James Hardie's Azek Acquisition: A Balancing Act Between Growth and Shareholder Accountability

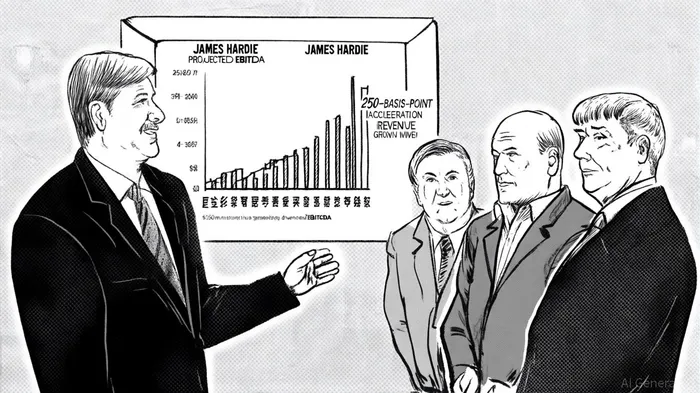

The $8.75 billion acquisition of Azek by James Hardie, finalized in late 2024, represents a bold strategic pivot for the Australian building materials giant. By merging with Azek, a U.S.-based leader in composite decking and exterior building products, James Hardie has expanded its total addressable market to $23 billion and projected annual revenue growth by over 250 basis points[1]. This move, however, has sparked intense debate among investors and analysts, who are scrutinizing the trade-offs between aggressive growth ambitions and corporate accountability.

Strategic Rationale: Market Expansion and Synergy Potential

The acquisition is framed as a catalyst for James Hardie's long-term growth. By integrating Azek's $1.8 billion in adjusted EBITDA and $5.9 billion in trailing net sales[1], the combined entity gains a dominant position in North America's $15 billion exterior building products market. According to a report by James Hardie, the transaction is expected to generate at least $350 million in annual adjusted EBITDA synergies through operational efficiencies and cross-selling opportunities[1]. These synergies, if realized, could accelerate James Hardie's revenue trajectory and solidify its leadership in a sector poised for resilience amid housing market fluctuations.

However, the financial engineering underpinning the deal has raised red flags. The transaction structure—offering Azek shareholders $26.45 in cash and 1.0340 James Hardie shares per Azek share—results in a 35% dilution of James Hardie's existing equity base[4]. This dilution, which bypassed shareholder approval under ASX Listing Rules[3], has drawn sharp criticism from institutional investors. A coalition of 21 Australian fund managers, representing over $100 billion in assets, publicly condemned the lack of transparency, arguing that such significant dilution warranted direct shareholder consent[3].

Corporate Accountability and Shareholder Backlash

The backlash underscores a broader tension in corporate governance: the balance between executive autonomy and investor trust. James Hardie's decision to avoid a shareholder vote for the Azek deal, citing time-sensitive market conditions, has been interpreted as a prioritization of short-term strategic momentum over long-term stakeholder alignment. This sentiment was amplified by Fitch Ratings, which revised James Hardie's credit outlook to “negative” in March 2025, citing concerns over elevated EBITDA leverage post-acquisition[2].

Yet, the company has taken steps to address investor concerns. In response to the fund managers' letter, James Hardie reaffirmed its commitment to retaining its primary listing on the ASX and pledged not to shift its headquarters to the NYSE without shareholder approval[3]. These assurances, while welcomed, have done little to quell skepticism about the board's risk tolerance. Critics argue that the acquisition's high leverage and dilutive nature could strain James Hardie's balance sheet, particularly if macroeconomic headwinds—such as rising interest rates or a slowdown in U.S. housing demand—curtail Azek's growth potential.

Financial Projections and Risk Mitigation

Despite these risks, the combined entity's financials appear robust. As of December 31, 2024, the company reported $5.9 billion in net sales and adjusted EBITDA exceeding $1.8 billion[1], suggesting strong near-term cash flow generation. James Hardie has also emphasized that the acquisition will be accretive to cash earnings per share in the first full fiscal year post-closing[1], a claim that hinges on effective integration of Azek's operations.

A critical question remains: Can James Hardie sustain its growth narrative while addressing shareholder concerns? The answer will depend on its ability to deliver on synergy targets, manage debt levels, and maintain transparency. For now, the market is watching closely.

Conclusion

James Hardie's Azek acquisition exemplifies the dual-edged nature of transformative M&A. While the deal promises to unlock significant market opportunities, it also tests the boundaries of corporate accountability. For investors, the key takeaway is clear: aggressive growth strategies must be paired with transparent governance to preserve trust. As the combined company navigates integration challenges and macroeconomic uncertainties, its ability to reconcile these priorities will define its long-term success.

Comentarios

Aún no hay comentarios