Klarna's IPO and Strategic Share Sales by Key Investors: Assessing Commonwealth Bank of Australia's Position and Profit Potential

The Commonwealth Bank of Australia (CBA) has long been a strategic investor in KlarnaKLAR--, the Swedish buy-now-pay-later (BNPL) giant. Its 2020 investment of $300 million secured a 5.5% stake in Klarna and half-ownership of its operations in Australia and New Zealand[1]. Now, as Klarna prepares for its U.S. IPO—priced at $40 per share, valuing the company at $15.1 billion[2]—CBA faces a pivotal decision: to sell down its stake for immediate capital gains or retain ownership to capitalize on Klarna's long-term growth. This move, if executed, could yield up to $1.8 billion for CBA, based on a $20 billion valuation[3].

CBA's Strategic Dilemma: Risk Mitigation or Long-Term Confidence?

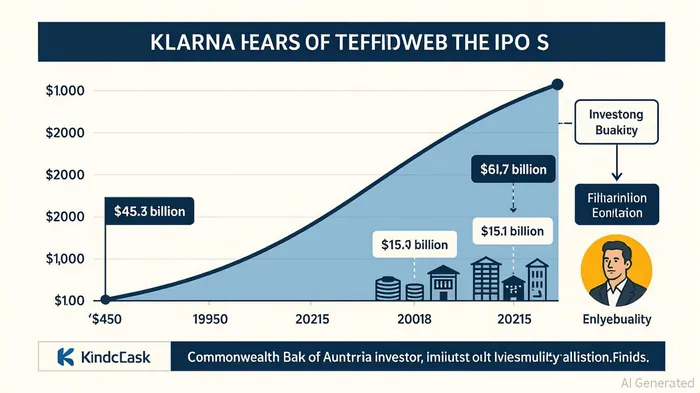

CBA's potential partial sale of its Klarna stake reflects a nuanced balance between risk management and strategic foresight. By 2025, CBA's stake in Klarna was valued at $956 million, a significant increase from $574 million in 2024[4]. Selling a portion of this stake would allow the bank to lock in gains amid a volatile market environment. For instance, Klarna's valuation has fluctuated wildly—from a 2021 peak of $45.6 billion to a 2022 trough of $6.7 billion[5]—highlighting the risks of holding a high-growth fintech investment in a cyclical economy.

However, CBA's decision also signals confidence in Klarna's ability to evolve beyond its BNPL roots. The company has positioned itself as a digital banking platform, offering savings, budgeting, and investment tools[6]. This pivot could insulate Klarna from regulatory scrutiny targeting BNPL services and diversify its revenue streams. CBA's 50% ownership of Klarna's ANZ operations further underscores its commitment to the company's regional success, suggesting that any sell-down would likely be partial rather than a full exit[1].

Klarna's IPO: A Bellwether for Fintech Valuations

Klarna's IPO, which raised $1.37 billion[2], has become a litmus test for investor sentiment toward fintechs. The $15.1 billion valuation, while a fraction of its 2021 peak, represents a recovery from its 2022 low and reflects cautious optimism. Analysts note that Klarna's brand strength—serving 111 million active consumers and 790,000 merchants—gives it a competitive edge over rivals like AffirmAFRM--, which trades at a 7.2x next-twelve-months (NTM) sales multiple compared to Klarna's 3.9x[7]. Yet, profitability remains a concern: Klarna reported a $52 million net loss in Q2 2025 despite $823 million in revenue[2].

The IPO's success hinges on Klarna's ability to demonstrate scalable profitability and navigate macroeconomic headwinds. Rising credit costs and regulatory pressures, particularly in the U.S., pose significant challenges[8]. For CBA, the IPO offers an opportunity to reassess its exposure to a sector where valuations have normalized. If Klarna's stock underperforms, CBA could mitigate losses by reducing its stake. Conversely, a strong post-IPO performance might encourage the bank to retain its position, betting on Klarna's long-term potential as a digital banking platform.

Broader Implications for Fintechs

Klarna's IPO underscores a broader shift in fintech valuations. The sector, once characterized by speculative growth-at-all-costs models, is now underpinned by disciplined unit economics and profitability metrics[9]. Investors are demanding proof of sustainable margins, a trend evident in Klarna's conservative valuation compared to its 2021 peak. For CBA, this environment presents both opportunities and risks. A partial exit could free up capital for other investments or shareholder returns, while retaining a stake aligns with its long-term vision of supporting innovation in financial services.

Moreover, Klarna's IPO could catalyze a resurgence in fintech listings. The offering was 15 times oversubscribed[2], indicating robust demand for high-quality fintech assets. If Klarna navigates its post-IPO challenges successfully, it may pave the way for other BNPL and digital banking startups to access public markets. For CBA, this could mean leveraging its experience with Klarna to identify and invest in the next wave of fintech disruptors.

Conclusion

CBA's strategic share sale in Klarna's IPO encapsulates the delicate balance between risk mitigation and long-term confidence. By potentially securing $1.8 billion in proceeds, the bank can fortify its balance sheet while retaining a stake in a company poised to evolve into a digital banking powerhouse. Klarna's IPO, meanwhile, serves as a barometer for fintech valuations, signaling a market that prioritizes profitability over pure growth. As the sector matures, CBA's approach to its Klarna investment will likely be studied as a case study in prudent, forward-looking capital management.

Comentarios

Aún no hay comentarios