Japan Display (TSE:6740): A Contrarian Play on Display Tech's Future Amid Mixed Fundamentals

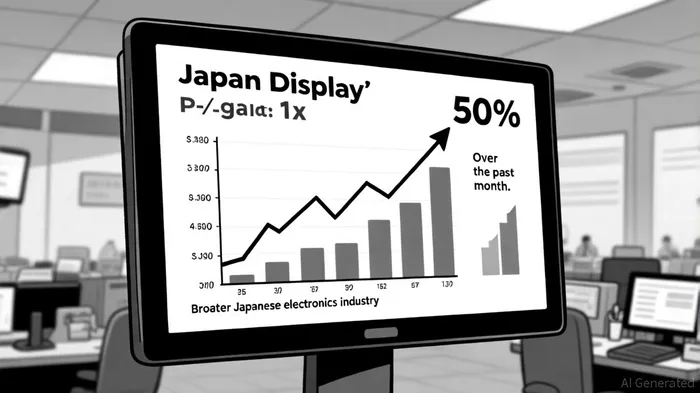

Japan Display Inc. (TSE:6740) has emerged as a paradox in the display technology sector: a company with a stock price surging 50% in the past month and a 42% year-to-date rally, yet trailing a five-year decline of 51% and reporting a net loss of -20.26 billion JPY in its most recent quarter [1]. This divergence between short-term momentum and long-term fundamentals raises critical questions about its valuation potential.

Market Momentum: A Short-Term Catalyst

The recent 50% price surge has been fueled by speculative trading and broader macroeconomic tailwinds. On September 19, 2025, the stock closed at ¥27.00, a 3.85% daily gain, amid a broader Nikkei 225 rally projected to hit 43,225 by month-end [2]. High trading volumes—peaking at 407 million shares on September 17—suggest growing retail and institutional interest [3]. However, this momentum appears disconnected from JDI's core financials. Despite a 31.22% improvement in quarterly losses compared to the prior period, the company's EBITDA margin remains at -17.36%, and its price-to-sales (P/S) ratio of 1x lags behind its peer average of 1.3x [4].

Industry Tailwinds: OLED and Next-Gen Tech

The global OLED market, valued at $65.7 billion in 2025, is projected to grow at a 13.7% CAGR through 2035, driven by foldable smartphones, automotive displays, and energy-efficient TVs [5]. JDI's recent development of eLEAP OLED technology for tablets and laptops positions it to capture incremental demand in high-margin applications [6]. Meanwhile, the company's foray into microLED and quantum dot (QLED) technologies—prototypes unveiled in 2019—aligns with long-term industry shifts toward higher resolution and energy efficiency [7].

Yet JDI faces existential challenges. Japan's display market share has plummeted to 1.1%, eclipsed by China's 50.8% dominance in OLED production [8]. The company's acquisition of JOLED's R&D division and partnership with Chinese firm HKC signal a strategic pivot to leverage external expertise amid capital constraints [9].

Valuation Dilemma: Undervaluation or Desperation?

JDI's 1x P/S ratio suggests undervaluation relative to peers, but this metric masks deeper issues. The company's five-year decline and -35.08 billion JPY EBITDA underscore structural inefficiencies. However, the display industry's transition to microLED and QLED could create a “value trap” scenario: investors betting on future earnings potential may overlook near-term liquidity risks.

A critical inflection point lies in JDI's ability to commercialize its next-gen technologies. For instance, its collaboration with Nikon and Canon on advanced manufacturing equipment could reduce production costs for microLED displays [10]. If successful, this might justify the current valuation premium, especially as the Japan QLED market is forecast to grow at a 13.3% CAGR through 2033 [11].

Risks and Opportunities

While JDI's R&D pipeline is promising, execution risks loom large. The company's nine consecutive annual net losses and reliance on government subsidies highlight its fragility [12]. Conversely, the broader industry's shift toward OLED and microLED could catalyze a turnaround if JDI secures key partnerships or wins contracts in automotive or AR/VR sectors.

Conclusion

Japan Display's stock price surge reflects a speculative bet on its potential to navigate the display industry's technological evolution. While its current valuation appears undervalued relative to peers, investors must weigh this against its weak financials and competitive disadvantages. For those with a long-term horizon, JDI could represent a high-risk/high-reward opportunity if it successfully scales its next-gen technologies. However, the path to profitability remains fraught with execution risks and industry headwinds.

Comentarios

Aún no hay comentarios