US Labor Market Softening Signals Shift to Defensive Plays Amid Policy Crosscurrents

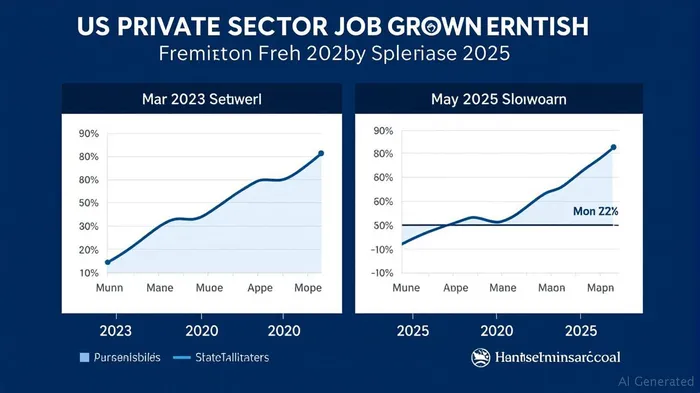

The US labor market's momentum has hit a wall. ADP's May 2025 report revealed a mere 37,000 private sector jobs added—the weakest pace since March 2023—marking a sharp slowdown from April's revised 60,000. This deceleration, which undershot expectations by over 75%, signals a critical inflection point for investors. With hiring intentions weakening amid tariff-driven cost pressures and policy uncertainty, portfolios must pivot toward sectors insulated from labor market headwinds. The data underscores a need to rotate capital into defensive industries while avoiding overexposure to labor-intensive sectors.

Sector Divergences: Winners and Losers in a Cooling Labor Market

The May ADPADP-- report reveals stark sector bifurcation. Leisure/hospitality added 38,000 jobs, benefiting from seasonal demand and post-pandemic recovery tailwinds. Meanwhile, professional/business services lost 17,000 jobs, a red flag for industries reliant on discretionary corporate spending. Education/health services also declined by 13,000 roles, suggesting caution in sectors tied to consumer and government budgets.

The goods-producing sectors shed 2,000 jobs, with manufacturing and mining bearing the brunt of tariff-induced cost pressures. By contrast, construction added 6,000 jobs, hinting at regional demand in housing markets. These divergences highlight the labor market's uneven recovery—and the risks of overexposure to industries facing structural or cyclical headwinds.

Regional and Firm Size Dynamics: Smaller Firms Struggle, Medium-Sized Ones Thrive

Regional performance further complicates the picture. The Northeast and South lost jobs (-19,000 and -5,000, respectively), while the West added 37,000, driven by Mountain states. This geographic split suggests localized economic disparities, with policy impacts (e.g., trade wars) disproportionately affecting manufacturing-heavy regions.

Firm size data offers another layer of insight. Small establishments (1–49 employees) lost 13,000 jobs, reflecting their vulnerability to cost pressures. Medium-sized firms (50–499 employees), however, added 49,000 jobs, indicating resilience in mid-tier companies. This bifurcation points to opportunities in mid-cap equities, while smaller businesses may struggle to maintain margins in a tightening labor market.

Tariff Pressures and Wage Dynamics: Cost Constraints Drive Caution

The ADP report underscores how tariff-related inflation is reshaping labor markets. Manufacturing and natural resources sectors are shedding jobs due to rising input costs, even as medium firms and sectors like financial services expand. Meanwhile, wage growth remains stable for job-stayers (4.5%) but lags at smaller firms (2.6%), signaling that labor-intensive industries may face margin squeezes if costs outpace revenue growth.

Investment Strategy: Rotate to Defensive Sectors with Pricing Power

The data demands a tactical shift:

1. Embrace defensive sectors: Utilities, consumer staples, and healthcare (excluding education/health services) offer stability. These industries have pricing power to offset cost pressures and are less tied to cyclical labor demand.

2. Favor mid-sized firms: Companies with 50–499 employees, particularly in financial services or tech, appear better positioned to navigate uncertainty.

3. Avoid labor-heavy industries: Overexposure to leisure/hospitality (despite recent gains) or professional services could backfire if demand weakens further.

4. Monitor policy risks: Investors must stay agile as trade disputes and fiscal policies reshape sector dynamics.

Conclusion: Rebalance Now to Navigate the Softening Labor Market

The May ADP data is a wake-up call. With hiring slowing and cost pressures rising, portfolios must prioritize stability over speculation. Rotate capital toward sectors and firms with pricing power, geographic or sectoral insulation from tariffs, and manageable labor costs. The labor market's softening is not a temporary blip—it's a signal to rebalance before the broader economy feels the pinch.

The path forward is clear: defensive positioning and sector rotation are no longer optional—they're essential.

Risk Disclosure: Past performance does not guarantee future results. Investors should conduct their own research or consult a financial advisor before making investment decisions.

Comentarios

Aún no hay comentarios