KBR, Inc.: Navigating Legal Turmoil and Investment Dilemmas in 2025

The recent legal and operational upheaval at KBRKBR--, Inc. (NYSE: KBR) has thrust the energy and defense contractor into the spotlight, presenting a complex calculus for value-oriented investors. At the heart of the storm lies a securities class action lawsuit initiated by Berger Montague PC, which alleges that KBR misled investors about the viability of its joint venture, HomeSafe Alliance, and its $20 billion military relocation contract with the U.S. Department of Defense's Transportation Command (TRANSCOM). This litigation, coupled with a separate WARN Act lawsuit and operational setbacks, raises critical questions about the company's short-term risks and long-term resilience.

The Legal Quagmire: A Double-Edged Sword

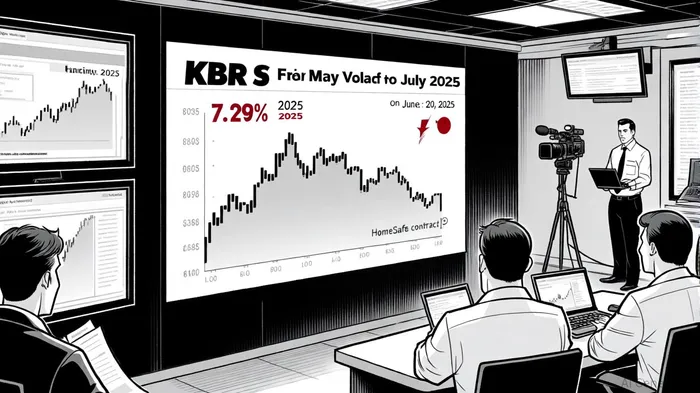

The securities class action, Norrman v. KBR, Inc., targets KBR's alleged failure to disclose material concerns about HomeSafe's ability to fulfill its obligations under the Global Household Goods Contract. According to a report by Hagens Berman, KBR executives assured investors during a May 6, 2025, earnings call that the partnership was “strong” and “excellent,” despite internal knowledge of TRANSCOM's dissatisfaction [1]. When HomeSafe announced the contract's termination for cause on June 19, 2025, KBR's stock plummeted 7.29% in a single day, erasing $1.3 billion in market value [2].

The lawsuit, which seeks to represent shareholders who purchased KBR stock between May 6 and June 19, 2025, has a lead plaintiff deadline of November 18, 2025 [3]. While the outcome remains uncertain, historical precedents suggest that similar securities litigation cases settle for an average of $43 million. However, given the scale of the $20 billion contract and the reputational damage to KBR, legal experts speculate that the settlement could be significantly higher [4].

Compounding the issue is a separate lawsuit alleging violations of the WARN Act, which claims that KBR and HomeSafe laid off over 200 employees without the required 60-day notice [5]. These dual legal fronts—civil and employment-related—add layers of complexity to KBR's risk profile, potentially straining its balance sheet and diverting management's attention from core operations.

Financial Resilience Amid Turbulence

Despite these challenges, KBR's financials reveal a company with structural strengths. For Q2 2025, the firm reported $2.0 billion in revenue, a 6% increase driven by its Defense & Intel segment [6]. Its liquidity position remains robust, with $1.008 billion in available borrowing capacity and a net leverage ratio of 2.4x [7]. However, the termination of the HomeSafe contract has already begun to erode profitability. Q3 results revealed a $48 million net loss from discontinued operations, including $64 million in asset impairments and $30 million in write-offs [8].

Analysts remain divided on KBR's prospects. While Goldman Sachs maintains a “Neutral” rating with a $55.00 price target, Keybanc upgraded to “Overweight” with a $63.00 target, citing long-term demand for defense infrastructure [9]. The average 12-month price target of $62.78 implies a potential 27% upside from current levels, but recent downgrades from Bank of America and UBS reflect growing caution [10].

Risk vs. Reward: A Value Investor's Dilemma

For value-oriented investors, the key question is whether KBR's stock represents a contrarian opportunity or a cautionary tale. On one hand, the company's core business in defense and energy services remains resilient, with the Sustainable Technology Solutions segment posting a 16% quarter-over-quarter increase in operating income [11]. On the other hand, the legal uncertainties and operational missteps—such as the HomeSafe debacle—highlight governance risks that could persist for years.

The litigation timeline will be critical. If KBR can resolve the securities class action quickly and at a manageable cost, it may stabilize investor sentiment. However, a protracted legal battle or a large settlement could exacerbate earnings volatility and delay strategic investments. Additionally, the WARN Act lawsuit, though smaller in scale, could set a precedent for employee-related liabilities in future ventures.

Historical backtesting of KBR's earnings releases from 2022 to 2025 reveals a mixed picture for buy-and-hold strategies. While the stock occasionally outperformed the S&P 500 by up to 2.01% within nine days of an earnings event, this advantage typically decayed by the 30-day mark, with end-of-window drift at just +0.53% [4]. The win rate for positive price movement oscillated between 55–60% initially but fell below 50% by day 30, suggesting that short-term gains are inconsistent and often eroded by market forces. These findings underscore the importance of caution for investors relying on earnings-driven momentum, as the data does not support a reliable edge in directional trading around these events.

Conclusion: Proceed with Caution

KBR's situation embodies the classic tension between value and risk. While its financial fundamentals and industry positioning offer a foundation for recovery, the ongoing litigation and operational setbacks create significant headwinds. For investors with a high risk tolerance and a long-term horizon, the stock's current valuation—trading at a 18.2% discount to estimated fair value—may present an entry point [12]. However, those prioritizing stability should wait for clearer resolution of the legal disputes and a demonstration of improved operational execution.

In the interim, KBR's ability to navigate these challenges will hinge on its transparency, leadership, and capacity to rebuild trust with stakeholders. Until then, the stock remains a high-risk proposition, demanding close scrutiny and strategic patience.

Comentarios

Aún no hay comentarios