KinderCare Learning Companies Faces Class-Action Litigation: Assessing Legal Risks and Shareholder Value Implications

The ongoing class-action lawsuit against KinderCare LearningKLC-- Companies, Inc. (NYSE: KLC) has cast a long shadow over the childcare provider's post-IPO trajectory. Filed in the U.S. District Court for the District of Oregon as Gollapalli v. KinderCareKLC-- Learning Companies, Inc., the case alleges that the company's October 2024 initial public offering (IPO) registration statement omitted material risks, including repeated incidents of child abuse, neglect, and harm at its facilities, according to a Scott+Scott report. These allegations, if proven, could expose KinderCare to significant financial and reputational damage, raising critical questions about its long-term viability and shareholder value.

Litigation Risk: A Closer Look

The lawsuit centers on claims that KinderCare's IPO disclosures were misleading, failing to address systemic issues in its operations. According to the complaint, the company's failure to meet basic childcare industry standards and regulatory requirements created a "heightened risk of lawsuits, adverse regulatory action, and reputational harm," a point emphasized by Scott+Scott. This narrative gained traction in early 2025, as independent investigations and media reports highlighted lapses in safety and care quality, reflected in the PACER docket for the case (PACER docket).

Procedurally, the case is in its early stages. On September 9, 2025, the court extended the deadline for defendants to respond to the complaint, pushing the motion for lead plaintiff and lead counsel to October 14, 2025 (per the PACER docket). While no substantive rulings on the merits have been issued, the procedural delays and the involvement of multiple law firms-including Shamis & Gentile, DJS Law Group, and Robbins Geller-underscore the complexity of the litigation. Investors who purchased shares during the IPO are now racing to secure lead plaintiff status, a critical step for those seeking to direct the case's strategy, as noted in a Shamis & Gentile notice.

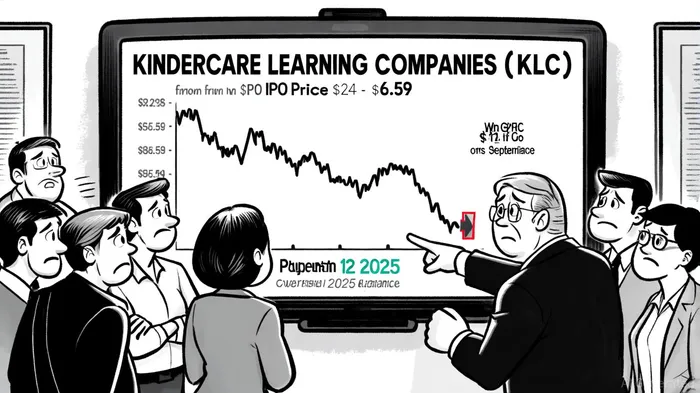

Financial Impact and Shareholder Value

The stock's performance since the IPO underscores the market's skepticism. KinderCare's shares debuted at $24 but plummeted to $9.81 by August 12, 2025, following the company's announcement of revised financial guidance due to "lower-than-expected enrollment and increased compliance costs," an outcome highlighted by Scott+Scott's commentary. By late September 2025, the stock had further declined to around $6.85, reflecting a 67% drop from its IPO price, according to KLC historical prices. This trajectory highlights the immediate financial toll of litigation uncertainty and operational challenges.

The potential costs of the lawsuit are multifaceted. A successful class action could result in a costly settlement or jury award, straining KinderCare's balance sheet. More broadly, the allegations threaten to erode trust among parents, regulators, and investors. For instance, the company's revised guidance already signals a broader struggle to maintain enrollment, which is critical for its revenue model, a point underscored by Scott+Scott. If reputational damage persists, the long-term cost of capital could rise, deterring future investment and limiting growth opportunities.

Long-Term Implications and Investor Considerations

Beyond direct financial risks, the litigation raises existential questions about KinderCare's business model. The childcare industry is highly sensitive to public perception, and allegations of neglect or abuse could trigger regulatory scrutiny or stricter compliance requirements. For example, states may impose new licensing standards or penalties, increasing operational costs (as reflected in the PACER docket). Such developments could further compress profit margins, particularly for a company already grappling with enrollment declines.

Investors must also weigh the likelihood of a favorable resolution. While the case remains in its procedural phase, the sheer volume of media attention and the involvement of multiple law firms suggest a high probability of a protracted legal battle. Scott+Scott has noted that the appointment of a lead plaintiff by October 14 will be a pivotal moment, potentially shaping the case's direction and settlement prospects, and law-firm notices reiterate the importance of that appointment.

Conclusion

KinderCare Learning Companies' class-action litigation represents a textbook example of how corporate governance failures can translate into severe shareholder value destruction. While the company's immediate financial struggles are evident in its stock price, the long-term risks-ranging from regulatory penalties to reputational harm-are equally concerning. For investors, the key takeaway is clear: the litigation is not merely a legal issue but a strategic threat that could redefine the company's trajectory. As the case unfolds, close monitoring of both legal developments and operational performance will be essential for assessing KinderCare's path forward.

Comentarios

Aún no hay comentarios