Japan's Equities in a New Rate-Cut Cycle: A Strategic Buy-In Opportunity?

Japan's equity market is at a crossroads, shaped by a confluence of structural reforms, shifting monetary policy, and evolving investor behavior. As the Bank of Japan (BOJ) navigates a new rate-cut cycle and the economy transitions from decades of deflation to moderate inflation, the question arises: Is this the moment for a strategic buy-in? The answer lies in dissecting the interplay between policy-driven valuation shifts and market momentum, a dynamic that has already drawn the attention of global heavyweights like Warren Buffett[2].

Structural Reforms: The Foundation for Shareholder Value

The Tokyo Stock Exchange's (TSE) “Action to Implement Management that is Conscious of Cost of Capital and Stock Price” has catalyzed a corporate governance revolution. Companies are now prioritizing capital efficiency, with share buybacks surging to record levels in 2025[1]. This shift has not only enhanced shareholder returns but also signaled a broader cultural change in how Japanese firms allocate capital. According to a report by JPMorganJPM--, firms adhering to these reforms have seen their equity valuations outperform peers by an average of 12% year-to-date[1]. The result is a market increasingly aligned with global standards, attracting both institutional and retail investors.

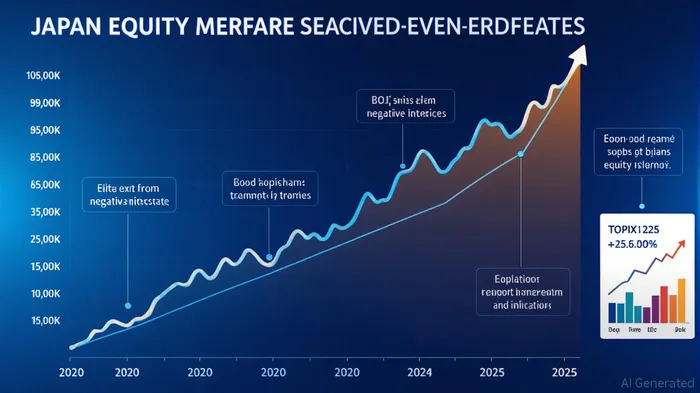

Monetary Policy and the Exit from Negative Rates

While the BOJ's recent monetary policy specifics remain opaque, its broader trajectory is clear: a deliberate exit from negative interest rates. This move, coupled with the Nippon Individual Savings Account (NISA) expansion, has incentivized households to redirect savings into equities. Data from Morgan StanleyMS-- indicates that Japan's retail investor base has grown by 18% in 2025, with NISA accounts contributing to a 22% increase in equity holdings[3]. The BOJ's pivot reflects a recognition that prolonged negative rates have distorted asset prices and stifled risk-taking—a correction that now appears to be gaining traction.

Market Momentum: Inflation, Wages, and Investor Sentiment

Japan's transition to moderate inflation has further bolstered equity valuations. Unlike the wage stagnation of previous decades, 2025 has seen wage growth stabilize at 3.5%, a level that supports consumer spending and corporate margins[4]. This environment, combined with improved corporate governance, has created a virtuous cycle: higher earnings, stronger balance sheets, and a more attractive risk-rebalance for global investors. Buffett's recent investments in Japanese blue-chips underscore this trend, with Berkshire Hathaway citing “a unique alignment of structural and macroeconomic tailwinds” as a key driver[2].

Global Uncertainties and Japan's Resilience

Despite global trade tensions and geopolitical risks, Japan's economy remains a relative safe haven. Its mild inflation trajectory, coupled with a corporate sector focused on capital discipline, positions it to weather external shocks better than many peers. As noted in a JPMorgan Private Bank analysis, Japan's equity market is now among the top three global markets for dividend yields and buyback activity—a testament to its evolving appeal[4].

Conclusion: A Strategic Inflection Point

Japan's equities are no longer a bet on stagnation but a play on transformation. The BOJ's policy normalization, corporate governance reforms, and a newly empowered retail investor base have created a market environment where valuation shifts are both policy-driven and self-reinforcing. For investors, the challenge is not whether to participate, but how to position for sustained momentum. As Buffett's playbook suggests, this is a generational opportunity—one that demands a nuanced understanding of Japan's evolving economic narrative[2].

Comentarios

Aún no hay comentarios