Klarna's Oversubscribed US IPO: A Fintech Powerhouse Entering the Public Market

The much-anticipated US initial public offering (IPO) of KlarnaKLAR--, the Swedish buy now, pay later (BNPL) giant, has ignited significant investor enthusiasm. Priced at $40 per share—above its marketed range of $35 to $37—the offering values the company at approximately $15.1 billion, a stark contrast to its $45 billion peak in 2021 but a recovery from its 2022 valuation of $6.7 billion [1]. With 34.3 million shares sold, the IPO raised $1.37 billion, oversubscribed by 25 to 26 times, signaling robust demand in a cautiously optimistic fintech market [2]. Yet, as the company prepares to trade on the New York Stock Exchange under the ticker “KLAR,” the question remains: Does this valuation reflect sustainable growth, or is it driven by speculative fervor in the BNPL sector?

Valuation in Context: Sector Growth vs. Profitability Challenges

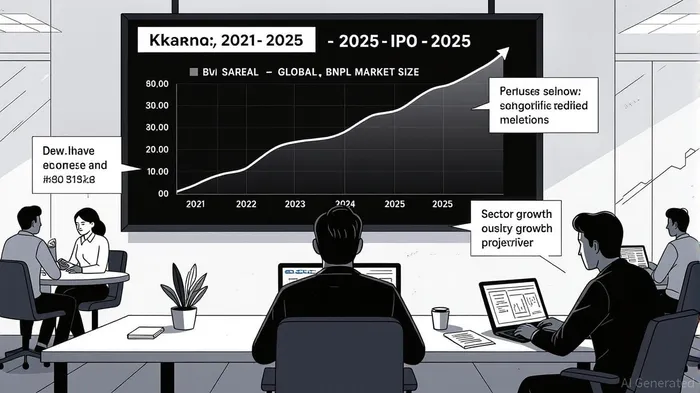

The BNPL sector is undeniably on a growth trajectory. According to a report by Bloomberg, the global BNPL market is projected to reach $560.1 billion in 2025, expanding at a 13.7% annual rate, and is expected to grow further to $911.8 billion by 2030 [3]. Klarna, with 111 million active consumers and 790,000 merchant integrations, is a key player in this expansion. However, its valuation of $15.1 billion—while a recovery from its 2022 trough—still lags behind its 2021 peak. This discrepancy underscores the sector's maturation and the market's recalibration of expectations.

Klarna's financials tell a mixed story. For Q2 2025, the company reported $823 million in revenue, a 20% year-over-year increase, but also a net loss of $53 million, up from $18 million in Q2 2024 [4]. While the company has achieved five consecutive profitable quarters as of Q2 2025, its recent loss highlights the challenges of balancing growth with profitability in a competitive landscape. By comparison, AffirmAFRM--, a major BNPL rival, trades at a market cap of $28 billion and a revenue multiple of 8.9x, significantly higher than Klarna's 5x multiple [5]. This gapGAP-- reflects Affirm's faster revenue growth (nearly 40% in 2023) and a business model that derives 50% of its revenue from interest income, compared to Klarna's 24% [5].

Strategic Positioning and Competitive Dynamics

Klarna's valuation must also be assessed against its strategic initiatives. The company is transitioning from a pure BNPL platform to a broader digital banking and shopping assistant, with products like the Klarna Card and partnerships with WalmartWMT-- and JPMorgan ChaseJPM-- [6]. These moves aim to diversify revenue streams beyond transaction fees, which currently account for the majority of its income. However, its reliance on merchant fees—tied to gross merchandise volume (GMV)—makes it more vulnerable to macroeconomic shifts, such as rising interest rates and regulatory scrutiny.

The BNPL sector faces intensifying regulatory pressure, particularly in the EU and Australia, where new laws mandate transparency and responsible lending practices [7]. Klarna's Swedish banking license adds another layer of complexity, as it must navigate both European and US regulatory frameworks. Meanwhile, competitors like Affirm and PayPalPYPL-- are leveraging AI-driven credit assessments and personalized payment plans to enhance risk management, further intensifying competition [8].

Investor Sentiment and Market Signals

Despite these challenges, Klarna's IPO has attracted strong investor demand. The offering's oversubscription and pricing above the marketed range suggest confidence in its market leadership and long-term potential. This optimism is partly fueled by the broader revival of the US IPO market, with listings like FigmaFIG-- and CircleCRCL-- signaling cautious optimism for high-growth fintechs [9]. However, past fintech IPOs, such as KlaviyoKVYO-- and Instacart, serve as cautionary tales when valuations outpace public market expectations [10].

Analysts view Klarna's IPO as a bellwether for the sector. A successful debut could validate the BNPL model's sustainability, encouraging other fintechs to pursue public listings. Conversely, a weak performance might highlight the risks of prioritizing growth over profitability. The company's recent partnership with Walmart and its expansion into digital banking are critical factors that could differentiate it from peers, but its ability to maintain profitability in a high-interest-rate environment remains a key uncertainty.

Conclusion: Sustainable Growth or Speculative Hype?

Klarna's $15.1 billion valuation reflects a blend of sector optimism and strategic momentum. The BNPL market's projected growth, coupled with Klarna's expanding merchant network and digital banking ambitions, provides a strong foundation for long-term value creation. However, the valuation discount compared to peers like Affirm—and the company's recent net loss—highlight the risks of macroeconomic volatility, regulatory hurdles, and competitive pressures.

For investors, the IPO represents an opportunity to bet on Klarna's ability to navigate these challenges while capitalizing on the BNPL sector's expansion. Yet, the valuation's sustainability will ultimately depend on the company's execution of its strategic vision, its path to consistent profitability, and its ability to adapt to a rapidly evolving regulatory and economic landscape.

Comentarios

Aún no hay comentarios