Kenvue's Stock Resilience Amid Regulatory and Reputational Storms: A Cautionary Investment Analysis

The consumer healthcare sector has long been a magnet for regulatory scrutiny, but few companies exemplify the risks of public health scares better than KenvueKVUE-- Inc. (KVUE). In 2025, the firm faces a perfect storm of reputational and regulatory challenges, centered on its flagship Tylenol brand. According to a report by Investing.com, the Trump administration's anticipated advisory against Tylenol use during pregnancy—linked to autism risk—has already triggered a 6.05% premarket stock plunge on September 22, 2025 [1]. This development underscores the fragility of Kenvue's market position, even as it leverages a portfolio of iconic brands like Listerine and Neutrogena.

Regulatory Risks: A Double-Edged Sword

Kenvue's exposure to regulatory risks is not merely theoretical. The company's Q2 2025 results reveal a 4.0% year-over-year decline in net sales, with organic sales dropping 4.2% due to volume and pricing pressures [2]. While these figures reflect broader market dynamics, the looming Tylenol controversy threatens to exacerbate the trend. Health Secretary Robert F. Kennedy Jr.'s advocacy for a link between acetaminophen and autism has amplified public anxiety, despite Kenvue's insistence that no credible scientific evidence supports such claims [1]. The company's interim CEO, Kirk Perry, reportedly sought exemptions for Tylenol in the administration's report, a move that provided temporary relief but did little to resolve the underlying issue.

The potential fallout from a government advisory is staggering. Legal liabilities, reputational damage, and a shift in consumer behavior could erode Tylenol's dominance in the over-the-counter painkiller market. As noted by Monexa.ai, Kenvue's 2025 outlook now projects low-single-digit sales declines, compounded by foreign currency headwinds and operational inefficiencies [3]. These challenges are further compounded by negative free cash flow margins, raising concerns about dividend sustainability [3].

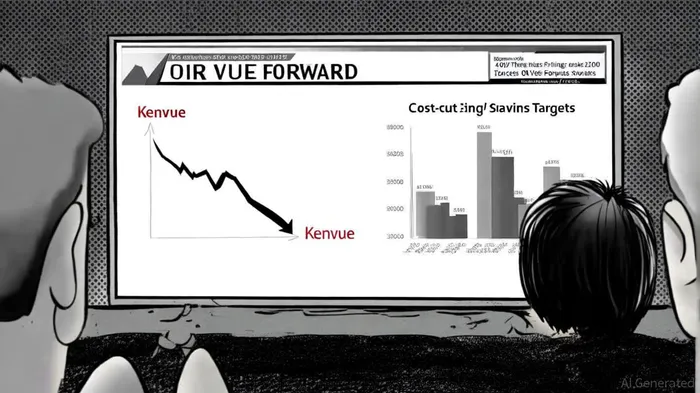

Strategic Responses: Cost-Cutting vs. Innovation

Kenvue's “Our Vue Forward” cost-cutting initiative aims to generate $350 million in annualized savings by 2026, targeting EBITDA margin expansion and reinvestment in innovation [3]. While such measures are prudent, they may not offset the reputational damage from the Tylenol saga. The company's commitment to quality and compliance—highlighted in its corporate policies—remains a defensive asset, but these systems have yet to be tested in a high-stakes regulatory crisis [4].

Activist investor TOMS Capital has escalated pressure, advocating for bold moves like asset separations or a full sale to unlock shareholder value [5]. This reflects a growing skepticism about Kenvue's ability to navigate its current challenges through organic strategies alone. The firm's sluggish growth in competitive U.S. skincare markets further complicates its turnaround prospects [5].

Reputational Risks and Investor Sentiment

The stock's 16-week low valuation reflects investor fears of lawsuits, stricter regulations, and consumer backlash [1]. A single government announcement linking Tylenol to autism could trigger a cascade of legal actions, mirroring past crises in the pharmaceutical industry. For context, Johnson & Johnson's 1982 Tylenol tampering scandal cost the company $100 million in losses but ultimately reinforced its crisis management protocols. Kenvue's response to its current predicament will be critical in determining whether it can replicate such resilience.

Conclusion: A High-Stakes Balancing Act

Kenvue's stock resilience hinges on its ability to mitigate regulatory and reputational risks while executing its cost-cutting and innovation strategies. While the company's quality systems and brand equity provide a foundation, the Tylenol controversy remains a wildcard. Investors must weigh the potential for short-term volatility against the long-term viability of Kenvue's business model. For now, the stock appears overexposed to external shocks, making it a high-risk proposition in a sector where public trust is paramount.

Comentarios

Aún no hay comentarios