KNOREX's NYSE American Listing and 24% Revenue Growth in 2024: A Strategic Buy Signal for Resilient Consumer Tech Exposure

The recent NYSE American listing of Knorex Ltd.KNRX-- (ticker: KNRX) has injected fresh momentum into the AI-driven advertising sector, offering investors a compelling case for resilient consumer tech exposure. With a 24% revenue increase in 2024 and a $12 million IPO completed on September 29, 2025, the company is poised to capitalize on the post-pandemic surge in demand for automated, data-centric marketing solutions. This analysis explores how Knorex's strategic positioning, technological innovation, and alignment with macroeconomic trends make it a standout candidate for long-term growth.

Leveraging IPO Momentum in a High-Growth Sector

Knorex's IPO, led by R. F. Lafferty & Co. Inc., raised $12 million by issuing 3 million Class A ordinary shares at $4.00 apiece, with an additional 450,000 shares reserved for over-allotment, according to a QuiverQuant announcement. While the stock initially traded at $2.81-a 9% decline from its IPO price-the volatility is characteristic of newly public tech firms in nascent markets. The proceeds will fund geographic expansion in North America and Asia, as well as R&D to enhance its AI/ML-driven platform, KnorexKNRX-- XPOsm. This platform, which streamlines cross-channel ad campaigns and reduces wasted spend, addresses a critical pain point in digital advertising: inefficiency in fragmented, multi-platform campaign management, as noted in a Knorex IPO post.

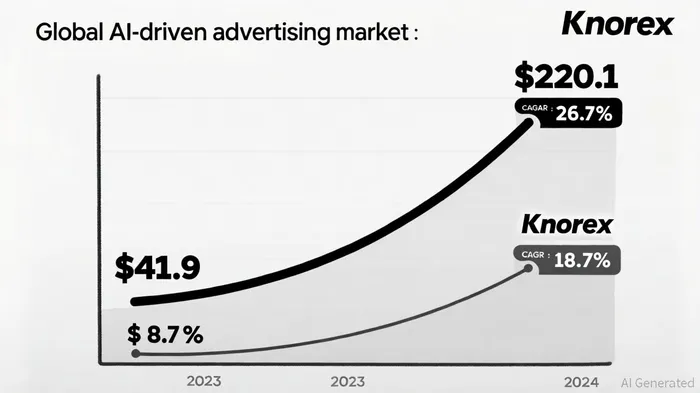

The IPO's timing is fortuitous, coinciding with a broader industry shift toward AI-powered automation. According to a Global Market Insights report, the AI-driven advertising market is valued at $41.9 billion in 2023 and is projected to grow at a 26.7% CAGR, reaching $220.1 billion by 2030. Knorex's 24% revenue growth in 2024-up from $8.7 million in 2023-positions it as a rare high-performing player in a sector still dominated by legacy models (the IPO filing and company disclosures provide the revenue and IPO details).

Strategic Buy Signal: Scalable Market Positioning

Knorex's value proposition lies in its ability to unify disparate advertising channels under a single AI-powered interface. Its XPOsm platform leverages predictive analytics and real-time optimization to deliver personalized content at scale, a capability that aligns with the post-pandemic demand for hyper-targeted consumer engagement, as highlighted in an Investing.com article. For instance, the platform's machine learning algorithms can adjust campaign parameters dynamically, improving conversion rates while minimizing manual intervention-a critical advantage in an industry where ad spend waste remains a persistent issue (the company has emphasized these operational benefits in investor communications).

The company's global footprint further strengthens its scalability. With operations in the U.S., Vietnam, India, Malaysia, and Singapore, Knorex is uniquely positioned to tap into both mature and emerging markets. This diversification mitigates regional economic risks while enabling the firm to adapt its solutions to local consumer behaviors (market analyses and Knorex disclosures describe this geographic mix). Moreover, the global digital advertising market is forecasted to reach $871 billion by 2027, creating ample room for Knorex to capture market share as it expands.

Post-Pandemic Innovation Cycle: A Tailwind for AI-Driven Solutions

The post-pandemic era has accelerated the adoption of AI in marketing, driven by three key factors: the explosion of consumer data, the need for cost efficiency, and the rise of omnichannel strategies. Knorex's focus on programmatic advertising-automating ad buying and placement-addresses all three. By integrating AI into campaign execution, the company enables clients to reduce costs, improve targeting, and generate actionable insights from vast datasets, a theme that Knorex has emphasized in its market commentary.

This innovation cycle is not just theoretical. Real-world applications of AI in advertising, such as predictive budgeting and automated A/B testing, are already yielding measurable results. For example, Knorex reported a 40% increase in gross profit to $4.5 million in 2024, despite a net loss of $5.88 million, underscoring the platform's potential to drive profitability as scale increases (company financial statements report these figures). The CEO, Justin Choo, has emphasized that the IPO provides "vital capital and market visibility" to accelerate global expansion, a sentiment echoed by industry analysts who view AI-driven platforms as the future of digital marketing.

Risks and Mitigants

While Knorex's trajectory is promising, investors must remain cognizant of risks. The stock's post-IPO volatility and the company's current negative EBITDA (-$5.49 million in the last twelve months) highlight the challenges of scaling a tech-driven business in a competitive sector (the IPO filing and recent financials disclose these metrics). Additionally, the AI advertising market is still fragmented, with numerous startups vying for dominance. However, Knorex's first-mover advantage in cross-channel unification and its strategic use of IPO proceeds to enhance AI capabilities provide a durable moat, according to market observers.

Conclusion: A Strategic Bet on the Future of Advertising

Knorex's NYSE American listing represents more than a fundraising milestone-it is a strategic inflection point in the evolution of AI-driven advertising. By combining IPO momentum with scalable market positioning, the company is well-placed to benefit from the post-pandemic innovation cycle. For investors seeking resilient exposure to consumer technology, KNRX offers a compelling case: a high-growth sector, a differentiated product, and a clear path to capitalizing on the $220 billion AI advertising opportunity by 2030.

Comentarios

Aún no hay comentarios