Japan's Inflation Slowdown: A Strategic Buying Opportunity in Resilient Sectors?

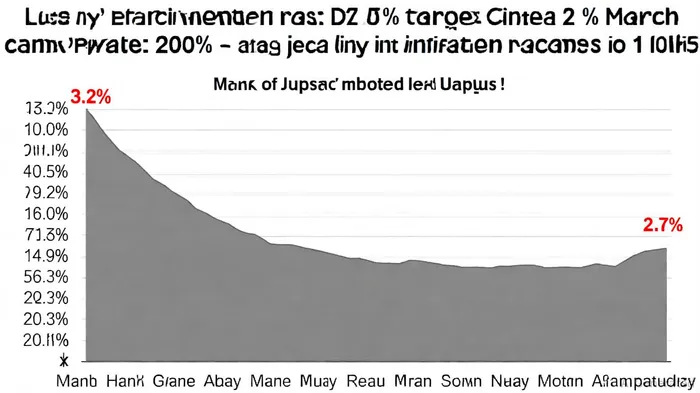

Japan's economy is navigating a delicate balancing act in 2025. After years of deflationary struggles, the nation now faces the challenge of cooling inflation while avoiding a relapse into stagnation. With core inflation easing to 2.7% in August 2025 from a peak of 3.2% in March, the Bank of Japan (BOJ) has opted to maintain its key interest rate at 0.5%, adopting a cautious “wait-and-see” approach. This measured stance, combined with resilient GDP growth and structural shifts in household investment behavior, has created a unique window for investors to capitalize on undervalued sectors poised to thrive in a soft landing scenario.

The Soft Landing Framework: Inflation Eases, Growth Persists

Japan's second-quarter GDP expanded by 0.5% quarter-on-quarter, driven by robust private consumption and a rebound in exports. While the BOJ's 2% inflation target remains elusive, the decline in headline inflation—from 3.1% in July to 2.7% in August—signals that government utility subsidies and moderating food price pressures are providing temporary relief. This soft landing trajectory—where inflation normalizes without triggering a recession—is critical for investors. It allows the BOJ to avoid aggressive rate hikes, preserving liquidity in markets while still incentivizing structural reforms.

However, risks loom. U.S. tariffs on Japanese exports, particularly in the automotive sector, threaten to erode growth in the coming quarters. Projections suggest a contraction in Q3 2025, with an annualized rate of -1.7% due to weaker residential investment and export volumes. Yet, the resilience of Japan's labor market—unemployment remains at a healthy 2.5%—and the U.S. Federal Reserve's anticipated rate cuts in 2026 could cushion the blow.

Resilient Sectors: Where to Allocate Capital

1. Exports and Automotive Innovation

Japan's export sector, particularly automotive manufacturing, has demonstrated remarkable adaptability. Despite U.S. tariffs, firms like ToyotaTM-- and HondaHMC-- have maintained export volumes by trimming prices and avoiding domestic retail inflation. Toyota's FY2025 financial results underscore this resilience, with a 18% increase in equipment orders driven by AI and 5G demand. For investors, the automotive sector offers both defensive and growth characteristics. Dividend yields in the automotive parts industry average 2.60%, reflecting strong cash flows.

2. Financials: A Shift in Household Behavior

The BOJ's inflationary environment has spurred a seismic shift in Japanese households, which are reallocating cash savings into risk assets. The Nippon Individual Savings Account (NISA) tax-exempt system has accelerated this trend, boosting demand for equities and mutual funds. The Nikkei 225, trading at a forward P/E of 14.96 as of July 2025, offers compelling valuations compared to its 10-year average of 16.40. Financial institutionsFISI--, particularly wealth management firms, stand to benefit as households seek higher returns amid rising interest rates.

3. Real Estate: A Tale of Two Markets

Japan's real estate sector is bifurcating. Prime commercial properties in Tokyo and Osaka have seen land price increases of 2.7% year-on-year, with foreign investment surging by 45% in H1 2025. Office and logistics sectors are attracting capital, with Q1 2025 commercial real estate investment volume rising 24% to ¥1.9 trillion. However, J-REITs face headwinds, with acquisition volumes down 16% year-on-year as investors adopt a more selective stance. For income-focused investors, REITs with stable occupancy rates—such as those in Tokyo's central 23 wards—remain attractive, offering yields of 5.5–6.0%.

Strategic Entry Points: Timing the Soft Landing

The key to capitalizing on Japan's soft landing lies in timing. Investors should prioritize sectors with structural tailwinds:

- Technology and AI-driven manufacturing: Companies like Tokyo Electron, benefiting from global demand for 5G and AI infrastructure, offer growth potential despite a P/E of 17.2x.

- Wealth management and banking: As households shift ¥51 trillion in cash savings to equities, firms like NomuraNMR-- and SMBC Nikko are well-positioned to capture market share.

- Prime commercial real estate: With Tokyo's office occupancy rates at 97.2%, developers of mixed-use complexes in Shibuya and Shinagawa could outperform in a low-interest-rate environment.

Risks and Mitigation

While the soft landing scenario is favorable, investors must remain vigilant. U.S. tariff escalations could disrupt export-driven sectors, and a weaker yen may pressure import-dependent industries. Hedging strategies, such as currency-hedged ETFs or diversified portfolios across sectors, can mitigate these risks. Additionally, monitoring the BOJ's policy response to inflation—particularly its exit from negative rates—will be critical in 2026.

Conclusion

Japan's inflation slowdown, coupled with a soft landing trajectory, presents a rare opportunity to invest in undervalued, resilient sectors. From export-led manufacturing to financial innovation and prime real estate, the country's structural reforms and demographic shifts are creating long-term value. For investors willing to navigate short-term uncertainties, the current environment offers a compelling case for strategic entry.

Comentarios

Aún no hay comentarios