Kohl's Stock Momentum and Strategic Turnaround: Is Citigroup's Upgrade a Sustainable Inflection Point for Retail?

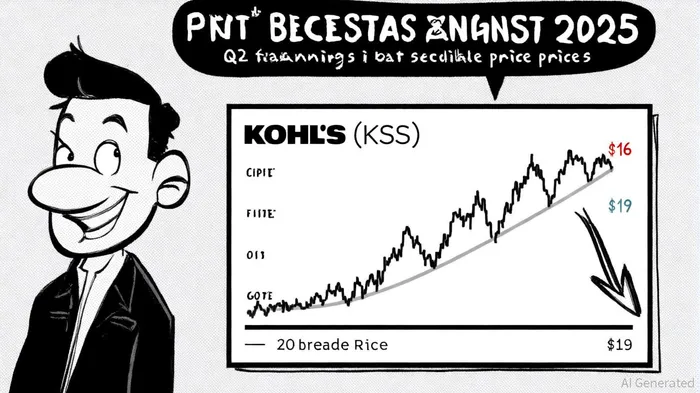

The recent CitigroupC-- upgrade of Kohl'sKSS-- (KSS) stock—from a $16.00 to $19.00 price target while maintaining a “Neutral” rating—has sparked debate about whether this signals a sustainable inflection pointIPCX-- for the retail sector. To assess this, we must dissect Kohl's strategic turnaround, its alignment with broader retail trends, and the sustainability of its operational improvements.

Citigroup's Upgrade: A Cautious Optimism

Citigroup analyst Paul Lejuez's revised price target reflects a 18.75% increase, building on an earlier 100% jump from $8.00 to $16.00 in August 2025[1]. This optimism stems from Kohl's Q2 2025 results, where adjusted earnings per share (EPS) of $0.56 exceeded expectations despite a 4.2% decline in comparable sales[2]. Lejuez highlighted cost discipline—$150 million in annual savings from warehouse consolidations—and inventory optimization, which reduced stock by 5% to $3.0 billion[3]. However, the “Neutral” rating underscores lingering risks, including weak sales trends and a competitive retail landscape.

Historically, KSS's stock has shown mixed outcomes following earnings beats. A backtest of eight such events from 2022 to 2025 reveals a median 5-day excess return of +2.6%, but this advantage faded by the second week and turned slightly negative by day-30[4]. While the initial positive reaction aligns with the recent Q2 beat, the lack of sustained momentum suggests investors should temper expectations.

Strategic Initiatives: Digital, Sustainability, and Partnerships

Kohl's 2025 strategy hinges on three pillars: digital transformation, sustainability, and strategic partnerships. E-commerce now accounts for 40% of total sales, up from 24% in 2020[4], driven by a revamped mobile app, AI-powered inventory management, and curbside pickup. The Sephora in-store beauty partnership, for instance, has boosted beauty sales by low double digits, while Kohl's private labels (Sonoma, Apt. 9) are integrating sustainable materials[5]. These moves align with broader retail trends, where AI-driven personalization and circular economy models are becoming table stakes[6].

Yet challenges persist. Kohl's three-year revenue decline and a 5.1% year-over-year sales drop in Q2 2025[7] suggest that even with cost-cutting, the company must prove its ability to reverse long-term sales erosion. Competitors like KrogerKR-- and AmazonAMZN-- have leveraged similar strategies—Kroger's 3.4% identical sales growth and Amazon's 13.3% revenue increase in Q2 2025[8]—to outperform in a sector where margin pressures and consumer spending shifts are acute.

Broader Retail Trends: AI, Sustainability, and Consumer Shifts

The retail sector in 2025 is defined by two megatrends: AI-driven personalization and sustainability as a core business model. Kohl's adoption of agentic AI for inventory optimization and hyper-personalized marketing mirrors industry-wide shifts[9]. However, sustainability efforts—such as Kohl's 50% emissions reduction target by 2025 and 85% waste diversion goal[10]—are increasingly expected rather than exceptional. Retailers like Zara and Levi's are embedding circularity into their operations, raising the bar for differentiation[11].

Critically, Kohl's 9.31 P/E ratio and 1.31% net margin[12] suggest it remains undervalued relative to peers, but these metrics must improve alongside revenue growth to justify a higher price target. The average analyst price target of $12.75 with a “Reduce” consensus[1] indicates skepticism about Kohl's ability to sustain its recent momentum.

Sustainability of the Upgrade: A Mixed Outlook

Citigroup's upgrade is cautiously optimistic, balancing Kohl's operational improvements with sector-wide headwinds. While the company's cost discipline and digital initiatives are commendable, the retail sector's competitive intensity—exemplified by Amazon's dominance and Kroger's resilience—poses a significant challenge[13]. Additionally, Kohl's reliance on high-margin categories like beauty and personal care may not offset declining sales in core apparel segments[14].

The sustainability of the upgrade hinges on two factors: (1) Kohl's ability to scale its digital and omnichannel strategies to drive consistent sales growth, and (2) the broader retail sector's capacity to absorb AI and sustainability investments without margin compression. If Kohl's can replicate the success of its Sephora partnership in other categories and maintain its cost discipline, the $19.00 price target may prove achievable. However, the “Neutral” rating reflects a realistic acknowledgment that the retail sector's structural challenges—shifting consumer preferences, regulatory pressures, and supply chain volatility—remain unresolved[15].

Conclusion

Citigroup's upgrade of Kohl's stock signals cautious optimism but stops short of a bullish endorsement. While Kohl's strategic initiatives align with critical retail trends, the sustainability of its turnaround depends on its ability to execute against ambitious digital and sustainability goals while reversing long-term sales declines. For investors, the $19.00 price target represents a moderate upside, but the broader sector's volatility and Kohl's operational risks suggest a “watch and wait” approach may be prudent.

Comentarios

Aún no hay comentarios