Labor Market Fragility and Equity Valuations: Navigating Risk Through Sector Rotation

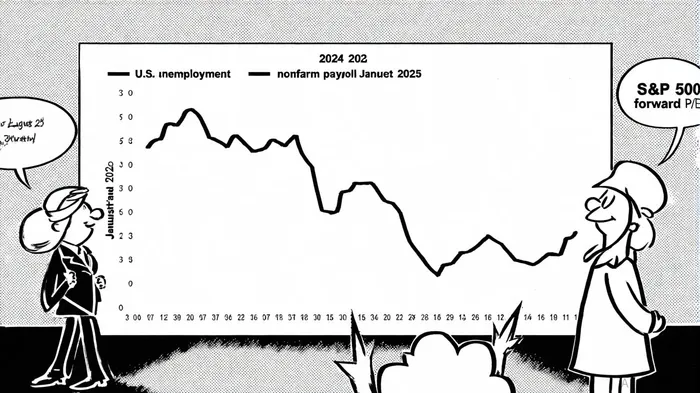

The U.S. labor market has entered a period of fragility, marked by slowing job creation, rising unemployment, and sector-specific imbalances. According to a report by CNBC, nonfarm payrolls rose by just 22,000 in August 2025, far below the forecasted 75,000, while the unemployment rate climbed to 4.3%—a stark contrast to the robust hiring seen earlier in the year [1]. This follows a revised July gain of 79,000 and a net loss of 13,000 in June, underscoring a labor market that is losing momentum. Meanwhile, wage growth, though moderate at 3.7% year-over-year, has failed to meet expectations, signaling a potential moderation in inflationary pressures [1].

These developments have significant implications for equity valuations. The S&P 500's forward 12-month P/E ratio stands at 22.4, a level that reflects stretched valuations and heightened sensitivity to macroeconomic risks [2]. Historically, labor market downturns have led to divergent sector performances. For instance, defensive sectors such as healthcare and consumer staples have demonstrated resilience during economic contractions, while cyclical sectors like industrials and consumer discretionary have faced sharper declines [3]. As the labor market weakens, investors must recalibrate their strategies to mitigate risk and capitalize on sector rotation opportunities.

Sector Rotation: Defensive Plays in a Fragile Labor Market

Defensive sectors are poised to outperform in the current environment. Healthcare, for example, added 31,000 jobs in August 2025, reflecting its enduring demand even as other industries struggle [1]. This sector's resilience is mirrored in equity markets: during the 2008 financial crisis and the 2020 pandemic-induced recession, healthcare stocks averaged positive returns, outperforming the broader market in six of seven recessions since 1960 [4]. Similarly, consumer staples—driven by inelastic demand for essentials—have historically averaged a 15% return during economic slowdowns [4].

In contrast, cyclical sectors face headwinds. Manufacturing and wholesale trade lost 12,000 jobs each in August 2025, exacerbated by uncertainty over U.S. trade policies and rising tariffs [1]. These industries, along with financials, are particularly vulnerable to a Fed rate cut—a move now priced in at near-certainty by markets [2]. While lower borrowing costs may boost sectors like technology and housing, traditional banks could see compressed net interest margins, compounding their challenges [2].

Diversification and the Role of Valuation Metrics

Equity valuations are stretched, with the S&P 500's CAPE ratio reaching 32.87 in 2025—a level historically associated with overvaluation [5]. This raises concerns about a potential correction, particularly for high-P/E sectors like information technology, which trades at 38.09 times earnings [5]. Investors must balance exposure to growth-oriented sectors with defensive holdings to hedge against volatility.

A diversified portfolio could include alternative assets such as gold and commodities, which often exhibit low correlation with equities and act as inflation hedges [4]. Additionally, sectors like utilities, which provide stable cash flows, may offer downside protection. For example, the utilities sector's unrounded unemployed-per-job-opening ratio (UJOR) of 0.97 in April 2025 highlights persistent labor shortages, suggesting continued demand for essential services [6].

Strategic Implications for Investors

The Federal Reserve's anticipated rate cut in September 2025 will likely amplify sector divergences. While lower rates may buoy tech and housing markets, they could also exacerbate inflationary pressures in sectors with already tight labor markets, such as healthcare [2]. Investors should prioritize sectors with strong earnings visibility and low sensitivity to macroeconomic shocks.

Historical data underscores the importance of timing. During the 2008-2009 recession, for instance, financials and industrials fell by over 50%, while consumer staples and healthcare declined by less than 20% [3]. A similar pattern emerged during the 2020 pandemic, where defensive sectors outperformed as cyclical industries faced prolonged downturns [3]. These precedents suggest that a strategic shift toward defensive allocations is prudent in the current climate.

Conclusion

The U.S. labor market's fragility, coupled with stretched equity valuations, demands a disciplined approach to risk management. By rotating into defensive sectors, diversifying with alternative assets, and monitoring macroeconomic signals, investors can navigate the uncertainties ahead. As the Fed's policy response unfolds, sector-specific strategies will be critical to preserving capital and capturing opportunities in a shifting economic landscape.

Comentarios

Aún no hay comentarios