Lifco's Q3 Earnings as a Catalyst for Long-Term Growth

Financial Performance: Navigating Margin Pressures

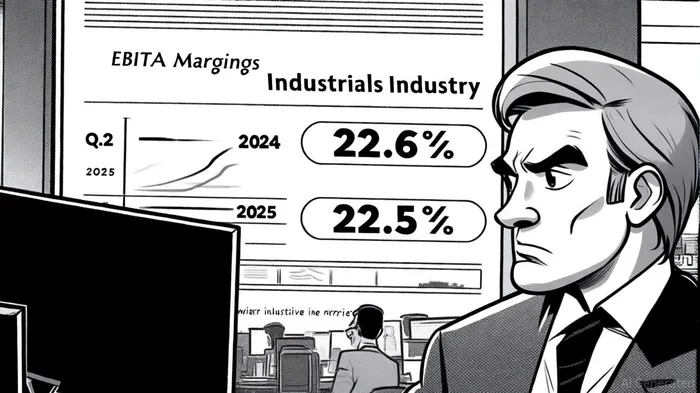

Lifco's Q2 2025 results revealed a 3.2% year-over-year revenue increase to SEK 6,943 million, yet EBITA margins contracted to 22.5% from 23.9% in the prior-year period, according to Lifco's interim report. This decline was attributed to a negative product mix in key segments like Demolition & Tools and Systems Solutions, as well as timing-related challenges tied to Easter. While such short-term headwinds are not uncommon in cyclical industries, they underscore the importance of operational discipline.

The company's cash flow from operating activities also fell by 8.5% to SEK 971 million in Q2 2025, driven by increased working capital in the Contract Manufacturing division, per the interim report. These figures highlight the fragility of maintaining high-margin performance in a fragmented industrial sector. However, Lifco's historical resilience-demonstrated by a 15.1% average annual earnings growth rate over the past five years, as shown by Simply Wall St-suggests that its long-term trajectory remains intact.

Strategic Acquisitions: Fueling Growth Amid Margin Constraints

Lifco's acquisition strategy has been a cornerstone of its growth narrative. In the first half of 2025 alone, the company consolidated seven businesses, including Arnold Deppeler in the Dental segment and Italgears in Systems Solutions, according to the interim report. These acquisitions not only diversify Lifco's revenue streams but also align with its focus on niche, market-leading businesses. By integrating high-margin, specialized operations, Lifco aims to offset margin pressures in its core segments.

However, the success of this strategy hinges on effective integration and cost synergies. For instance, the Contract Manufacturing division's working capital challenges in Q2 2025 suggest that post-acquisition operational alignment remains a critical test. Investors will need to monitor how Lifco balances the short-term costs of integration with the long-term benefits of scale.

Sustainability as a Strategic Lever

Lifco's sustainability initiatives are not merely compliance-driven but deeply embedded in its growth strategy. The company has set science-based climate targets validated by the Science Based Targets initiative (SBTi), including a 42% reduction in absolute Scope 1 and 2 greenhouse gas emissions by 2030 from a 2023 baseline, as detailed on Lifco's sustainability page. This commitment is reinforced by its 2024 Annual and Sustainability Report, which emphasizes sustainability as a core component of its acquisition criteria.

These efforts are not just reputational assets; they also create tangible value. For example, Lifco's focus on sustainability supports its customers' decarbonization goals, potentially securing long-term contracts in sectors like healthcare and industrial manufacturing. Moreover, its 2025 sustainability roadmap includes a target for 10% of customers by revenue to adopt science-based targets by 2029, aligning its growth with global decarbonization trends described on the sustainability page.

Long-Term Outlook: Balancing Risks and Rewards

While Lifco's Q3 2025 earnings will provide a more granular view of its financial health, the broader narrative remains one of cautious optimism. The company's ability to navigate margin pressures through strategic acquisitions and sustainability-driven differentiation is a key strength. However, risks persist, including macroeconomic volatility and the execution challenges inherent in rapid expansion.

For investors, the critical question is whether Lifco can translate its sustainability commitments into measurable financial outcomes. A 22.6% EBITA margin in 2024 places it above the Industrials industry average, but maintaining this edge will require continued innovation and operational rigor. The upcoming Q3 report, coupled with the October 24 webcast featuring CEO Per Waldemarson and CFO Therése Hoffman, will offer insights into how the company plans to address these challenges (see the Marketscreener article referenced above).

Conclusion

Lifco's Q3 2025 earnings represent more than a quarterly update-they are a litmus test for the company's ability to harmonize margin expansion with sustainability leadership. In a high-margin consumer sector increasingly shaped by ESG criteria, Lifco's dual focus on profitability and planetary responsibility could position it as a leader in the next phase of industrial evolution. Investors who prioritize long-term value creation over short-term volatility may find Lifco's strategic trajectory both compelling and resilient.

Comentarios

Aún no hay comentarios