Keurig Dr Pepper's High-Stakes Coffee Bet: Balancing Long-Term Value Creation with Short-Term Skepticism

Keurig Dr Pepper (KDP) has embarked on a transformative strategic journey with its $18.4 billion acquisition of JDE Peet's, a move designed to position the combined entity as the world's largest pure-play coffee company. While the company's leadership touts this as a bold step toward long-term value creation, the market has responded with skepticism, slashing KDP's stock price by over 18% in early trading and erasing $8 billion in market value[3]. This divergence between strategic ambition and investor sentiment raises critical questions: Can KDP's high-leverage bet on the global coffee market deliver sustainable growth, or is the company overreaching in a bid to replicate past successes?

Strategic Moves for Long-Term Growth

KDP's 2025 strategy is anchored in three pillars: innovation, diversification, and scale. The company reported robust Q1 2025 results, with net sales rising 4.8% to $3.6 billion and operating income up 4.7% to $801 million[1]. These figures underscore KDP's ability to execute disciplined cost management and capitalize on high-growth categories like energy drinks, which now generate over $1 billion in annual sales[3]. However, the acquisition of JDE Peet's represents a quantum leap in ambition. By merging KDP's single-serve coffee dominance with JDE's global portfolio (including brands like StarbucksSBUX-- and Lavazza), the company aims to create a $16 billion annual revenue stream under a new Global Coffee Co. spin-off[4].

The rationale for this move is compelling. Coffee consumption is projected to grow at a 4% CAGR through 2030, driven by premiumization and convenience trends[2]. KDP's CEO, Tim Cofer, has emphasized that the acquisition will unlock $400 million in annual cost synergies and drive EPS accretion, while the separation of the coffee and North American beverage businesses is expected to enhance operational clarity[4].

Market Skepticism and Risks

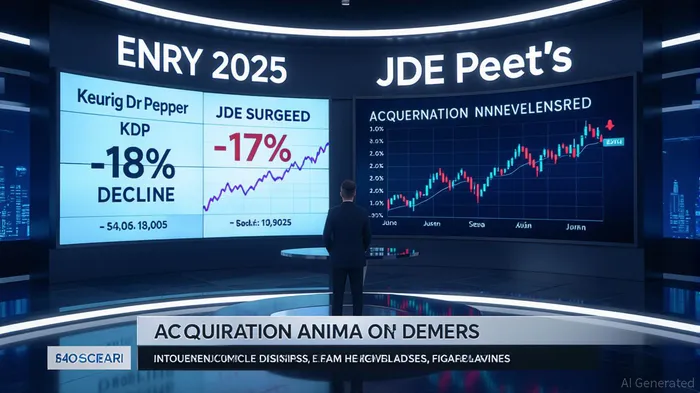

Despite these strategic justifications, investors remain wary. The acquisition's all-cash structure and $18.4 billion price tag have pushed KDP's pro-forma net-debt/EBITDA ratio into the mid-to-high-5x range—a level that raises red flags for leveraged buyout specialists and value investors alike[2]. Analysts at HSBCHSBC-- and UBSUBS-- have downgraded KDPKDP-- to “Hold,” citing concerns about near-term deleveraging and the execution risks inherent in such a large-scale integration[3].

The stock's sharp decline reflects these fears. In early August 2025, KDP shares fell 11.5% on the day of the announcement, with critics arguing that the deal overvalues JDE Peet's and underestimates the challenges of separating two complex businesses[5]. Meanwhile, JDE Peet's shares surged 17% in London, illustrating the market's belief that KDP is paying a premium for a struggling asset[2].

Reconciling the Two Sides

The key to evaluating KDP's strategy lies in reconciling its long-term vision with short-term execution risks. On one hand, the company's free cash flow generation—$1.2 billion in 2024—provides a buffer for debt servicing[1]. On the other, the success of the JDE Peet's acquisition hinges on achieving $400 million in cost synergies within three years and cleanly separating the new entities by 2026[2].

Analysts like RBC Capital offer a more optimistic view, maintaining an “Outperform” rating and a $42 price target, arguing that the coffee spin-off could unlock a 13% upside for KDP's stock over the next 12 months[3]. This optimism is tied to the potential for the Global Coffee Co. to dominate the single-serve segment, a market KDP already controls with 35% U.S. market share[1].

Conclusion

Keurig Dr Pepper's JDE Peet's acquisition is a high-stakes gamble that could redefine its trajectory. While the company's Q1 2025 results and energy drink growth demonstrate operational strength, the market's skepticism is warranted given the leverage and integration risks. For long-term value creation to materialize, KDP must execute flawlessly: delivering synergies, separating the businesses cleanly, and navigating the debt burden without sacrificing innovation. Investors who believe in the company's ability to transform the global coffee landscape may find the current stock price a compelling entry point—but only if they're prepared to weather the near-term turbulence.

Comentarios

Aún no hay comentarios