LASR Stock: Defense Backlog vs. Margin Risk in 2026 Outlook

nLIGHT LASR is entering 2026 with a defense-led growth story that is gaining credibility. Aerospace and defense (A&D) momentum improved through 2025 as late-stage programs progressed and the business mix continued shifting toward higher-value offerings.

At the same time, the 2026 setup is not just about demand. Revenue timing, product mix and factory utilization will likely decide how smooth the earnings path looks from quarter to quarter.

LASR’s Near-Term Setup Starts With Defense Momentum

Defense demand is the core driver behind LASR’s improved visibility. A&D revenues climbed 60% year over year in 2025 to $175 million, supported by stronger shipments and program execution. Management is targeting total growth in 2026 with double-digit A&D expansion. Funded backlog is expected to support that plan and reinforce a multi-year shift toward higher-value defense products as programs mature.

That mix shift matters because it can lift the quality of revenues over time. LASRLASR-- also broadened its defense footprint beyond directed energy as laser sensing moved from design wins to production, helping diversify exposure and reduce reliance on one-off development milestones. LASR’s funded backlog of about $162 million as of Dec. 31, 2025, provides a baseline for 2026. However, nLIGHTLASR-- has indicated that additional “go-get” beyond the existing backlog is needed to achieve total 2026 growth, which widens outcomes if prototype awards slip.

The key issue is timing. Development revenues are milestone-driven, and funding and testing risk can shift deliveries across quarters. That can swing reported revenues, mix and cash generation even when program demand is intact. This is where dispersion shows up for investors. If milestone schedules reset or customer testing takes longer than expected, quarterly cadence can look uneven, even as longer-cycle defense programs remain on track.

For the first quarter of 2026, nLIGHT expects revenues between $70 million and $76 million. The Zacks Consensus Estimate for first-quarter 2026 revenues is pegged at $70.6 million, indicating 36.6% growth from the figure reported in the year-ago quarter. The consensus mark for earnings is currently pegged at 8 cents per share, up couple of cents over the past 30 days. LASR reported a loss of 4 cents per share in the year-ago quarter.

LASR’s Industrial Exit Creates a Measurable Headwind

LASR is deliberately absorbing a near-term headwind by exiting cutting and welding. Management expects a 2026 revenue impact of about $25 million to $30 million, with only modest contribution in the first half of 2026 and near-zero in the second half. The strategic logic is straightforward: the business was shrinking, and the company is prioritizing areas aligned with defense and advanced laser platforms. Still, removing revenues that carried a positive margin can pressure near-term comparisons. That pressure can show up in headline margin optics before the benefits of a cleaner portfolio and scaled defense production become more visible in the income statement.

Microfabrication is another swing factor in 2026. Management has described limited visibility, reduced China contribution and variable ordering patterns, with the potential for flat-to-down performance versus 2025. If microfabrication softens while the industrial wind-down accelerates, LASR’s growth burden leans more heavily on aerospace and defense. That raises the bar for defense execution to keep total company growth on track.

The competitive backdrop also remains active. Peers like IPG Photonics IPGP and Coherent COHR operate in overlapping laser markets, underscoring why consistency in end-market demand and program timing matters for LASR’s quarterly narrative. nLIGHT is also facing stiff competition in the optical components and laser end-market from the likes of Lumentum Holdings LITE.

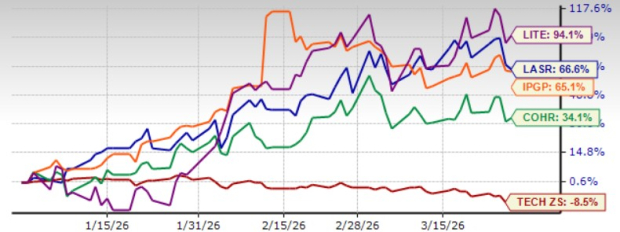

nLIGHT shares have jumped 66.5% on a year-to-date (YTD) basis, outperforming the broader Zacks Computer & Technology sector’s decline of 8.6%. LASR shares have outperformed peers, including IPG Photonics and Coherent, shares of which have returned 65.1% and 34.1%, respectively, over the same time frame. nLIGHT shares have underperformed Lumentum, shares of which have jumped 94.1% YTD.

LASR Stock’s Price Performance

Image Source: Zacks Investment Research

LASR shares are also overvalued, as suggested by a Value Score of F. In contrast, each of Lumentum and IPG Photonics have a Value Score of F while Coherent has D, suggesting stretched valuations. In terms of forward price/sales, nLIGHT trades at a multiple of 12.29 higher than the broader Zacks Computer and Technology sector’s 5.67.

LASR Stock’s Valuation

Image Source: Zacks Investment Research

LASR’s Margin Sensitivity is the Real Earnings Debate

Margins are the main debate because they are sensitive to mix and utilization. In the fourth quarter of 2025, product gross margin stepped down sequentially to 37.3% as mix became less favorable, factory utilization declined and inventory charges increased due to the cutting and welding exit.

The near-term guideposts reinforce that sensitivity. For the first quarter of 2026, management guided to mid-to-high-20% overall gross margin and positive adjusted EBITDA, reflecting how consolidated results can shift with production volumes and fixed-cost absorption.

Development revenue adds another layer of volatility. As milestones reset, development margin can move sharply, and a heavier weighting to development work can dilute consolidated profitability if product ramps do not land on schedule.

Zacks Rank

nLIGHT currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Coherent Corp. (COHR): Free Stock Analysis Report

IPG Photonics Corporation (IPGP): Free Stock Analysis Report

Lumentum Holdings Inc. (LITE): Free Stock Analysis Report

nLight (LASR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios