Labrador Iron Ore Royalty's Strategic Dividend Growth and Exposure to a Resilient Iron Ore Market

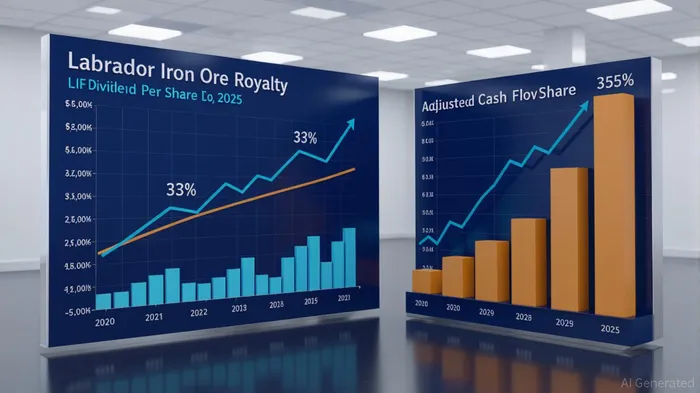

Labrador Iron Ore Royalty Corporation (LIFZF/LIF) has long positioned itself as a compelling income investment, leveraging its unique royalty structure tied to iron ore production in Labrador, Canada. For income-focused investors, the company's recent 33% dividend hike to CAD 0.40 per share[5] and its 10-year compound annual growth rate (CAGR) of 8.91%[4] suggest a resilient payout strategy. However, the investment case hinges on two critical factors: the consistency of its cash flow generation and the structural health of the iron ore market.

Dividend Growth: A Mixed but Strategic Trajectory

LIF's dividend history reflects both ambition and caution. While the company's 5-year dividend growth rate is reported at 14.80%[4] or 17.61%[5] depending on the source, its recent performance underscores a strategic pivot. The 2025 dividend increase, the largest in recent memory, signals confidence in its ability to sustain payouts despite a 64% year-over-year drop in adjusted cash flow per share in Q2 2025[1]. This resilience is partly attributable to its royalty structure, which ties revenue to the production volumes and pricing of iron ore pellets from the Iron Ore Company of Canada (IOC).

However, the absence of an IOC dividend in Q2 2025—a stark contrast to the CAD 41.5 million received in the same period in 2024[1]—highlights the volatility inherent in LIF's business model. Investors must weigh the company's ability to offset such shortfalls through higher concentrate for sale (CFS) volumes against the risk of prolonged iron ore price declines.

Iron Ore Market: Resilience Amid Structural Headwinds

The iron ore market in 2025 presents a paradox: short-term stability coexists with long-term uncertainty. Prices have held above USD 100 per ton, supported by China's “anti-cut-throat competition” policies and infrastructure-driven steel demand[2]. Goldman SachsGS-- forecasts prices to average USD 95 per ton in Q4 2025 before normalizing to USD 80 by 2026[1]. This near-term stability benefits LIFLIF--, as its royalty revenue is directly linked to pellet premiums and ore prices.

Yet structural challenges loom. Chinese steel production, a key driver of demand, is projected to fall below 900 million tonnes by 2035[3], while new supply from Guinea's Simandou project—expected to add 100–120 million tonnes of high-grade ore annually by 2029—threatens to oversaturate the market[1]. These dynamics could pressure LIF's margins, particularly as lower-grade ore and quality issues in Australia's Pilbara region complicate supply-side adjustments[4].

Cash Flow Volatility: A Double-Edged Sword

LIF's cash flow has exhibited sharp quarterly swings. Adjusted cash flow per share fell 37% in Q1 2025 compared to Q4 2024[2], only to rebound 30% in Q2 2025[1]. This volatility reflects the interplay of iron ore prices, pellet premiums, and CFS sales volumes. While the company's debt-free balance sheet provides a buffer[5], the sustainability of its 10.79% dividend yield[1] remains contingent on its ability to navigate these fluctuations.

The decarbonization of the steel industry offers a potential tailwind. High-grade iron ore, which commands premiums in the 65% Fe-grade segment[3], aligns with LIF's asset base. However, this advantage may be offset by the Simandou project's entry into the market, which could dilute the value of high-grade ore over time.

Conclusion: A High-Yield Bet with Commodity Risks

Labrador Iron Ore Royalty's 33% dividend increase and 10.79% yield[1] make it an attractive option for income seekers, particularly in a low-yield environment. Yet the investment case is inextricably tied to the iron ore market's ability to balance near-term demand resilience with long-term supply pressures. Investors must monitor China's steel output, global trade tensions, and the Simandou project's progress to gauge LIF's future cash flow potential.

For those willing to accept commodity volatility, LIF offers a compelling blend of yield and exposure to a critical industrial commodity. However, the absence of a clear path to dividend growth in 2025[4] and the projected decline in iron ore prices to USD 80/ton by 2029[3] suggest prudence in evaluating its long-term sustainability.

Comentarios

Aún no hay comentarios