Korean Battery Makers' Strategic Pivot to U.S. Energy Storage: Can ESS Demand Offset EV Woes?

The global energy transition is reshaping the fortunes of South Korean battery manufacturers, as they confront a stark reality: a sharp decline in electric vehicle (EV) demand has forced a strategic recalibration toward the U.S. energy storage sector (ESS). With EV battery sales faltering and Chinese competitors dominating the global market, Korean firms like LG Energy Solution, SK On, and Samsung SDI are pivoting to lithium iron phosphate (LFP) batteries for ESS—a move that could determine their long-term viability.

The EV Downturn: A Catalyst for Strategic Shift

South Korea's battery giants have faced a perfect storm in the EV sector. Samsung SDI reported its first quarterly operating loss in nearly eight years in Q4 2024, with revenues dropping 28.8% year-over-year to 3.75 trillion won[1]. LG Energy Solution, meanwhile, posted a 225.5 billion won operating loss during the same period, citing weaker European sales and rising operational costs[1]. SK On's factory utilization rates plummeted from 95% in early 2024 to 46%, underscoring the sector's fragility[2].

This downturn is not isolated. Global EV demand has softened, with South Korean firms' market share in the EV battery sector declining from 31.7% in 2021 to 20.1% in 2024, while Chinese rivals like CATL and BYD captured 53.6% of the global market[2]. In response, the South Korean government has allocated a $14.6 billion support package to stabilize the industry[3], while companies are slashing investments and prioritizing next-generation technologies like 46-Pi batteries[1].

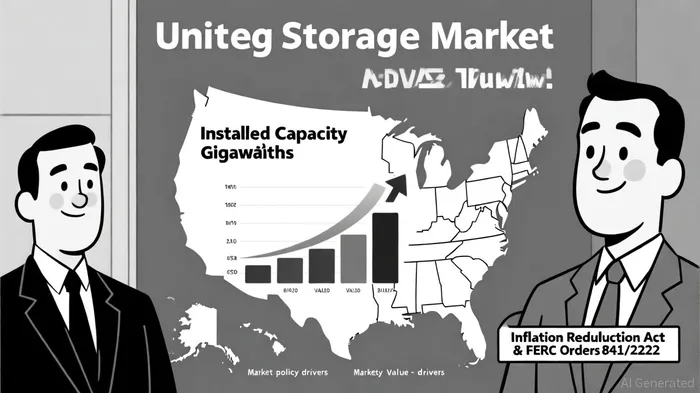

The U.S. ESS Boom: A New Frontier for Korean Firms

Amid these challenges, the U.S. energy storage sector has emerged as a beacon of opportunity. According to a report by Mordor Intelligence, the U.S. ESS market is projected to grow at a 21.62% compound annual growth rate (CAGR) from 2025 to 2030, expanding from 49.52 gigawatts (GW) to 131.75 GW[4]. Simultaneously, the market's value is expected to surge from $106.7 billion in 2024 to $1.49 trillion by 2034, driven by renewable integration, federal incentives, and technological advancements[5].

Korean companies are capitalizing on this momentum. LG Energy Solution, for instance, has begun mass-producing LFP ESS batteries at its Michigan plant and secured a $4.3 billion long-term order for LFP batteries under the Inflation Reduction Act (IRA)[6]. The company's localized production strategy, supported by IRA tax credits, has positioned it to outcompete Chinese firms facing U.S. tariffs on ESS imports[7]. SK On, too, is securing supply chain partnerships, including a memorandum of understanding with L&F to source cathode materials for LFP batteries in North America[6]. Samsung SDI, meanwhile, is evaluating U.S. ESS production lines to avoid tariffs and maintain price competitiveness[6].

Policy Tailwinds and Market Dynamics

The U.S. policy landscape is a critical enabler for Korean firms. The extended Investment Tax Credit (ITC) reduces the cost of residential and commercial storage systems, while FERC Orders 841 and 2222 have expanded market access for storage resources in wholesale electricity markets[4]. Regional initiatives like California's Rule 21 and NEM 3.0 are further accelerating behind-the-meter deployments[4].

These policies have created a favorable environment for Korean companies. As of Q1 2025, their market share in North America has surged to 54%, up from 26.7% in 2021[6]. This growth is not merely a short-term rebound but a structural shift: U.S. ESS demand is expected to expand from 19 GW in 2023 to 250 GW by 2035[6], a trajectory that dwarfs the current scale of the EV battery market.

Challenges and Long-Term Outlook

Despite these positives, challenges persist. Interconnection delays and safety concerns around PFAS in lithium-ion electrolytes could slow near-term growth[4]. However, Korean firms' focus on LFP—a technology with lower safety risks and longer lifespans—positions them to navigate these hurdles. Additionally, their ability to scale production in the U.S. and leverage IRA incentives ensures a competitive edge over Chinese rivals.

For investors, the key question is whether ESS demand can fully offset the EV sector's decline. While the U.S. ESS market's projected value of $1.49 trillion by 2034[5] suggests significant revenue potential, Korean firms must continue innovating and securing long-term contracts to sustain profitability. Their strategic pivot to ESS, however, appears well-aligned with the energy transition's trajectory.

Conclusion

South Korean battery manufacturers are at a crossroads. The EV sector's slump has exposed vulnerabilities, but the U.S. ESS market offers a compelling path forward. By leveraging policy tailwinds, localizing production, and capitalizing on their expertise in LFP technology, companies like LG Energy Solution, SK On, and Samsung SDI are not only mitigating their EV-related losses but also positioning themselves as leaders in the global energy transition. For investors, this strategic realignment represents a high-conviction opportunity in a sector poised for decades of growth.

Comentarios

Aún no hay comentarios