Iron Mountain's Strategic Debt Financing and Growth Trajectory in the Data Center and AI Sectors

Iron Mountain’s recent €1.2 billion senior notes offering, priced at 4.75% with a 2034 maturity, represents a calculated move to refinance short-term debt and fuel long-term growth in high-demand sectors like data centers and AI. By upsizing the offering from €750 million, the company has secured critical liquidity to redeem its 3.875% GBP Senior Notes due 2025 and reduce near-term leverage, while aligning capital with strategic priorities [1]. This analysis evaluates the financial prudence of the offering and its potential to drive value creation in an evolving digital infrastructure landscape.

Assessing Financial Prudence: Debt Terms and Leverage Management

Iron Mountain’s debt-to-EBITDA ratio currently stands at 5.40x, with an interest coverage ratio of 1.66x, reflecting moderate leverage but manageable risk given its robust cash flow generation [3]. The company’s target leverage range of 4.5x to 5.5x suggests the €1.2B offering, which increases leverage to approximately 5.0x post-redemption, remains within acceptable bounds [1]. By extending the maturity profile of its debt to 2034, Iron MountainIRM-- mitigates refinancing risks and aligns borrowing costs with long-term asset lifecycles. While the 4.75% coupon is higher than its existing 3.875% GBP notes, the longer maturity reduces immediate interest burden and provides flexibility for reinvestment [2].

The proceeds’ allocation further underscores prudence. Redeeming the 2025 GBP notes eliminates a near-term maturity cliff, while repaying revolving credit facility debt lowers variable-rate exposure. These actions stabilize the balance sheet, enabling the company to channel capital toward higher-return opportunities in data centers and AI [1].

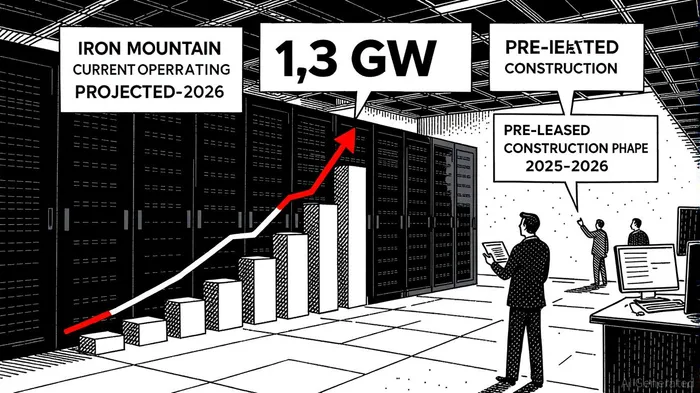

Growth in Data Centers: Capacity Expansion and Demand Alignment

Iron Mountain’s data center segment is a cornerstone of its value proposition. With 450 MW of operating capacity at 96% occupancy and 202 MW under construction (60% pre-leased), the company is poised to nearly triple its portfolio to 1.3 GW by 2026 [2]. This expansion, concentrated in high-demand markets like Northern Virginia, directly addresses surging demand for cloud computing and edge infrastructure driven by AI adoption. For context, the segment’s 24% year-over-year revenue growth in Q2 2025—bolstered by 26% organic storage growth—underscores its scalability [4].

The strategic focus on pre-leased construction (628 MW allocated for future development) minimizes idle capacity risk, ensuring demand is secured before significant capital outlays. This approach, combined with $1 billion in annual operating cash flow, positions Iron Mountain to fund growth without overleveraging [5].

AI Integration: Enhancing Digital Solutions for Competitive Edge

Beyond physical infrastructure, Iron Mountain is leveraging AI to differentiate its digital offerings. Its Insight Digital Experience Platform (DXP) now incorporates AI-powered tools for workflow automation and intelligent decision-making, catering to enterprises seeking efficiency in data management [4]. This innovation aligns with broader trends in AI inference and cloud infrastructure, where Iron Mountain’s assets are uniquely positioned to support workloads requiring low-latency processing.

The company’s Q2 results, including record $1.7 billion in revenue and $628 million in Adjusted EBITDA, validate the effectiveness of its "Matterhorn Strategy," which prioritizes high-growth segments [5]. Despite a $43.3 million net loss attributed to currency fluctuations, the guidance increase to $6.79–$6.94 billion in 2025 revenue reflects confidence in sustaining momentum [5].

Long-Term Value Creation: Balancing Risks and Rewards

Critics may question whether Iron Mountain’s leverage (5.40x debt-to-EBITDA) could constrain flexibility during economic downturns. However, the company’s strong occupancy rates, pre-leased capacity, and cash flow generation mitigate these risks. The data center and AI sectors’ structural growth—driven by digital transformation and AI adoption—further justify the capital allocation.

A would illustrate its aggressive expansion trajectory. Additionally, tracking its leverage ratio against the 4.5x–5.5x target over the next two years will be critical to assessing financial discipline.

Conclusion

Iron Mountain’s €1.2B senior notes offering is a strategically sound move to optimize its capital structure while accelerating growth in data centers and AI. By refinancing short-term debt, extending maturities, and investing in high-occupancy, pre-leased assets, the company balances prudence with ambition. As digital infrastructure demand intensifies, Iron Mountain’s dual focus on physical expansion and AI-driven digital solutions positions it to capture long-term value, provided it maintains disciplined leverage management.

Source:

[1] Iron Mountain IncorporatedIRM-- Upsizes and Prices Debt Offering [https://www.stocktitan.net/news/IRM/iron-mountain-incorporated-upsizes-and-prices-debt-7ivpilfmukt4.html]

[2] Iron Mountain Q2 2025 slides: Record results drive guidance increase [https://www.investing.com/news/company-news/iron-mountain-q2-2025-slides-record-results-drive-guidance-increase-93CH-4172717]

[3] Iron Mountain (IRM) Financials 2025 [https://www.marketbeat.com/stocks/NYSE/IRM/financials/]

[4] Iron Mountain Incorporated (IRM) Stock Price [https://www.datainsightsmarket.com/companies/IRM]

[5] Iron Mountain Reports Second Quarter 2025 Results [https://investors.ironmountain.com/news/news-details/2025/Iron-Mountain-Reports-Second-Quarter-2025-Results/default.aspx]

Comentarios

Aún no hay comentarios