Labor Data Revisions and the Fed's Tightrope: How Shifting Employment Figures Reshape Market Dynamics

The U.S. labor market is undergoing a seismic reassessment, with the Bureau of Labor Statistics (BLS) revising job growth estimates downward by 911,000 for the 12-month period ending in March 2025. This adjustment, the largest in modern economic history, has exposed critical flaws in the BLS's methodology and raised urgent questions about the reliability of data underpinning Federal Reserve policy and investor decisions[2]. As the Department of Labor initiates an internal review and the Office of the Inspector General probes data collection practices, the implications for monetary policy and market dynamics are becoming increasingly clear.

Methodology Under Scrutiny: A Crisis of Confidence

The BLS's preliminary benchmark revisions reveal systemic challenges, including declining survey response rates, overestimation of job creation at new firms, and adjustments for undocumented workers[1]. These issues have eroded trust in the accuracy of labor data, prompting Secretary Lori Chavez-DeRemer to call for reforms[1]. Compounding concerns, the BLS has shifted to secondary data sources for metrics like wireless telephone services and leased vehicles in the Consumer Price Index (CPI), a move aimed at improving transparency but one that introduces new uncertainties[2].

The Office of the Inspector General's investigation into inflation and employment data collection further underscores the fragility of the current system[3]. With the BLS acknowledging resource constraints and methodological gaps, investors must now factor in the possibility of more frequent and larger revisions—a scenario that could destabilize policy expectations and market positioning.

Historical Precedents and Policy Implications

Past labor data revisions have historically influenced Federal Reserve decisions, but the scale of the 2025 adjustment is unprecedented. The downward revision has forced a reassessment of labor market strength, with sectors like professional services, leisure, and retail experiencing outsized declines[4]. This has shifted the Fed's focus from inflationary pressures to a weaker labor market, creating a policy dilemma: support employment or maintain inflation control.

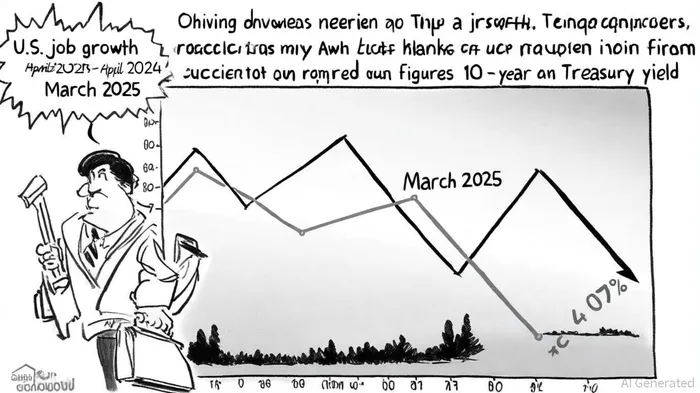

The Fed's September 2025 policy meeting is now a focal point, with markets pricing in a 25-basis point rate cut and some analysts advocating for a larger reduction[4]. The 10-year Treasury yield has already fallen to 4.07%, reflecting expectations of aggressive easing[4]. However, the interplay between revised labor data and persistent inflation—exacerbated by Trump-era tariffs—complicates the Fed's calculus[5]. A weaker labor market could justify rate cuts, but inflation risks remain a tailwind for higher-for-longer rates.

Market Reactions and Portfolio Adjustments

The bond market has already rallied, with Treasury yields declining sharply as investors anticipate Fed action[4]. Gold prices, meanwhile, have surged to record highs, signaling a flight to safety amid economic uncertainty[4]. In equities, sectors poised to benefit from cheaper borrowing costs—such as technology, real estate, and high-leverage companies—are expected to outperform, while cyclical sectors like retail and manufacturing face headwinds[4].

Investors must also consider the long-term implications of the BLS's methodological shifts. The reliance on secondary data sources for CPI and employment metrics introduces volatility into inflation expectations, which could amplify market swings. For example, if future revisions further weaken labor data, the Fed may be compelled to act more aggressively, accelerating rate cuts and boosting risk assets. Conversely, if inflation proves more persistent, bond yields could rebound, punishing long-duration portfolios.

Strategic Recommendations for Investors

Given the uncertainty surrounding labor data reliability, investors should adopt a dual strategy:

1. Overweight Sectors Benefiting from Easing Cycles: Position in technology, real estate, and infrastructure stocks, which historically outperform during rate-cutting environments[4].

2. Underweight Cyclical Sectors: Reduce exposure to retail, manufacturing, and other sectors sensitive to weaker labor demand[4].

3. Hedge Against Volatility: Allocate to safe-haven assets like gold and long-duration Treasuries, which have gained traction as investors seek protection against policy missteps[4].

4. Monitor Data Revisions Closely: The next round of BLS revisions, expected in late 2025, could further reshape market dynamics. Adjust portfolios dynamically based on the magnitude and direction of these revisions.

Conclusion

The current labor data crisis is not merely a technical issue but a structural challenge with far-reaching implications for monetary policy and market behavior. As the Fed navigates the tension between employment and inflation, investors must remain agile, leveraging insights from the BLS's ongoing review and historical precedents. By adjusting portfolios to account for the new normal of volatile data revisions, investors can position themselves to capitalize on the opportunities—and mitigate the risks—of an uncertain economic landscape.

Comentarios

Aún no hay comentarios