.5 million pounds of uranium and process 1.5–2.5 million pounds in 2026. On the commercial side, uranium sales are projected at 1.5–2 million pounds through a mix of contract shipments and spot transactions. These sales plans sit alongside contracted deliveries of roughly 620,000–880,000 pounds in 2026, which sets a baseline for volumes that should move through income statements over time.

At year-end 2025, Energy FuelsUUUU-- held 810,000 pounds of finished uranium and 2.18 million pounds of finished and contained inventory in total. This can support delivery requirements and provide flexibility to pursue opportunistic spot sales when pricing is attractive.

The tradeoff is timing. If management chooses to build inventory rather than sell, near-term reported revenues can shift, even if operational momentum improves. This flexibility can help value maximization over a cycle, but it can also make quarterly comparisons harder for investors to interpret.

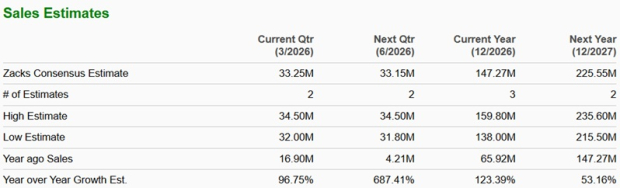

The Zacks Consensus Estimate for Energy Fuels’ revenues for 2026 is $147.27 million, suggesting 123.4% year-over-year growth.

Image Source: Zacks Investment Research

Contracts Add Volume With Market-Linked Upside

A key support for 2026–2032 volumes is the company’s long-term contracting. Energy Fuels has six long-term contracts with U.S. utilities covering deliveries from 2026 through 2032. Those agreements include 3.21 million pounds of committed base sales. With customer options, the potential total delivery range expands to 3.71-5.29 million pounds, which can add volume while preserving upside if market-linked pricing continues to work in the company’s favor.

Why Reported Revenues May Lag Even if Operations Improve

Operational improvement does not guarantee immediate revenue acceleration. First-quarter 2026 realizations are expected to be lower due to legacy contracts signed in 2022, while newer contracts are described as back-half weighted.

Management also has discretion over whether to sell, store, or even buy spot pounds if prices soften. These choices can delay revenue recognition and shift when earnings momentum shows up in the financials, even if cost trends and throughput are moving the right way.

What the Short-Term Rating for Energy Fuels Signals Now

From a near-term investor lens, Energy Fuels presently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Its Style Scores skew weak overall, with VGM Score of F, Value Score of F, Growth Score of F, and Momentum Score of C.

That mix suggests investors may want clearer evidence of execution before paying up for the 2026 margin narrative. For context, Cameco Corporation CCJ and Centrus Energy Corp. LEU also currently carry a Zacks Rank of 3 in the same industry comparison set, underscoring that the group’s near-term setup can be more about delivery and pricing dynamics than broad-based rating support.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cameco Corporation (CCJ): Free Stock Analysis Report

Energy Fuels Inc (UUUU): Free Stock Analysis Report

Centrus Energy Corp. (LEU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios